Relationships in the Supply Chain

John Fernie

Introduction

Relationship marketing (RM), Customer Relationship Marketing (CRM), e-CRM for online businesses and Collaborative Planning, Forecasting and Replenishment (CPFR) are only some of the acronyms to appear in the academic literature in the last 10 to 15 years. This represents a major paradigm shift in marketing and logistics away from a traditional transactional view of exchange between buyers and sellers to a more proactive, collaborative relationship approach. The purpose of this chapter is to discuss the conceptual framework of supply chain relationships and their applications to retailing through Quick Response (QR) and Efficient Consumer Response (ECR) initiatives. Finally, the role of logistical service providers in supply chain relationships will be reviewed.

Changing Buyer Seller Relationships

The origins of the relationship approach to understanding buyer–seller interaction at different parts of the supply chain goes back several decades, when the conventional marketing mix paradigm began to be challenged. The growth of the service sector, the move from mass marketing to micro marketing to mass customization, with the associated database infrastructure, allowed companies to target customers more effectively. While consumer marketing embraced a relationship approach to improve customer retention, these trends were particularly prominent in industrial markets where the Industrial Marketing and Purchasing Group (IMP) initiated much of the business to business research in this area.

In parallel with these developments was a growing literature in logistics and supply chain management embodying similar paradigms and constructs. The fourth P of the marketing mix, Place, was traditionally centred on the wholesale and retail trade and how suppliers would channel their products to market. By the 1980s two key factors would begin to elevate logistics to greater prominence in the literature: the rise in power of the multiple retailers, thereby changing power relationships, and the need to eliminate inventory and non-value added activities in getting products to market. Thus, to compete with Japanese manufacturing, European and US companies embraced Just-In-Time (JIT) techniques, reduced their supply base and worked more closely with the remaining suppliers. So throughout the 1990s debates emerged on the lean compared with the agile supply chain, the latter more relevant to the fast-moving consumer goods (FMCG) market.

Interestingly, with a few exceptions such as Martin Christopher, the academic literature on relationships tends to be published in discrete camps as evidenced by readers on marketing (Hart, 2003) and logistics (Waters, 2003) which exhibit similar constructs when discussing relationships but very rarely cross-reference between ‘marketing’ and ‘supply chain’ literatures. Nevertheless, key themes are common – power and dependence, trust and commitment, co-operation and co-opetition, which will be discussed in turn.

Power and Dependence

‘Power in the supply chain can be defined operationally as the ability of one entity in the chain to control the decision of another entity’ (Daparin and Hogarth-Scott, 2003: 259). It is generally agreed that the power base has shifted over time from supplier to retailer. When French and Raven (1959) produced their seminal work, the suppliers controlled the supply chain. The five power bases that they identified – reward power, coercive power, referent power, legitimate power and expert power – would lead to dependency of the retailer on the supplier, especially with regard to expert power in that the supplier had the marketing/logistics expertise in the channel. Clearly this has changed in 45 years in that retailers can delist (coercive), reward, joint promote (referent) and dictate terms (legitimate) to suppliers because of their dominant market position (expert power).

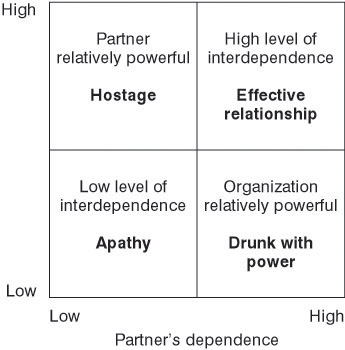

The nature of such relationships between manufacturers and retailers was discussed by Kumar (1996) in a study of 400 relationships. He categorized them into different levels of dependence (Figure 2.1). The ‘win–win’ quadrant is the top right category where there is a high level of interdependence between parties. The ‘hostage’ and ‘drunk with power’ categories could lead to a breakdown in the relationship.

Figure 2.1: Effects of Interdependence

Trust and Commitment

According to Kumar (1996) trust is the antithesis of power, and it is trust that leads to co-operation. However, trust can easily be heralded as ‘the glue that holds a relationship’ (O’Malley, 2003: 130), but it is difficult to measure because this involves social networks which are inherently fluid in a retail buying context. At an organizational level trust, and therefore commitment, can be related to the relationship lifecycle. Many UK private label suppliers have grown with the retailers which they supplied, especially in the area of chilled fresh food where the category was developed by the retailer in partnership with these companies. This does not guarantee stability as evidenced by Marks and Spencer’s breakdown in relationship with some UK clothing suppliers when it decided to source products offshore and thereby sever links which had been fostered for generations. Similarly, the introduction of factory gate pricing by grocery retailers is viewed by many suppliers in the UK as opportunistic behaviour which impacts upon trust in the relationship.

Co operation and co opetition

Much of the literature from ECR conferences and trade bodies implies greater collaboration between supply chain partners. This is discussed in more depth in the next section. In the academic literature, most attention has been focused upon collaborative advantage rather than competitive advantage (Christopher and Peck, 2003) and co-opetition (Brandenburger and Nalebüff, 1996) rather than competition. The thrust of this argument is that in sectors such as the FMCG industry where demand is stable, it is more appropriate for companies to ‘grow the cake’ in specific categories by boosting demand and compete on conventional marketing criteria. Similarly, companies have reviewed their logistics operations and are now willing to collaborate with competitors on ‘invisible’ shared resources but not on promotion or ‘visible’ marketing efforts. This mirrors the well established approach by Japanese manufacturing companies which cooperate on R&D but compete on the branded consumer goods in the marketplace.

The creation of value added partnerships within industrial sectors is based on the tenets of resource-based theory, transaction cost analysis and network theory. In essence, the key decisions that have to be taken by companies within the supply chain relate to their core competencies, the allocation of resources and the network of organizations with which they interact. The best examples of such a division of labour is in the clothing ‘fast fashion’ sector which is discussed in much length elsewhere in the book. Benetton is the classical example of the network organization, with its international poles throughout the world. Here Benetton keeps the capital-intensive parts of the operation ‘in house’, contracting out to small and medium sized enterprises (SMEs) the labour-intensive phase of production (tailoring, knitting, ironing). Likewise, Zara has developed its production pole at La Coruna with its integrated network of SMEs in Galicia and N. Portugal.

In other parts of the retail sector, the rosy picture of collaboration and co-operation is less evident from published empirical research. The previous edition of this volume cited work by Hogarth-Scott and Parkinson (1993) and Ogbonna and Wilkinson (1996) in the food sector of a more adversarial approach than the ‘partnership’ dialogue promulgated at the time. In the basic clothing sector similar trends were evident (Fernie, 1998) and the downward pressure in prices with the intense competition in the UK clothing market has done little to redress the emphasis on tough price negotiations. Indeed, Philip Green’s takeovers of BHS and Arcadia have been marked by his public pronouncements on the renegotiating of supplier contracts.

The Competition Commission (2000) investigation of the nature of competition in the UK supermarket sector was generally supportive of the status quo except for the need for a supplier code of practice to eliminate the worst excesses of retailer power on suppliers. Anecdotal evidence would appear to suggest that prices were being driven down to unacceptable levels, plus retailers required other ‘contributions’ for slotting allowances and other discounts for volume purchases. In a more recent study of buyer–seller relationships in the UK and Australian markets, Daparin and Hogarth-Scott (2003) challenge many of the conventional views on co-operation, trust and power. They claim that much of the literature argues that power is a negative construct and is invariably viewed as a distinctive independent construct divorced from the construct of co-operation. From their research, they would maintain that co-operation occurs as a result of compliant behaviour brought about by the application of power.

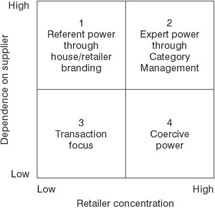

Using the results from their survey, Daparin and Hogarth-Scott (2003) discuss dependence and power in relation to retail concentration and supplier dependency. Therefore, where retail concentration is high and there is low retailer dependence on the supplier, retailers will be more likely to use coercive power. Where concentration levels are high but dependence on suppliers is also high, retailers are more likely to use expert power, probably through the use of category management. The use of such expert power leads to co-operative behaviour which in turns leads to greater trust within the relationship. This model is illustrated in Figure 2.2, which shows that the use of coercive/reward power can lead to capitulation in the relationship even if trust is broken within the context of category management and the referent/expert power in the right hand quadrant disintegrates into coercive power.

Figure 2.2: Power Strategies of Retailers

Quick Response

The term Quick Response (QR) was coined in the United States in 1985 (Fernie, 1994; Hines, 2001) when Kurt Salmon Associates (KSA) recognized deficiencies in the fashion supply chain. According to KSA, only 11 weeks out of the 66-week lead time in the pipeline are spent on the actual processes (value adding time / horizontal time), and the rest (non-value adding time/vertical time) are wasted in the form of work in progress (WIP) and finished inventories at various stages of the complex system (KSA, 1997; Christopher, 1997, 1998; Christopher and Peck, 1998). The resultant losses arising from this were estimated at US $25 billion, due to stocking too large an inventory of unwanted items and too small of the fast movers.

In response to this situation, the American textiles, apparel and retail industries formed the VICS (Voluntary Interindustry Commerce Standards Association) in 1986 as their joint effort to streamline the supply chain and make a significant contribution in getting the in-vogue style at the right time in the right place (Fernie, 1994,1998) with increased variety (Giunipero et al, 2001; Lowson, 1998; Lowson, King and Hunter, 1999) and inexpensive prices. This is done by applying an industry standard in information technologies (such as bar-codes, EDI, shipping container marking and roll ID) and contractual procedures (Lowson et al, 1999; Ko, Kincade and Brown, 2000; Giunipero et al, 2001) among the supply chain members. Not only is QR an IT-driven systematic approach (Forza and Vinelli, 1996, 1997, 2000; Hunter, 1990; Riddle et al, 1999) to achieve supply chain efficiency from raw materials to retail stores, it is also a win–win partnership in which each member of the supply chain shares the risks and the benefits of the partnership on an equal basis to realize the philosophy of ‘the whole is stronger than the parts’.

QR, in principle, requires the traditional buyer–supplier relationship, which is too often motivated by opportunism, to transform into a more collaborative partnership. In this QR partnership, the objectives of the vendor are to develop the customer’s business. The benefit to the vendor is the likelihood that it will be treated as a preferred supplier. At the same time, the costs of serving that customer should be lower as a result of a greater sharing of information, integrated logistics systems and so on (Christopher, 1997; Christopher and Juttner, 2000). Thus, partnership among the supply chain members is a prerequisite of QR programmes.

QR’s ultimate goal, nonetheless, is to give customers the savings that are gained through the initiative (Giunipero et al, 2001). The last, and perhaps one of the most important tenets of the original proposition of the QR concept is that QR is a survival strategy of the domestic manufacturing sector in the advanced economies against competition from low- cost imports (Finnie, 1992; MITI, 1993, 1995, 1999; METI, 2002). In the case of the United States, the QR initiative was expected to make a considerable contribution to the Pride with the USA campaign, which promoted the excellence of US-made products to American consumers, who had already been familiar with inexpensive imported casual clothing.

With the basic fashion category, relatively steady demand is a feature of the market, therefore the US-born QR concept places much focus on the relationship between retailers and apparel manufacturers. The eventual benefits for both parties are detailed in Table 2.1. Giunipero et al (2001) summarize the hierarchical process of QR adaptation as an integral part of QR as business process re-engineering (BPR) (Table 2.2). This model, most appropriate for the apparel–retail linkage in basic clothing, has become a role model for QR programmes in other advanced economies.

|

Retailer QR benefits |

Supplier QR benefits |

|---|---|

|

Reduced costs |

Reduced costs |

|

Reduced inventories |

Predictable production cycles |

|

Faster merchandise flow |

Frequency of orders |

|

Customer satisfaction |

Closer ties to retailers |

|

Increased sales |

Ability to monitor sales |

|

Competitive advantage |

Competitive advantage |

|

Source: Quick Response Services (1995) |

|

|

STAGE 1 |

(Introduction of basic QR technologies) |

|

SKU level scanning |

|

|

JAN (standard) bar-code |

|

|

Use of EDI |

|

|

Use of standard EDI |

|

|

STAGE 2 |

(Internal process re-engineering via technological and organizational |

|

improvement) |

|

|

Electronic communication for replenishment |

|

|

Use of cross-docking |

|

|

Small amounts of inventory in the system |

|

|

Small lot size order processing |

|

|

ARP (automatic replenishment programme) |

|

|

JIT (Just-In-Time) delivery |

|

|

SCM (shipping container marking) |

|

|

ASN (Advanced Shipping Notice) |

|

|

STAGE 3 |

(Realization of a collaborative supply chain and win–win relationship) |

|

Real-time sales datasharing |

|

|

Stock-out data sharing |

|

|

QR team meets with partnerships |

|

|

MRP (Material Resource Planning) |

|

|

Sources: Giunipero et al, 2001; KSA, 1997 |

|

Having achieved many of the QR goals, VICS has implemented a CPFR (Collaborative Planning, Forecasting and Replenishment) programme, to synchronize market fluctuations and the supply chain in a more real-time fashion. Through establishing firm contracts among supply chain members and allowing them to share key information, CPFR makes the forecasting, production and replenishment cycle ever closer to the actual demands in the marketplace (VICS, 1998). While the American practices have played a leading role in the QR and SCM initiatives in the apparel industry, much of the success is in the basic fashion segment, where the manufacturing phase is normally the first to be transferred offshore. In this sense, the philosophy of QR as the survival strategy of fashion manufacturing in the industrial economies has not been realized.

QR in Japan

While the US apparel industry competes largely on a cost basis in the basic fashion segment, Japanese firms have forged their success on bridge fashion with flexible specialization (Piore and Sabel, 1984) in a subcontracting network of process specialists in the industrial districts (Sanchi) led by the ‘apparel firms’ with design and marketing expertise. The US fashion industry essentially produces for the international market that is mostly controlled by the largest retailers, which are the real promoters and the first to profit from QR (Scarso, 1997; Taplin and Ordovensky, 1995). Thus, the Japanese fashion industry shows clear contrasts to its US and most of the European counterparts, where large retailers control the supply chain (Azuma, 2001).

Harsh competition from offshore and stagnant domestic consumption in the past decade has come to highlight the costly structure and the lack of partnership in the Japanese fashion supply chain (MITI, 1993, 1999; METI, 2002). This led to the formation of QRPA (Quick Response Promotion Association; now FISPA-Fashion Industry SCM Promotion Association) in 1994, as a joint endeavour of the Japanese T–A–R (textiles, apparel and retailing) industries to regain competitiveness of the overall domestic industry in order to effectively and efficiently serve everchanging customers needs.

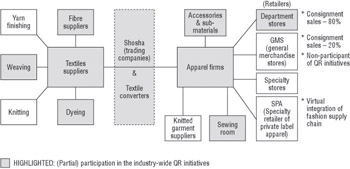

Ten years has passed since the introduction of the first QR initiative in the Japanese fashion industry. A series of programmes has been implemented in an orderly manner, from the retail–textiles and textiles–apparel, to apparel–sewing interfaces (Figure 2.3). FBA (Fashion Business Architecture) is an application of CPFR to the interface of the Japanese department stores and apparel firms. With an increasing adaptation of the industry standard platforms, such as EDI (JAIC: Japan Apparel Industry Council format), JAN (Japan article number) code, and ASN (Advanced Shipping Notice), department stores and apparel firms have achieved some of the expected QR benefits by eliminating the labour-intensive and costly processes of ticketing and inspections in a smooth flow of information. Elsewhere in the supply chain, however, there are fewer QR initiatives, apart from some positive results at a textiles–apparel (T–A) collaboration programme in men’s heavy garments manufacturing, and a fibre sourcing network at the highly concentrated sector upstream of the supply chain.

Figure 2.3: The Structure of the Japanese Fashion Industry

Thus, QR initiatives have not necessarily worked out throughout the domestic apparel manufacturing sector. Unless the ongoing partnership programme in the mid-stream of the supply chain is accomplished, the Japanese QR in the long run is likely to be limited to retailing and apparel firms, providing that offshore sourcing locations are becoming less important. Nevertheless, Apparel–Sewing (A–S) Net, one of the current initiatives linking the apparel firms with their sewing subcontractors, is designed to be applied for sourcing in China.

Efficient Consumer Response

Efficient Consumer Response (ECR) emerged in the United States partly through the joint initiatives between Wal-Mart and Procter and Gamble and the increased competition in the traditional grocery industry in the early 1990s due to recession and competition from new retail formats. Once again, Kurt Salmon was commissioned to analyse the supply chain of a US industrial sector. Similar trends were evident to those in its earlier work in the apparel sector: excessive inventories, long uncoordinated supply chains and an estimated potential savings of US $30 billion, 10.8 per cent of sales turnover (see Table 2.3).

|

Supply chain study |

Scope of study |

Estimated savings |

|---|---|---|

|

Kurt Salmon Associates (1993) |

US |

|

|

Coca-Cola Supply Chain Collaboration (1994) |

|

|

|

ECR Europe (1996 ongoing) |

|

|

|

Source: Fiddis, 1997 |

||

ECR programmes commenced in Europe in 1993, a European Executive Board was created in 1994 and a series of projects and pilot studies were commissioned. For example, the Coopers and Lybrand survey of the grocery value chain estimated potential savings of 5.7 per cent of sales turnover (Coopers and Lybrand, 1996). Since then ECR has been adopted by around 50 countries in all the continents of the world. The European ECR initiative defines ECR as a ‘global movement in the grocery industry focusing on the total supply chain – suppliers, manufacturers, wholesalers and retailers, working closer together to fulfil the changing demands of the grocery consumer better, faster and at least cost’ (Fiddis, 1997: 40).

Despite the apparent emphasis on the consumer, many of the early studies focused mainly on the supply side of ECR. Initially reports sought efficiencies in replenishment and the standardization of material handling equipment to eliminate unnecessary handling through the supply chain. The Coopers and Lybrand report in 1996 and subsequent re-prioritizing towards demand management, especially category management (see McGrath, 1997) have led to a more holistic view of the total supply chain being taken. Indeed, the greater cost savings attributed to the Coopers’ study compared with that of Coca-Cola can be attributed to a more narrow perspective of the value chain in the Coca-Cola survey (Table 2.3).

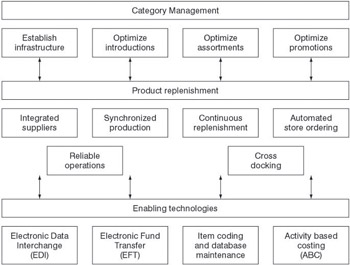

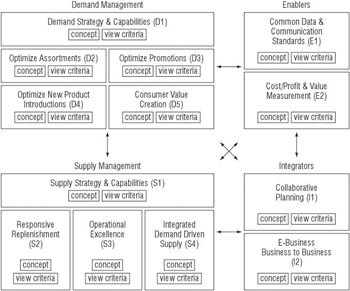

The main focus areas addressed under ECR are Category Management, product replenishment and enabling technologies. As can been seen from Figure 2.4, these are broken down into 14 further areas where improvements can be made to enhance efficiency. After the exceptional success of ECR Europe’s annual conferences in the late 1990s/early 2000s, a series of initiatives was promulgated which encouraged much greater international collaboration. ECR movements began to share best practice principles, most notably the bringing together of the different versions of the US, Europe, Latin America and Asia scorecards to form a Global Scorecard. The Scorecard was used to assess the performance of trading relationships. These relationships were measured under four categories – demand management, supply management, enablers and integrators (Figure 2.5). Comparing Figures 2.4 and 2.5 shows how ECR has developed in recent years to accommodate changes in the market environment. It is not surprising that the Global Commerce Initiative (GCI) has been the instigator of the Global Scorecard in that one of its key objectives is to advocate the promulgation of common data and communications standards, including those pertaining to global Web exchanges.

Figure 2.4: ECR Improvement Concepts

Figure 2.5: ECR Concepts

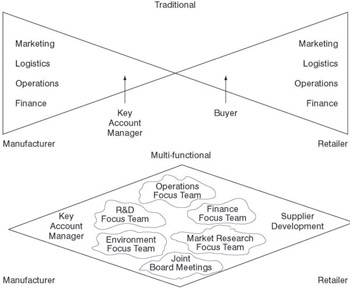

Retailers are becoming more sophisticated in their approach to demand and supply management, and there has been considerable progress in moving from a traditional organizational structure, the ‘bow tie’, to a multi-functional team structure (Figure 2.6) as relationships changed between retailers and their suppliers (Table 2.4). ECR conferences are replete with examples of how category performance has been improved through enhancing the consumer experience ‘in store’ by remerchandising traditional layouts. Such approaches are not only being adopted by major companies but also the small to medium sized retailers. Each year the Scottish Grocers Federation conference highlights the success of category planning between major snack and soft drink manufacturers and their convenience store customers. After all, these businesses have limited store space and depend heavily on impulse purchases.

Figure 2.6: Transformation of the Interface Between Manufacturer and Retailer

|

Current relationship |

Target relationship |

|---|---|

|

|

|

Source: Coopers and Lybrand, 1996 |

|

Although logisticians would prefer a consistent flow of product through the supply chain, tactical promotions remain a feature in many retailers’ marketing strategies. Research by Hoch and Pomerantz (2002) on 19 food product categories in 106 supermarket chains in the United States shows that price sensitivity and promotional responsiveness are much greater with high frequency ‘staple’ purchases. Compared with more specialist niche products, however, where greater variety and range built store traffic, staple products benefited from range reduction – a strategy which has been adopted by multinational FMCG manufacturers.

In order to integrate this demand-side planning with continuous replenishment, collaborative planning is necessary (see Figure 2.6). The main catalyst to fostering integration has been the VICS initiative on Collaborative Planning, Forecasting and Replenishment (CPFR), previously alluded to in the Quick Response section. VICS, a non-profit organization, drew its membership primarily from US non-food retailers and their suppliers until the late 1990s when the grocery sector embraced the CPFR model. For example, Wal-Mart and Warner-Lambert are usually cited as key partners in sales forecast collaboration in the early to mid- 1990s. The shift into grocery is hardly surprising in view of Wal-Mart’s move into food through its supercentres in the United States and its overseas acquisitions of grocery businesses such as Asda in the UK.

By the late 1990s, VICS had produced a nine-step generic model bringing together elements of ECR initiatives – the development of collaborative arrangements, joint business plans, shared sales forecasts, continuous replenishment from orders generated. GCI has been the key player in globalizing this US initiative through collaboration between VICS, ECR Europe, other ECR country associations and global exchange groups. The CPFR sub-committees now have international co-chairs as the globalization of CPFR had grown to 62 members in 2002.

Although the tenets of CPFR have been established, the implementation of the model remains patchy and like ECR initiatives will tend to focus on ‘quick wins’ where measurable profit enhancement or cost savings can be achieved. Most pilot schemes have involved a handful of partners dealing with specific categories. Companies come from a variety of technical platforms and ‘cultures’ of collaboration. Indeed, the likes of Wal-Mart, Tesco and Sainsbury with their own intranet exchanges could actually impede more universal adoption of common standards!

Overall, however, to implement CPFR it is a prerequisite that a close working relationship has been fostered between trading partners in order to invest the necessary human resources to develop joint plans to generate real-time forecasts. In our discussion earlier on promotional activity, it was clear that demand is more volatile with price promotions, in addition to seasonal and event planning. CPFR would generate greater benefits in these heavily promoted channels where over-stocks or out-ofstocks are more evident than in high volume, staple, frequently purchased items where demand is more predictable.

The Role of Logistics Service Providers (Lsps)

Third-party logistics providers are ‘the missing piece in the ECR puzzle’ (Rozemund, quoted in Mitchell, 1997: 60). So much has been written on relationships throughout the supply chain, especially manufacturer– retailer relationships, but the actual physical process of getting the products to the stores has been largely ignored. Yet the decision on whether to outsource or not is very similar to the ‘make or buy’ decision in operations management. Although we will focus our attention on logistics outsourcing here, ECR draws a range of third-party activities into the equation. As companies move to become virtual organizations and concentrate upon their core competencies, relationships will be formed with IT providers, banks, advertising agencies and security companies in addition to logistics service firms.

The theoretical work on outsourcing is based on the seminal work of Williamson (1979, 1990) on transaction cost analysis, which has been further developed by Reve (1990) to a contractual theory of the firm, and applied by Cox (1996) and Aertsen (1993) to Supply Chain Management. In essence, these authors have revised Williamson’s ideas on high asset specificity and ‘sunk costs’ to the notion of ‘core competencies’ within the firm. Therefore, a company with core skills in logistics would have high asset specificity and would have internal contracts within the firm. Complementary skills of medium asset specificity skills would be outsourced on an ‘arms’ length’ contract basis.

Conceptual research tends to establish the context within which the outsourcing decision is taken. Much of this work emphasized that long- term relationships or alliances are being formed between purchasers and suppliers of logistical services (Bowerson, 1990; Gardner and Cooper, 1994; McKinnon, 2003). Empirical work on the use of logistics service providers and their relationship with purchasing companies has tended to be biased towards surveys of US manufacturing companies with regard to the provision of both domestic and international outsourcing services (Gentry, 1996; Sink, Langley and Gibson, 1996; McGinnis, Kochunny and Ackerman, 1995; Lieb and Randall, 1996). Throughout the latter half of the 1990s and the early years of the millennium, Langley, Allen and Tyndal (2002) have undertaken annual reviews of third-party logistics in the United States involving a range of industrial sectors, including the retail sector. In 2002 the geographical scope of the survey was widened to include Western Europe and Asia.

UK research has been driven largely by surveys by consultants or contractors, for example, CDC (1988) and Applied Distribution (1990), with the period surveys of PE International (1990, 1993, 1996) being the most comprehensive. Academic surveys have been limited to Fernie’s exploratory work in the buying and marketing of distribution services in the retail market (Fernie, 1989, 1990) and two separate surveys on the role of dedicated distribution centres in the logistics network (Cooper and Johnston, 1990; Milburn and Murray, 1993).

These empirical surveys have shown that the contract logistics market has grown and the providers of these services have increased in status and professionalism. Logistics is no longer solely associated with trucking but also with warehousing, inventory control, systems and planning. However, the market is volatile and many of the reasons cited for contracting out such as cost, customer service and management expertise are also used to justify retention of the logistical service ‘in house’. There is an impression that companies enter some form of partnership but in many cases lip service is being paid to the idea.

In a survey of British retailers by the author in the mid-1990s it was shown that outsourcing was of marginal significance to many British retailers, which have a tendency to retain logistics services ‘in house’ (Fernie, 1999). Indeed, retail management was much more positive about the factors for continuing to do so than for contracting out such services. Clearly retailers not only wished to maintain control over the logistics functions but felt that their staff could provide customer service at a lower cost. As with other industrial sectors, transport was the most likely logistics activity to be contracted out. Despite the growth of the third- party market in the 1980s and 1990s, at that time a degree of saturation appeared to have been reached in that few companies expected to increased their proportion of contracting out in the future.

This has been borne out by the annual retail logistics surveys by the IGD, which has indicated a levelling off in expenditure in outsourcing of transport and warehousing by supermarket chains. Nevertheless, since the Fernie (1999) survey, trends in retail logistics have changed the nature of third-party support to focus more upon the primary network rather than the traditional RDC to store business. Retailers, seeking to reduce inventory at RDCs, have incorporated primary consolidation centres in their logistics network to increase vehicle fill and increase frequency of deliveries. The notion of ‘dedicated distribution’ is less relevant now than when RDCs were initially rolled out in the 1980s and 1990s. Vehicles no longer return empty to RDCs after delivering to stores but either pick up loads from suppliers or return packaging waste for recycling. Finally, factory gate pricing will take these initiatives a step further through the coordination of vehicle planning to minimize vehicle movements throughout the primary and secondary network.

All of these changes will offer opportunities to LSPs, although there will be winners and losers in this new contractual environment with a ratio- nalization of transport provision. Similar trends are evident in the clothing sector, which has come under intense price competition. In the early 2000s, the demerger of Arcadia led to outsourcing the logistics support to stores; more recently Matalan outsourced its logistics operation in 2003 and in order to save £20 million from its UK operation, Marks and Spencer continues to outsource but has rationalized its LSPs from five to two. It is currently reviewing its overseas logistics operation where savings of £100 million are expected to be achieved.

The outsourcing decision is a complex one, related to the size and historical evolution of the network. Companies with a long history of in- house logistics have ‘sunk costs’ within the organizations, equating with Williamson’s (1990) view on asset specificity. The contract relationship will be intra-organizational, that is between the retail and logistics departments in a company. Retail businesses with large, complex networks, however, have invariably developed relationships with logistics providers as they have moved into new geographical markets or new retail sectors. This has necessitated the use of complementary skills of medium asset specificity and the development of a range of contractual relationships of an inter-organizational nature (Cox, 1996).

This research showed that the transport function was most commonly outsourced, primarily because the core competencies required are of a residual nature with low asset specificity. Contracts are generally shorter and the relationship is more ‘arms’ length’ in nature, or what Cox (1996) classified as an adversarial leverage type of relationship.

The role of the outsourcing decision has to be seen within the context of a retailer’s corporate strategy at discrete moments in a company’s history. Acquisitions or demergers, expansion or withdrawal from markets can all influence logistical decisions. No two companies are the same, and invariably a third-party provider is utilized to solve a particular logistical problem pertaining to a retailer’s investment strategy. This ‘horses for

courses’ argument tends to support the work undertaken in the United States by Sink, Langley and Gibson (1996).

Conclusions

This chapter has illustrated the considerable research that has taken place into relationships through the supply chain. A background to the theoretical constructs underpinning buyer–seller relationships was given, drawing on research from the marketing and logistics literature.

The concepts of power and dependence, trust and commitment, cooperation and co-opetition were critically reviewed in the context of the retail sector. Much of the research on retailer–manufacturer relationships has focused on the concept of Quick Response and Efficient Consumer Response. The development of QR from its US origins to applications in the clothing sector in Japan was discussed to illustrate that QR has less relevance in the ‘fast fashion’ Japanese market. ECR, by contrast, has been embraced in numerous markets throughout the world. The harmonization of the VICS model of collaborative planning forecasting and replenishment (CPFR) with ECR Europe initiatives bodes well for future collaborative initiatives in the grocery supply chain.

Finally, the role of third-party logistics providers to instigate these strategic objectives was discussed. As the retail logistics environment changes – greater internationalization, integration of primary and secondary networks and reverse logistics – LSPs can capitalize on these marketing opportunities.

References

Aertsen, F (1993) Contracting out the physical distribution function: a trade-off between asset specificity and performance measurement’, International Journal of Physical Distribution and Logistics Management, 23 (1), pp 26–28

Applied Distribution (1991) Third Party Contract Distribution, Applied Distribution Ltd, Maidstone

Azuma, N (2001) The reality of Quick Response (QR) in the Japanese fashion sector and the strategy ahead for the domestic SME apparel manufacturers, pp 11–20 in Logistics Research Network 2001 Conference Proceedings, Heriot-Watt University, Edinburgh

Bowerson, P J (1990) The strategic benefits of logistics alliances, Harvard Business Review, 68 (4), pp 36–45

Brandenburger, A and Nalebüff, B (1996) Co-opetition, Doubleday, New York

Christopher, M (1997) Marketing Logistics, Butterworth Heinemann, Oxford

Christopher, M (1998) Logistics and Supply Chain Management, 2nd edn, Financial Times, London

Christopher, M and Juttner, U (2000) Achieving supply chain excellence: the role of relationship management, International Journal of Logistics: Research and Application, 3 (1), pp 5–23

Christopher, M and Peck, H (1998) Fashion logistics, in Logistics and Retail Management, ed J Fernie and L Sparks, Kogan Page, London Christopher, M and Peck, H (2003) Marketing Logistics, Butterworth-Heinemann, Oxford

Competition Commission (2000) Supermarkets: A report on the supply of groceries from multiple stores in the United Kingdom, Competition Commission, London

Cooper, J and Johnston, M (1990) Dedicated contract distribution: an assessment of the UK market place, International Journal of Physical Distribution and Logistics Management, 20 (1), pp 25–31

Coopers and Lybrand (1996) European Value Chain Analysis Study: Final report, ECR Europe, Utrecht

Corporate Development Consultants (CDC) (1988) The UK Market for Contract Distribution, CDC, London

Cox, A (1996) Relationship competence and strategic procurement management: towards an entrepreneurial and contractual theory of the firm, European Journal of Purchasing and Supply Management, 2 (1), pp 57–70

Daparin, G P and Hogarth-Scott, S (2003) Are co-operation and trust being confused with power? An analysis of food retailing in Australia and the UK, International Journal of Retail and Distribution Marketing, 31 (5), pp 256–67

Daugherty, P J, Stank, T P and Rogers, D S (1996) Third-party logistics service providers: purchasers’ perceptions, International Journal of Purchasing and Materials Management, 32 (2), pp 7–16

Fernie, J (1989) Contract distribution in multiple retailing, International Journal of Physical Distribution and Materials Management, 20 (1), pp 1–35 Fernie, J (1990) Third party or own account – trends in retail distribution, chapter 5 in Retail Distribution Management, Kogan Page, London

Fernie, J (1994) Quick response: an international perspective, International Journal of Physical Distribution and Logistics Management, 24 (6), pp 38–46 Fernie, J (1998) Relationships in the supply chain, in Logistics and Retail Management, ed J Fernie and L Sparks, Kogan Page, London

Fernie, J (1999) Outsourcing distribution in UK retailing, Journal of Business Logistics, 21 (2), pp 83–95

Fiddis, C (1997) Manufacturer–Retailer Relationships in the Food and Drink Industry: Strategies and tactics in the battle for power, FT Retail and Consumer Publishing, Pearson Professional, London

Finnie, T A (1992) Textiles and apparel in the USA: restructuring for the 1990s, Special Report no 2632, Economist Intelligence Unit, London

Forza, C and Vinelli, A (1996) An analytical scheme for the change of the apparel design process towards quick response, International Journal of Clothing Science and Technology, 8 (4), pp 28–43

Forza, C and Vinelli, A (1997) Quick Response in the textile-apparel industry and the support of information technologies, Integrated Manufacturing Systems, 8 (3), pp 125–36

Forza, C and Vinelli, A (2000) Time compression in production and distribution within the textile–apparel chain, Integrated Manufacturing Systems, 11 (2), pp 138–46

French, J R P and Raven, B H (1959) The basis of social power, in Studies in Social Power, ed P Cartwright, pp 150–67, Institute for Social Research, University of Michigan, Ann Arbor, Michigan

Gardner, J and Cooper, M (1994) Partnerships: a natural evolution in logistics, Journal of Business Logistics, 13 (2), pp 121–44

Gentry, J J (1996) Carrier involvement in buyer–seller supplier strategic partnerships, International Journal of Physical Distribution and Logistics Management, 26 (3), pp 14–25

Giunipero, L C, Fiorito, S S, Pearcy, D H and Dandeo, L (2001) The impact of vendor incentives on Quick Response, International Review of Retail, Distribution and Consumer Research, 11 (4), pp 359–76

Hart, S (2003) Marketing Changes, Thomson Learning, London

Hines, T (2001) From analogue to digital supply chain: implications for fashion marketing, in Fashion Marketing, Contemporary Issues, ed P Hines and M Bruce, Butterworth Heinemann, Oxford

Hoch, S J and Pomerantz, J J (2002) How effective is category management?, ECR Journal, 2 (1), pp 26–32

Hogarth-Scott, S and Parkinson, S T (1993) Retailer–supplier relationships in the food channel – a supplier perspective, International Journal of Retail and Distribution Management, 21 (8), pp 12–19

Hunter, A (1990) Quick Response in Apparel Manufacturing: A survey of the American scene, Textile Institute, Manchester

Ko, E, Kincade, D and Brown, J R (2000) Impact of business type upon the adoption of quick response technologies: the apparel industry experience, International Journal of Operations and Production Management, 20 (9), pp 1,093–111

Kumar, N (1996) The power of trust in manufacturer–retailer relationships, Harvard Business Review, 74 (6), pp 92–106

Kurt Salmon Associates (KSA) (1997) Quick Response: Meeting customer needs, KSA, Atlanta, GA

Langley, C J, Allen, G R and Tyndal, G R (2002) Third-Party Logistics Study, Georgia Institute of Technology, Atlanta, Georgia

Lieb, R and Randall, M (1996) A comparison of third party logistics services by large American manufacturers, 1991, 1994 and 1995, Journal of Business Logistics, 17 (1), pp 303–20

Lowson, B (1998) Quick Response for Small and Medium-Sized Enterprises: A feasibility study, Textile Institute, Manchester

Lowson, B, King, R and Hunter, A (1999) Quick Response: Managing supply chain to meet consumer demand , Wiley, New York

McGinnis, M A, Kochunny, C M and Ackerman, K B (1995) Third party logistics choice, International Journal of Logistics Management, 6 (2), pp 93–102

McGrath, M (1997) A Guide to Category Management, IGD, Letchmore Heath

McKinnon, A C (2003) Outsourcing the logistics function, in Global Logistics and Distribution Planning, ed D Waters, Kogan Page, London METI (2002) Seni Sangyo no Genjo to Seisaku Taiou (The Current Status of the Japanese Textile Industry and the Political Responses), METI (Japanese Ministry of Economy, Trade, and Industry; formerly MITI), Tokyo

Milburn, J and Murray, W (1993) Saturation in the market for dedicated contract distribution, Logistics Focus, 1 (5), pp 6–9

Mitchell, A (1997) Efficient Consumer Response: A new paradigm for the European FMCG sector, FT Retail and Consumer Publishing, Pearson Professional, London

MITI (1993) Seni Vision (Textile Vision), MITI (Japanese Ministry of International Trades and Industries), Tokyo

MITI (1995) Sekai Seni Sangyo Jijo (MITI World Textile Report), MITI, Tokyo MITI (1999) Seni Vision (Textile Vision), MITI, Tokyo

Ogbonna, E and Wilkinson, B (1996) Inter-organisational power relations in the UK grocery industry: contradictions and developments, International Review of Retail, Distribution and Consumer Research, 6 (4), pp 395–414

O’Malley, L (2003) Relationship marketing, in Marketing Changes, ed S Hart, pp 125–45, Thomson, London

PE International (1990) Contract Distribution in the UK: What the customers really think, PE International, Egham

PE International (1993) Contracting-out or Selling out?, PE International, Egham

PE International (1996) The Changing Role of Third Party Logistics: Can the customer ever be satisfied?, PE International, Egham

Piore, M J and Sabel, C F (1984) The Second Industrial Divide: Possibilities for prosperity, Basic Books, New York

Quick Response Services (1995) Quick Response Services for Retailers and Manufacturers, Quick Response Services, Richmond, CA Reve, T (1990) The firm as a means of internal and external contracts, in

The Firm as a Nexus of Treaties, ed M Aoki et al, pp 136–88, Sage, London Riddle, E J, Bradbard, D A, Thomas, J B, and Kincade, D H (1999) The role of electronic data interchange in Quick Response, Journal of Fashion Marketing and Management, 3 (2), pp 133–46

Scarso, E (1997) Beyond fashion: emerging strategies in the Italian clothing industry, Journal of Fashion Marketing and Management, 1 (4), pp 359–71

Sink, H L, Langley, C J and Gibson, B J (1996) Buyer observations of the US third-party logistics market, International Journal of Physical Distribution and Logistics Management, 26 (3), pp 38–46

Taplin, I M and Ordovensky, J F (1995) Changes in buyer–supplier relationships and labor market structure: evidence from the United States, Journal of Clothing Technology and Management, 12, pp 1–18

VICS (1998) Collaborative Planning, Forecasting, and Replenishment Voluntary Guidelines, VICS (Voluntary Interindustry Commerce Standards Association), Lawrenceville, NJ

Waters, D (ed) (2003) Global Logistics and Distribution Planning, Kogan Page, London

Williamson, O E (1979) Transaction-cost economics: the governance of contractual relations, Journal of Law and Economics, 22, pp 232–61

Williamson, O E (1990) The firm as a nexus of treaties: an introduction, in The Firm as a Nexus of Treaties, ed M Aoki et al, Sage, London

Preface

- Retail Logistics: Changes and Challenges

- Relationships in the Supply Chain

- The Internationalization of the Retail Supply Chain

- Market Orientation and Supply Chain Management in the Fashion Industry

- Fashion Logistics and Quick Response

- Logistics in Tesco: Past, Present and Future

- Temperature-Controlled Supply Chains

- Rethinking Efficient Replenishment in the Grocery Sector

- The Development of E-tail Logistics

- Transforming Technologies: Retail Exchanges and RFID

- Enterprise Resource Planning (ERP) Systems: Issues in Implementation

EAN: 2147483647

Pages: 119

- Measuring and Managing E-Business Initiatives Through the Balanced Scorecard

- A View on Knowledge Management: Utilizing a Balanced Scorecard Methodology for Analyzing Knowledge Metrics

- Measuring ROI in E-Commerce Applications: Analysis to Action

- Managing IT Functions

- The Evolution of IT Governance at NB Power