A View on Knowledge Management: Utilizing a Balanced Scorecard Methodology for Analyzing Knowledge Metrics

A View on Knowledge Management Utilizing a Balanced Scorecard Methodology for Analyzing Knowledge Metrics

Alea Fairchild

Vesalius College/Vrije Universiteit Brussel (VUB), Belgium

Copyright 2004, Idea Group Inc. Copying or distributing in print or electronic forms without written permission of Idea Group Inc. is prohibited.

Abstract

IT professionals who want to deploy foundation technologies such as groupware, CRM or decision support tools, but fail to justify them on the basis of their contribution to Knowledge Management, may find it difficult to get funding unless they can frame the benefits within a Knowledge Management context. Determining Knowledge Management's pervasiveness and impact is analogous to measuring the contribution of marketing, employee development, or any other management or organizational competency. This chapter addresses the problem of developing measurement models for Knowledge Management metrics and discusses what current Knowledge Management metrics are in use, and examines their sustainability and soundness in assessing knowledge utilization and retention of generating revenue. The chapter discusses the use of a Balanced Scorecard approach to determine a business-oriented relationship between strategic Knowledge Management usage and IT strategy and implementation.

Introduction

"Knowledge has become the key economic resource and the dominate — and perhaps even the only- source of competitive advantage." Peter Drucker, Managing in a Time of Great Change (1995)

Knowledge Management may be defined as a set of processes for transferring intellectual capital to value - processes such as innovation and knowledge creation and knowledge acquisition, organization, application, sharing, and replenishment (Knapp, 1998). Enterprises work in generating value from knowledge assets by sharing them among employees, departments and even with other companies in an effort to devise best practices.

From the point of view of information technology (IT) investment, it is important to note that the definition itself says nothing about technology; while Knowledge Management is often facilitated by IT technology, by itself it is not Knowledge Management.

"Now that knowledge is taking the place of capital as the driving force in organizations worldwide, it is all too easy to confuse data with knowledge and information with information technology." Peter Drucker, Managing in a Time of Great Change (1995)

The definition of knowledge is a complex and controversial one, and 'knowledge' can be interpreted in many different ways. Much of the Knowledge Management literature defines knowledge in broad terms, covering basically all the "software" of an organization. This involves the structured data, patents, programs and procedures, as well as the more intangible knowledge and capabilities of the people. It may also include the way that organizations function, communicate, analyze situations, come up with novel solutions to problems and develop new ways of doing business. Knowledge Management in an organization can also involve issues of culture, custom, values and skills as well as the enterprise's relationships with its suppliers and customers. Knowledge Management is a strategic, systematic program to capitalize on what an organization "knows" (Knapp, 1998).

Managerial interest in Knowledge Management stems from a number of economic facts about knowledge utilization in today's environment. These facts are shown in Figure 1.

- Long-run shifts in advanced industrial economies that have led to the increasingly widespread perception of knowledge as an important organizational asset.

- The rise of occupations based on the creation and use of knowledge.

- Theoretical developments -- for example, the resource-based view of the firm -- which emphasize the importance of unique and inimitable assets such as tacit knowledge.

- The convergence of information and communication technologies, and the advent of new tools such as Intranets and groupware systems.

- A new wave approach to packaging and promoting consultancy services in the wake of the rise and fall of Business Process Reengineering (BPR).

Figure 1: Economic Reasons for the Interest in Knowledge Management (KPMG Consulting, 2000)

- Long-run shifts in advanced industrial economies which have led to the increasingly widespread perception of knowledge as an important organizational asset.

- The rise of occupations based on the creation and use of knowledge.

- Theoretical developments - for example, the resource-based view of the firm — which emphasize the importance of unique and inimitable assets such as tacit knowledge.

- The convergence of information and communication technologies, and the advent of new tools such as Intranets and groupware systems.

- A new wave approach to packaging and promoting consultancy services in the wake of the rise and fall of Business Process Reengineering (BPR).

Organizational requirements for Knowledge Management involve leveraging intellectual capital, not just retaining it, which requires attention to what have been recognized as "knowledge enablers", i.e., structures and attributes that must be in place for a successful Knowledge Management program. Besides technology, these enablers include content, learning, culture and leadership (KPMG Consulting, 2000). In order to measure Knowledge Management, some attention needs to be paid to measurement of the enabling factors as well.

The chapter discusses two possible sets of metrics, containing both qualitative and quantitative components, to aid management in understanding Knowledge Management initiatives and the necessary IT investments in relation to the company's strategic direction. This chapter addresses the question: What set of industry standard metrics, containing both hard and soft elements, can be adapted for use in Knowledge Management initiatives?

The chapter first explores literature on current Knowledge Management metrics. It then examines, from published research, how Knowledge Management is viewed in organizations to examine the sustainability and soundness in metrics that assess knowledge utilization and retention of generating revenue. It then creates an extension of the Balanced Scorecard framework in terms of two possible perspectives, so as to address Knowledge Management metrics. The conclusion of the chapter ties the Knowledge Management perspectives suggested in this research to the original intent of a Balanced Scorecard so as to show the relationship to strategy.

Background on Knowledge Management

How is Knowledge Management Measured?

A number of Knowledge Management thought leaders, such as Larry Prusak and Thomas Davenport, have stated a belief that it is impossible to develop direct, meaningful measures of knowledge assets. They believe it is possible to measure only the outputs of knowledge, given that knowledge is, by definition, intangible and therefore unobservable. But by developing an understanding of what makes a "unit" of knowledge, one might be able to create the necessary relationship between knowledge and the value it creates for the organization.

Although the focus on corporate culture and organizational change may extend the timeframe for a Knowledge Management program, only measurable benefits justify increased duration and cost in the eyes of senior management. Those benefits include better preparation for implementation and the ability to take advantage of existing technology.

Knowledge Management investments are thus likely to include the extension of existing enterprise software to eliminate barriers between transactional applications and repositories of corporate knowledge. Increasingly, companies will exploit corporate knowledge and provide it to users within the context of business problems, a more effective alternative to simply storing this content in and accessing it from a centralized knowledge repository (Dyer & McDonough, 2001). Given that there is no clear single activity that is Knowledge Management, it is more how and when Knowledge Management is integrated into organizational activities that can be measured.

In general, however, intellectual and knowledge-based assets fall into one of two categories: explicit or tacit. Included among the former are assets such as patents, trademarks, business plans, marketing research and customer lists. Generally, explicit knowledge consists of anything that can be documented, archived and codified, often with the help of IT. Much harder to grasp is the concept of tacit knowledge, or the know-how contained in people's heads. The challenge inherent with tacit knowledge is figuring out how to recognize, generate, share and manage it. While IT in the form of e-mail, groupware, instant messaging and related technologies can help facilitate the dissemination of tacit knowledge, identifying tacit knowledge in the first place is a major hurdle for most organizations (Surmacz & Santosus, 2001).

A recent Platinum Technologies study found that only 20% of Knowledge Management programs have used some form of metrics on how business performance is influenced. This may be that traditionalist management who use ROI for calculations have to find an appropriate equation for Knowledge Management (Shand, 1999). Platinum Technologies developed a method that was two parts hard, or quantifiable, measurement and one part soft, or more qualitative, measurement. By consolidating and better managing the different delivery channels for sales and marketing, Platinum significantly reduced the costs of maintaining and distributing collateral. This represents a hard and indisputable measure. The other third (the "soft" measure) resulted from increases in sales productivity, a measure with less clear impact on revenue. Senior management appreciated the difference between these hard and soft measures, especially the lesser emphasis on a metric that could be easily contested. This appreciation needs to be considered when assessing harder metric methods like return on investment (ROI) (Shand, 1999).

When is Knowledge Management Measured?

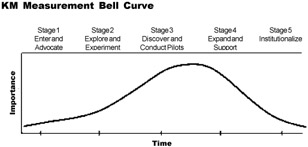

Figure 2 emerged from observing the numerous organizations that participated in an American Productivity and Quality Center (APQC) project (2001) and how they measure the value of Knowledge Management. During its 2000 consortium learning forum entitled 'Successfully Implementing Knowledge Management', APQC focused on how some of the most advanced early Knowledge Management adopters implement a Knowledge Management initiative, mobilize resources, create a business case, and measure and evolve their Knowledge Management programs. This multi-client benchmarking project helped APQC and project participants identify measurement approaches, specific measures in use, and how measures impact and are impacted by the evolution of Knowledge Management.

Figure 2: APQC Project

In the earliest stages of Knowledge Management implementation, formal measurement rarely takes place, nor is it required (APQC, 2001). As Knowledge Management becomes more structured and widespread and companies move into Stages Two, Three, and Four, the need for measurement steadily increases. As Knowledge Management becomes institutionalized — a way of doing business — the importance of Knowledge Management-specific measures diminishes, and the need to measure the effectiveness of knowledge-intensive business processes replaces them.

According to the APQC, the key is to begin to ensure that direct business value is perceived by the organization as a result of the knowledge-enabling projects. During its 2000 consortium learning forum entitled 'Successfully Implementing Knowledge Management', APQC focused on how some of the most advanced early Knowledge Management adopters implement a Knowledge Management initiative, mobilize resources, create a business case, and measure and evolve their Knowledge Management programs. This multi-client benchmarking project helped APQC and project participants identify measurement approaches, specific measures in use, and how measures impact and are impacted by the evolution of Knowledge Management.

The APQC Knowledge Management Measurement Bell Curve can be seen to parallel the five stages of the IT Balanced Scorecard (BSC) Maturity Model developed by Van Grembergen and Saull (2000), in that as the use of Knowledge Management matures in the organization, defined and managed measurement processes develop and become linked to business process cycles. The Van Grembergen and Saull (2000) IT BSC Maturity Model highlights five maturity levels (Initial, Repeatable, Defined, Managed and Optimized) to classify to what extent the IT BSC Maturity Model is integrated into the strategic and operational planning and review systems of the business and IT.

As seen from the APQC data, it is important to establish a mechanism to capture the hard and soft lessons learned in the Knowledge Management pilots with their initial IT investments, as these will be the building blocks for the later Knowledge Management implementations (APQC, 2001).

Challenges in Developing Knowledge Management Metrics

Knowledge Management Diversity of Practice

The economic facts listed in the Introduction section may help to explain the breadth of interest in Knowledge Management ranging across many different industrial sectors. They also can help to explain the diversity in the actual practices which have been labeled as Knowledge Management (KPMG Consulting, 2000). Although such practices share a common interest in targeting knowledge rather than information or data, they tend to perform distinctively different functions depending on the business context. Therefore, measuring the impact of these different functions on the business potentially requires different approaches.

One may distinguish between at least four different types of Knowledge Management (Business Process Resource Centre, 2001; Sveiby, 2001a):

- Valuing Knowledge. This approach is of interest in consulting firms and financial institutions — for example, the Skandia organization — and in management accounting areas. Knowledge is viewed as 'intellectual capital', and the focus is on quantifying and recognizing the value of the organization's knowledge-base. An example of this approach would be PLS-Consult in Denmark, who categorizes customers according to value of knowledge contribution to the firm and follows up in its management information system.

- Exploiting Intellectual Property. This approach appeals to firms with a strong science and R&D base — typified by a number of pharmaceutical firms, the Buckman Labs organization, and so on — which are looking beyond the conventional approach based on patents, etc. to more effective ways of tapping into the commercial value of their existing knowledge-base.

An example of this approach would be the development of the Boeing 777, which was the first "paperless" development of aircraft. It included customers in design teams, with more than 200 teams with a wide range of skills who both designed and constructed sub parts, rather than the usual separated organization of design team and construction team. Suppliers world-wide used the same digital databases as Boeing.

- Capturing Project-Based Learning. As firms increasingly move towards innovation and project-based organization, many are recognizing the need to capture the learning from individual projects and make it available throughout the organization. Consultancies, professional service firms, aerospace companies, etc., are in the vanguard of developing systems to codify and communicate such knowledge. The client who initiated this research effort also looks at Knowledge Management in this respect.

An example of this approach can be seen in the use of Knowledge Management by firms such as McKinsey and Bain & Co. These two management consulting firms have developed 'knowledge databases' that contain experiences from every assignment, including names of team members and client reactions. Each team must appoint a 'historian' to document the work.

- Managing Knowledge Workers. The shift towards knowledge work in many sectors creates problems for traditional ways of managing and motivating employees. In many firms, Knowledge Management reflects managers' desire to increase the productivity of knowledge workers, breaking down some of the barriers to knowledge-sharing which are associated with 'professionalism' (BPRC, 2001). An example of this approach can be seen at Analog Devices in the US. CEO Ray Stata initiated a breakdown of functional barriers and competitive atmosphere and created a collaborative knowledge sharing culture from the top down. The company encourages a 'community of inquirers' rather than a 'community of advocates'.

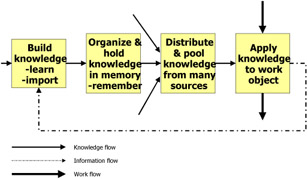

Why the different methods of viewing Knowledge Management is important is related to the knowledge, information and work flows associated with each type of Knowledge Management, as shown in Figure 3.

Figure 3: Four Stages of Knowledge Transition (Wiig, 1997)

Knowledge Management and IT Investment

The impact of Knowledge Management on IT investment can be related to the effect that each Knowledge Management initiative will have on increased costs of deployed services and technology tools. Based on a 2001 survey of 566 respondents done together by KM magazine and market research firm IDC, these survey results estimate that an average Knowledge Management budget will increase from $632,000 in 2000 to more than $1 million in 2002. These figures fall lower than expected, according to IDC, because two-fifths of the respondents represented companies with 500 or fewer employees, which shows the pervasiveness of the Knowledge Management concept into the reaches of the small and medium size businesses. Past data that emphasized larger companies showed an average budget of $2.7 million in 2000.

IDC believes from this survey that the budgets specifically designated for "Knowledge Management" initiatives decrease as these efforts become part of other technology or business process investments (Dyer & McDonough, 2001). For example, a company may perceive itself as investing in a customer service solution, though one with significant Knowledge Management capability, rather than categorize this investment as a Knowledge Management initiative. This again shows a need for measuring Knowledge Management and associated IT investment in a way to show its role in the organizational structure, benefiting business processes.

Measuring these roles via the Balanced Scorecard approach has already been established for evaluating IT and its investments, as Gold (1992) and Willcocks (1995) have already indicated in a conceptual manner and that has been further developed by Van Grembergen and Van Bruggen (1997), Van Grembergen and Timmerman (1998) and Van Grembergen (2000). Extending this Balanced Scorecard approach to the Knowledge Management environment would assist companies in understanding the use of Knowledge Management in relation to their knowledge capital resources, including IT implementation.

Connection between Knowledge Management Metrics Development and a Business Process View of Knowledge Management

Irrespective of the terms used, the practical management objectives of measuring Knowledge Management are similar: to find out how well the organization has converted human capital (individual learning/team capabilities) to structural capital (organizational knowledge or 'what is left when people go home', such as documented processes and knowledge bases) and thereby moved from tacit to explicit knowledge, and reduced the risk of losing valuable knowledge if people leave the organization. Loss of 'corporate memory' as a result of downsizing is one of the prime reasons given for adopting formal Knowledge Management practices. Other factors often mentioned include global competition and the pace of change; organizations see Knowledge Management as a means of avoiding repetition of mistakes, reducing duplication of effort, saving time on problem-solving, stimulating innovation and creativity, and getting closer to their customers (Corrall, 1999).

For all the interest and money spent on Knowledge Management there seems to be relatively few attempts to actually quantify the impact and results in business terms. The rationale is that knowledge exists in the context of its use (Svoika, 2001). Superior Knowledge Management frees companies to operate on fewer assets, collect their cash faster and have less volatility. The challenge is to make sure that the scope and the goal of the process is clear and focused, by providing a method to display indicators that measure objectives and are focused on the mission as set by the management. Given that Knowledge Management requires a mix of technical, organizational and interpersonal skills, the mix and emphasis varies according to responsibilities, but everyone involved needs to be able to understand the business and communicate business needs effectively, one approach to do this for Knowledge Management could be the Balanced Scorecard.

Van Grembergen and Timmerman (1998) and Martinsons, Davison and Tse (1999) were some of the first to have suggested that the Balanced Scorecard can be the foundation for the strategic management of information systems in organizations. Martinsons et al. (1999) use the Balanced Scorecard metrics to guide attainment of efficiency and effectiveness not only of information systems development but also of the use of the resulting information systems products in the operation of the business. They propose adaptations of the Balanced Scorecard framework based on the premise that IT is essentially an internal support function within an organization in contrast to the original framework, which focused on the impact of the business on the external market. The same analogy might be used for Knowledge Management, given that knowledge supports the activities of the organization.

Possible Solution of Utilizing Balanced Scorecard to Knowledge Management Metrics

Rationale for Balanced Scorecard in Knowledge Management

In their book, The Balanced Scorecard, Kaplan and Norton (1996) set forth a hypothesis about the chain of cause and effect that leads to strategic success. Kaplan and Norton (1996) have introduced the Balanced Scorecard at an enterprise level. Their fundamental premise is that the evaluation of a firm should not be restricted to a traditional financial evaluation but should be supplemented with measures concerning customer satisfaction, internal processes and the ability to innovate. Kaplan and Norton (1996) distinguish Financial, Internal, Customer, and Learning and Growth perspectives on organizational processes essential to an overall strategy. In looking at the original Kaplan and Norton (1996) implementation, Knowledge Management clearly fits within, if it does not define, the Learning and Growth aspect of their framework. If this is true, Knowledge Management outputs will impact on other processes. This is one reason why the significance in measuring Knowledge Management benefits or costs to other processes in organizations is an important area for extending the present Kaplan and Norton work (Firestone, 1998). Managers can track measures as they work toward their objectives, and measurement metrics aid in showing how to build internal capacity, such as human capital, tacit knowledge, and a knowledge culture. And a metrics framework keeps measures from being ad hoc, providing a reference point for Knowledge Management measurement after an implementation.

Use of Perspectives in Knowledge Management

Perhaps the key to proper initiatives and drivers is selecting the right perspectives, to use the Kaplan and Norton phrase, to view the interaction between Knowledge Management and the organizational strategy. This paper suggests that there might be two unique approaches to perspectives that would enhance the measurement of Knowledge Management in the organization.

First Approach. The first approach would be to use the different types of capital available in an organization, as shown in Figure 4, to be the four different scorecard perspectives of how Knowledge Management is leveraged in the organization. This approach is already in use in areas such as the US government, who is empowered to these Knowledge Management initiatives by the Clinger-Cohen Act of 1996 (Public Law 104–106), formerly known as the IT Management Reform Act. This Act requires CIOs in government to focus on the core competencies which represent skills and knowledge needed for effective mission support using information technologies. The four capitals which make up a knowledge-centric organization (KCO) are (Neilson, 2000):

- Human capital is all individual capabilities, the knowledge, skill and experience of the employees and managers.

- Intellectual capital includes the intangibles such as information, knowledge and skills that can be leveraged by an organization to produce an asset of equal or greater importance than land, labor and capital.

- Structural capital includes the processes, structures and systems that a firm owns less its people.

- Social capital is the goodwill resulting from physical and virtual interchanges between people with like interests and who are willing to share ideas within groups who share their interests.

Figure 4: Leveraging Knowledge Management with Balanced Scorecard

The dynamic mixing of human, intellectual, social and structural capital provides the fuel for creating and using knowledge. As retention and recruitment are major concerns in both public and private industry, an organization's success in leveraging its knowledge capital will ensure an organization remains competitive. The four capitals shown in the diagram can be directly related to the traditional Balanced Scorecard method in the following manner, shown in Table 1.

|

Balanced Scorecard Perspective |

Generic Measures |

Intellectual Capital Perspective |

Generic Measures |

|---|---|---|---|

|

Financial |

ROI, EVA |

Intellectual |

A wide variety of measures exist. See Table 2. |

|

Customer |

Satisfaction, retention, market and account share |

Social |

Social capital was originally defined and measured by the World Bank in terms that related entirely to density of horizontally organized social networks, subsequent investigations have resulted in complicating any such straightforward measurement. A variety of measures exist, one interesting one from Cap Gemini Ernst & Young and Henley College is called the KOPE survey. This covers the following categories: Knowledge Management strategy and link to business (K), organizational and cultural enablers (O), process enablers (P) and enabling technologies (E). For each of these categories there are between 10 and 13 dimensions. The survey has been designed to allow organizations to identify strengths and weaknesses in their Knowledge Management practices (Truch, 2001). |

|

Internal |

Quality, response time, cost and new product introductions |

Structural |

Andriessen and Tiessen's (2000) Value Explorer™ is an accounting methodology proposed by KPMG for calculating and allocating value to 5 types of intangibles: (1) Assets and endowments, (2) Skills & tacit knowledge, (3) Collective values and norms, (4) Technology and explicit knowledge, (5) Primary and management processes. |

|

Learning and Growth |

Employee satisfaction, IS availability |

Human |

From the work of Jac Fitz-Enz (1994), Human Capital Intelligence sets of human capital indicators are collected and benchmarked against a database. Similar to HRCA (Johansson, 1996), which calculates the hidden impact of HR related costs that reduce a firm's profits. |

|

Authors |

Name of Measurement |

Description |

|---|---|---|

|

Edvinsson and Malone (1997) |

Skandia Navigator™ |

Intellectual capital is measured through the analysis of up to 164 metric measures (91 intellectually based and 73 traditional metrics) that cover five components: (1) financial, (2) customer, (3) process, (4) renewal and development, and (5) human. |

|

Lev (2001) |

Value Chain Scoreboard™ |

Matrix of non-financial indicators arranged into three categories according to the cycle of development: Discovery/Learning, Implementation, and Commercialization. |

|

Roos, Roos, Dragonetti and Edvinsson (1997) |

IC-Index™ |

Consolidates all individual indicators representing intellectual properties and components into a single index. Changes in the index are then related to changes in the firm's market valuation. |

|

Pulic (2000) |

Value Added Intellectual Coefficient (VAIC™) |

Measures how much and how efficiently intellectual capital and capital employed create value based on the relationship to three major components: (1) capital employed, (2) human capital, and (3) structural capital. |

|

Sveiby (1997) |

Intangible Asset Monitor |

Management selects indicators, based on the strategic objectives of the firm, to measure four major components of intangible assets: (1) growth, (2) renewal, (3) efficiency, and (4) stability. |

As seen in financial and other 'hard' measurements, when it comes to numbers, all sorts of measurements come out of the woodwork. Table 2 is a listing of various IC measurements compiled by Karl Erik Sveiby, one of the predominant academics in this field.

Edvinsson and Malone (1997) measure intellectual capital with an 'all-encompassing' reporting model. They assume that if enough aspects of intellectual capital can be captured, one can have a 'complete' understanding on the utilization. What is missing from their approach is an integrated framework to show how the indicators are related. This is where an approach such as Balanced Scorecard can be useful. However, Sveiby (1997) claims his Intangible Asset Monitor is a more suitable approach for Knowledge Management than Balanced Scorecard, based on its notion of a 'knowledge perspective' of a firm. Thus he believes his Intangible Asset Monitor becomes a more demanding option for a management team; to get the best value, one should start by redesigning the strategy to be more 'knowledge focused'. Both approaches are fine for firms such as consulting houses and other service-oriented industries that focus on utilizing human capital. It is difficult to assume that other firms will have been converted enough to Knowledge Management to be knowledge-centric in their strategy. Therefore, we turn to our other suggestion, using a resource-based management approach.

Second Approach. The other approach possible in viewing the role of Knowledge Management in organizational strategy via a Balanced Scorecard would be to use a resource management-based approach, focusing on intellectual capital resources combined with business processes of the organization. This is based on the work of Mouristen et al. (2001) at the Copenhagen Business School, using the work on intellectual capital balance statements of Sveiby (1997). Table 3 correlates this approach to the Balanced Scorecard perspectives of Kaplan and Norton (1992).

|

Balanced Scorecard Perspective |

Generic Measures |

Intellectual Capital Statements (Mouristen et al., 2001) |

Generic Measures |

|---|---|---|---|

|

Financial |

ROI, EVA |

Employees |

Measurement of intellectual capital, as discussed above in Table 3 |

|

Customer |

Satisfaction, retention, market and account share |

Customers |

Customer satisfaction with 'quality of service' and product, related to Knowledge Management efforts |

|

Internal |

Quality, response time, cost and new product introductions |

Processes |

Internal hours on Knowledge Management process improvement, average response times for information gathered using Knowledge Management |

|

Learning and Growth |

Employee satisfaction, IS availability |

Technology |

Investment in Knowledge Management technology, number of hits on Knowledge Management project web sites, employee satisfaction with Knowledge Management project sites |

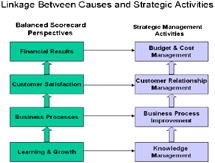

To tie the use of Knowledge Management into an organization, using either method, the relationship between Knowledge Management and organizational strategy must be understood and goals clearly defined. Figure 5 demonstrates the relationship between business processes in Balanced Scorecard terminology, and the use of Knowledge Management in an organization.

Figure 5: Knowledge Management Linkage— Cause and Activity

Correlating Knowledge Management Metrics to Strategy

Both of the suggested approaches above make use of such concepts as intellectual capital and the value of core processes in the organization. The rationale for this is that intellectual capital as a concept says more about the future earning capabilities of a company than any of the conventional performance measures we currently use (Roos, 1996). Kaplan and Norton (1996) discuss using Balanced Scorecard measures for assessing potential investment. In creating a mechanism that ties long-term objectives into measurable metrics, they claim that executives can see the relationship between investment and strategic plans. But should knowledge be considered a cost element, or a revenue generator? This is one challenge in using the Balanced Scorecard versus other mechanisms in industry. Until we view business processes in other ways than the traditional production function (input, output), approaches such as the Balanced Scorecard are still valid in the knowledge economy.

But there is also an element of debate of whether Balanced Scorecard mechanisms help promote the use of knowledge in organizations. Kaplan and Norton (1996) in their approach did not question the foundation of 'what constitutes a firm', but regard the notion of the firm as given by its strategy. They just want managers to take a more 'balanced view'. As they argue in their book (1996, p. 8): "The Balanced Scorecard complements financial measures of past performance with measures of the drivers of future performance. The objectives and the measures of the Scorecard are derived from an organization's vision and strategy." If Knowledge Management is not part of the firm's strategic view, then investment and management of intellectual assets will not take priority. Use of Knowledge Management requires firms to think about knowledge as a production element, but trends in Knowledge Management lead us to believe that knowledge will be viewed as a service economy, therefore with more intangible measurement. This is also true in the education field, where universities such as Manchester Metropolitan University's business school are examining how to measure their own use of Knowledge Management, and are exploring these two approaches discussed in the chapter as possible metric views.

Many corporations have not clearly articulated a need to manage knowledge. Of the 158 companies surveyed by the Conference Board (Beyond Knowledge Management: New Ways to Work and Learn, 2000), 80% had launched some kind of Knowledge Management activity, but only 15% had specific, stated Knowledge Management objectives and goals. Competitive necessity dictates that executives understand how Knowledge Management and knowledge sharing impact the bottom line, but many do not. KPMG Consulting reports that while most of those it surveyed understand that Knowledge Management can boost profits and reduce costs, less than 30% expected it to help increase their company's share price. The most important and useful metrics are those that directly inform the improvement of business performance and that can best be considered within the context of a learning process that embeds the metrics within the work process.

One Learning process, as an example, is that used by BP - Amoco (BP) as a central part of their Knowledge Management strategy — 'Learn Before, Learn During, Learn After'. Essentially BP - Amoco embeds Knowledge Management within the everyday work process by making it a normal part of doing business. At the beginning of any project they conduct a 'Peer Assist' (alternatively known as 'Prior Art'), where they get knowledgeable colleagues together to consider all that BP - Amoco knows about this particular subject. 'Learn During' involves a version of the US Army's well-known 'After Action Review' (AAR). BP - Amoco use the AAR after each 'identifiable event' rather than at the end of a project; thus it becomes a 'live' learning process that constantly informs the direction of the project. The third part is what BP - Amoco call a 'Retrospect', which is a team meeting designed to identify 'what went well', 'what could have gone better' and 'lessons for the future'.

By ensuring that time is made available within the actual project and that this learning process does not become extra work, BP - Amoco has managed to make it a normal part of doing business. The results have been real tangible business benefits visible in dollar terms that have turned around critics: "the Schiehallen oil field, a North Sea field considered too expensive to develop until a team spent six months pestering colleagues to share cost-saving tips. They were called wimps for not rushing out to 'make hole', but the learn-before-doing approach saved so much time on the platform (at $100,000 to $200,000 a day, not counting drilling costs) that they brought the field into production for $80 million less than anyone thought possible." Indeed, Tom Stewart recently stated about the CKO of BP: "Greenes is, as best I can figure, Knowledge Management's top moneymaker" (World Bank, 1999). This Learning Cycle then becomes the facilitating infrastructure for developing a process of Knowledge Management Metrics which allow the identification of real business value in each aspect of the necessary IT and other investments.

Summary

Measurement has always been perceived as a science of precision; however, the measurement practice in most organizations today is anything but precise. Indeed, the issues looked for in scorecards, such as customer and employee satisfaction, and in intellectual capital, tend to require less precision and entertain more interest in trends than in exact figures. Kaplan and Norton's (1996) cause-and-effect hypothesis could be essential to understanding Knowledge Management metrics in a way that the Balanced Scorecard prescribes. Although the Balanced Scorecard can form the foundation for organizational strategic success, it is, however, not sufficient in itself. Along with strategies, there must be initiatives, such as business process improvement efforts, to steer the organization in the right direction and improve Knowledge Management implementation.

At the heart of an ideal definition of knowledge capital is the creation and provision of 'value'. Without linkage to strategic initiatives reflected through forms of measurement or recording of value, whether simply anecdotal or more quantifiable, Knowledge Management might degenerate into superficial business management hype. A conscious effort in conceptualizing, designing and putting to practice metrics like the ones described above may, however, assist in realizing the true worth of Knowledge Management.

As regards IT investment in particular, information technology may help growth and the retention of organizational knowledge if care is taken to continuously recall that IT is only a part; corporate culture and work practices being equally relevant to the whole. Information technologies best suited for this purpose should be expressly designed with Knowledge Management and organizational capital in view. Thus, while technology can support Knowledge Management, it is not the starting point of a Knowledge Management program.

References

Andriessen & Tiessen (2000). Weightless weight - Find your real value in a future of intangible assets. Pearson Education London.

APQC. (2001). How to measure the value of Knowledge Management. Knowledge Management Review, March/April. Available online: http://www.apqc.org/free/articles/APQCKMR.pdf.

Business Process Resource Centre [BPRC]. (2001). Defining Knowledge Management. Warwick Business School, Business Process Resource Centre. Available online: http://bprc.warwick.ac.uk/Kmweb.html.

Corrall, S. (1999). Are we in the Knowledge Management business? Knowledge Management, 18. Available online: http://www.ariadne.ac.uk/issue18/knowledge-mgt/.

Drucker, P. F. (1995). Managing in a time of great change. New York: Truman Talley Books/Dutton.

Dyer & McDonough. (2001). The state of KM. Knowledge Management, (May). Available online: http://www.destinationkm.com/articles/default.asp?ArticleID=539.

Edvinsson, L., & Malone, M.S. (1997). Intellectual capital: Realizing your company's true value by finding its hidden brainpower. New York: Harper Business.

Firestone, J. (1998). Knowledge Management metrics development: A technical approach. Executive Information Systems, Inc. White Paper No. Ten, (June). Available online: http://www.dkms.com/dkmskmpapers.htm.

Fitz-Enz, J. (1994). How to measure human resource management. McGraw-Hill.

Gold, C. (1992). Total quality management in information services IS measures: A balancing act. Boston, MA: Research Note Ernst & Young Center for Information Technology and Strategy.

GSA. (1996). Performance-based management: Eight steps to develop and use information technology performance measures effectively (p. 106). Washington: GSA.

Johansson, U. (1996). Increasing the transparency of investments in intangibles. Available online: http://sveiby.konverge.com/articles/oecdartulfjoh.htm.

Kaplan, R. S., & Norton, D. P. (1992). The balanced scorecard - measures that drive performance. Harvard Business Review, 70(1), January/February, 71-79.

Kaplan, R. S., & Norton, D. P. (1996). The balanced scorecard - Translating strategy into action, xi, 322. Boston, MA: Harvard Business School.

Knapp, E. (1998). Knowledge Management. Business & Economic Review, 44(4), July/September.

KPMG Consulting. (2000). Knowledge Management Research Report 2000, 1-13. Available for download on the KPMG main web site as 2000 Knowledge Management Survey.

Lev, B. (2001). Intangibles: Management, measurement and reporting. Brookings Institution. Washington. Cited in FASB Special report April 2001: Business and Financial Reporting, Challenges from the New Economy.

Martinsons, M.,Davison, R., & Tse, D. (1999). The balanced scorecard: A foundation for the strategic management of information systems. Decision Support Systems, 25, 71–88.

Mouritsen, J.,Larsen, H. T.,Bukh, P. N., & Johansen, M. R. (2001). Reading an intellectual capital statement: Describing and prescribing Knowledge Management strategies. Proceedings of the 4th Intangibles Conference, Stern School of Business, New York University (May).

Neilson, R. (2000). Interview with Dr. Robert E. Neilson, Chief Knowledge Officer and Professor at the Information Resources Management College (IRMC) of the National Defense University, CHIPS Magazine, (Spring). Available online: http://www.chips.navy.mil/interview_with_dr.htm.

Pulic, A. (2000). An accounting tool for IC management. Available online: http://www.measuring-ip.at/Papers/ham99txt.htm.

Roos, J. (1996). Intellectual capital: What you can measure, you can manage. IMD Perspectives for Managers, No. 10. Available online: http://alexandrie.imd.ch/gotorec0302&id=&lang=?rec=031029057920189&act=0/.

Roos, J.,Roos, G.,Dragonetti, N. C., & Edvinsson, L. (1997). Intellectual capital: Navigating in the new business landscape. Macmillan, Houndsmills, Basingtoke.

Shand, D. (1999). Return on knowledge: Proving financial payoffs from Knowledge Management investments plagues experienced and novice practitioners. Knowledge Management, (April). Available online: http://www.destinationkm.com/articles/default.asp?ArticleID=725.

Strassmann, P. (1999). Measuring and managing knowledge capital. Report on Knowledge, Technology and Performance. Available online: http://www.strassmann.com/pubs/measuring-kc/.

Surmacz, J., & Santosus, M. (2001). The ABCs of Knowledge Management. CIO . Online edition, available: http://www.cio.com/research/knowledge/edit/kmabcs.html#what.

Sveiby, K. E. (1997). The new organizational wealth: Managing and measuring knowledge based assets. San Francisco, CA: Berrett Koehler. Chapter on measuring available online: http://203.147.220.66/IntangAss/MeasureIntangibleAssets.html.

Sveiby, K. E. (2001a). Methods for measuring intangible assets. Available online: http://www.sveiby.com.au/articles/IntangibleMethods.htm.

Sveiby, K. E. (2001b). What is Knowledge Management? Available online: http://www.sveiby.com/articles/KnowledgeManagement.html.

Svioka, J. (2001). Knowledge pays. CIO Magazine, (February 15). Available online: http://www.cio.com/archive/021501/new.html.

Truch, E. (2001). Mapping advances KM journey. Knowledge Management, (April). Available online: http://www.kmmag.co.uk/APRIL01/FORUMapr.HTM.

Van Grembergen, W. (2000). The balanced scorecard and IT governance. Information Systems Control Journal (previously IS Audit & Control Journal), 2, 40–43.

Van Grembergen, W., & Saull, R. (2000). Aligning business and Information Technology through the balanced scorecard at a major Canadian financial group: Its status measured with an IT BSC Maturity Model. Proceedings of the Hawaii International Conference on System Sciences (HICSS), Maui, Hawaii (January).

Van Grembergen, W., & Timmerman, D. (1998). Monitoring the IT process through the balanced score card. Proceedings of the 9th Information Resources Management (IRMA) International Conference, Boston, May (pp. 105–116).

Van Grembergen, W., & Van Bruggen, R. (1997). Measuring and improving corporate information technology through the balanced scorecard technique. Proceedings of the Fourth European Conference on the Evaluation of Information technology, Delft (October, pp. 163–171).

Van Grembergen, W., & Vander Borght, D. (1997). Audit guidelines for IT outsourcing. EDP Auditing, Auerbach 72-30-35 (June, pp. 1–8).

Wiig, K. M. (1997). Roles of knowledge-based systems in support of Knowledge Management. In J. Liebowitz & L. C. Wilcox (Eds.), Knowledge Management and Its Integrative Elements (pp. 69–87). Boca Raton: CRC Press.

Willcocks, L. (1995). Information management. The evaluation of information systems investments. London: Chapman & Hall.

World Bank. (1999). Knowledge Management metrics - A learning process. Comments from a speech from Laurence Smith, Knowledge & Learning Consultant, World Bank. Available online: http://www.zigonperf.com/resources/pmnews/knowledge_metrics.html.

Section I - IT Governance Frameworks

- Structures, Processes and Relational Mechanisms for IT Governance

- Integration Strategies and Tactics for Information Technology Governance

- An Emerging Strategy for E-Business IT Governance

Section II - Performance Management as IT Governance Mechanism

- Assessing Business-IT Alignment Maturity

- Linking the IT Balanced Scorecard to the Business Objectives at a Major Canadian Financial Group

- Measuring and Managing E-Business Initiatives Through the Balanced Scorecard

- A View on Knowledge Management: Utilizing a Balanced Scorecard Methodology for Analyzing Knowledge Metrics

- Measuring ROI in E-Commerce Applications: Analysis to Action

- Technical Issues Related to IT Governance Tactics: Product Metrics, Measurements and Process Control

Section III - Other IT Governance Mechanisms

- Managing IT Functions

- Governing Information Technology Through COBIT

- Governance in IT Outsourcing Partnerships

Section IV - IT Governance in Action

EAN: 2147483647

Pages: 182