A GENERIC APPLICATION OF PROJECT MANAGEMENT IN IMPLEMENTING SIX SIGMA AND DFSS

Project management brings together and optimizes (the focus is always on allocation of resources) rather than maximizes ( concentrating on one thing at the expense of something else; maximization leads to suboptimization) resources, including skills, cooperative efforts of teams , facilities, tools, information, money, techniques, systems, and equipment.

Why should project management, as opposed to other management principles, be used in the six sigma and DFSS implementation process? There are at least two reasons. First, project management focuses on a project with a finite life span, whereas other organizational units expect perpetuity. Second, projects need resources on both part-time and full-time bases, while permanent structures require resource utilization on a full-time basis. The sharing of resources may lead to conflict and requires skillful negotiation to see that projects get the necessary resources to meet objectives throughout the project life.

Since we already have defined the process of both six sigma and DFSS implementation as a project, indeed then, project management will ensure successes of the implementation process by following the generic four phases of a project's life. A typical approach is shown in Table 13.1. Tables 13.2 and Table 13.3 show the characteristics of the six sigma and DFSS implementation model and process using project management.

| Phase 1 | Phase 2 | Phase 3 | Phase 4 |

|---|---|---|---|

| Management Commitment | Structure Setup | Implementation | Working with Employees |

| Establish a six sigma and DFSS implementation team of one person from each functional area Train those selected in the six sigma and DFSS requirements | Capture company objectives Define:

Focus on continual improvement Develop policies and procedures Reconfirm quality management commitment | Make goal of six sigma and DFSS total improvement Examine internal structure and compare it to the goals of six sigma and DFSS Determine departmental objectives Review structure of the organization Review job descriptions Review current processes Review control mechanisms Review training requirements Review all communication methods Review all approval processes Review supplier relationship(s) Review risk considerations and how they are addressed Review all outputs Review all action plans | Provide applicable and appropriate training Prepare the organization for both internal and external audits Provide and/or develop appropriate and applicable methodology for corrective action Continue focus on improvement |

| Phase 1 | Phase 2 | Phase 3 | Phase 4 |

|---|---|---|---|

| Management Commitment | Structure Setup | Implementation of plan | Working with Employees and Suppliers |

| Initiate Project | Understand Process | Provide Six Sigma and DFSS Training | Monitor Progress |

| Management planning and goal setting Departmental commitment Quality team selection and active participation Training philosophy and tools of quality Process definition and selection Identification of critical processes and characteristics | Team flow charting for process understanding and analysis Cause and effect analysis Critical in-process parameters identified Standard operating procedures review, equipment repair, preventive maintenance, and calibration Process input and measurement evaluation Static process data collection Process evaluation | Executive training Departmental training Identification of shortcomings in the system of quality (specific areas) Definition of boundaries of responsibility Definition of limitations of resources Review of system for completeness | Worker/operator control in process Define quality system as it relates to current policies and practices (quality manual, procedures, instructions, and so on) Internal audits conducted Definition of key characteristics and monitoring of process variables Application of statistical process control in all key processes Initiation and follow up of corrective action |

THE VALUE OF PROJECT MANAGEMENT IN THE IMPLEMENTATION PROCESS

Project management is a tool that helps an organization to maximize its effort in implementing a project. Since the process of implementing both six sigma and DFSS ” or any other quality initiative ” is a project, the value of project management can be appreciated in at least two areas:

-

Planning the process

-

Setting reliable, realistic and obtainable goals

Planning the Process

Four steps define the planning process from a project management perspective. They are:

-

Identify and prioritize the customer base by contribution to current and future organizational profits.

-

Identify and weight criteria key customers use in selecting organizations and assess what changes to criteria or weighting are likely to occur in the future.

-

Assess the organization's competitive advantages and disadvantages in each area important to decision makers .

-

Establish long- term strategic objectives by identifying where the biggest gap exists between what is important to key customers and the organization's own strengths and weaknesses relative to competition.

To optimize the output of these four steps the following questions may be raised:

-

Is there a true management commitment for the project?

-

Does the project address needs of the organization's top priority customer groups?

-

Does the project address important needs of the customer?

-

Is the organization far ahead of competition in this area already?

-

Does this project truly offer the organization a good chance of making an improvement large enough to change customer behavior?

-

Will the project require investment large enough to wipe out potential gain?

-

How does the project rank on the above criteria in relation to other possible projects?

-

Once the project is selected, is the team continuously assessing whether or not the project is the best one to move the department and organization toward their goals?

Goal Setting

There are three basic steps in goal setting from a project perspective. They are:

-

Translate corporate strategy into concrete organizational goals that are attainable within a reasonable time.

-

Involve department managers in internal audit and benchmarking exercises to identify problem areas related to the goals.

-

With department managers, set specific improvement goals for each department and each team.

PM AND SIX SIGMA/DFSS

Harry (1997, p. 21.14) posed five questions in reference to projects. They are:

-

What do you want to know?

-

How do you want to see what it is that you need to know?

-

What type of tool will generate what it is that you need to see?

-

What type of data are required of the selected tool?

-

Where can you get the required type of data?

These questions, upon further probing, will deliver some very impressive results. However, the concern remains: How would a Black Belt or even a Master Black Belt go about getting the correct answers to these questions? We believe the answer lies with strategic planning and persistence to the basic format of PM. That is, in the language of PM identify:

-

Work breakdown structure

-

Work packages

-

Time-scheduled network diagrams

-

Responsibility-assignment matrix

-

Risk analysis and quantification

-

Earned value analysis

-

Project integration management plans

-

Resource costing

-

Project change management

And, in the language of six sigma/DFSS:

-

Select key project/product.

-

Define performance variables.

-

Create the SIPOC model.

-

Measure current performance and capability.

-

Conduct a benchmarking.

-

Identify and evaluate gap.

-

Identify success factors and goals of project.

-

Select the performance variables.

-

Evaluate new performance.

-

Confirm causal variables.

-

Establish operating limits and verify performance improvement.

-

Validate control system.

-

Implement control system.

-

Audit.

-

Monitor.

Ultimately, all projects in the six sigma/DFSS world are managed in the following four categories:

-

Project justification and prioritization techniques

-

Project planning and estimation

-

Monitoring and measurement of project activity

-

Project documentation and related procedures

Project Justification and Prioritization Techniques

Justification and prioritization of projects are based upon the following methods:

Benefit-cost analysis:

-

Return on investment (ROI)

-

Internal rate of return (IRR)

-

Return on assets (ROA)

-

Payback period

-

Net present value (NPV)

Decision analysis and portfolio analysis as applied to project decisions

Benefit-Cost Analysis

Project benefit-cost analysis is a comparison to determine if a project will be (or was) worthwhile. The analysis is performed prior to implementation of project plans and is based on time-weighted estimates of costs and predicted value of benefits. The benefit-cost analysis is used as a management tool to determine if approval should be given for the project go-ahead. The actual data are analyzed from an accounting perspective after the project is completed to quantify the financial impact of the project. The sequence for performing a benefit-cost analysis is:

-

Identify the project benefits.

-

Express the benefits in dollar amounts, timing, and duration.

-

Identify the project cost factors including materials, labor, resources.

-

Estimate the cost factors in terms of dollar amounts and expenditure period.

-

Calculate the net project gain (loss).

-

Decide if the project should be implemented (prior to start) or if the project was beneficial (after completion).

-

If the project is not beneficial using this analysis, but it is management's desire to implement the project, what changes in benefits and costs are possible to improve the benefit-cost calculation?

Return on Assets (ROA)

Johnson and Melcher (1982) give an equation for return on assets (ROA) as:

ROA = ![]()

where net income for a project is the expected earnings and total assets is the value of the assets applied to the project.

Return on Investment (ROI)

ROI = ![]()

where net income for a project is the expected earnings and investment is the value of the investment in the project.

There are several methods used for evaluating a project based on dollar or cash amounts and time periods. Three common methods are the net present value (NPV), the internal rate of return (IRR), and the payback period methods. Project risk or likelihood of success can be incorporated into the various benefit-cost analyses as well.

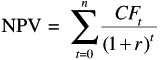

Net Present Value (NPV) Method

Weston and Brigham (1974) and Johnson and Melcher (1982) give the following equations:

where n = the number of periods; t = the time period; r = the per period cost of capital for the organization (also denoted as i if annual interest rate is used); and CF t is the cash flow in time period t. Note that CF , the cash flow in period zero, is also denoted as the initial investment.

The cash flow for a given period, CF t is calculated as:

CF t = CF B,t - CF C,t

where CF B,t is the cash flow from project benefits in time period t and CF C,t is the project costs in the same time period. The standard convention for cash flow is positive (+) for inflows and negative (-) for outflows.

The conversion from an annual percentage rate (APR) per year, equal to i, to a rate r for a shorter time period, with m periods per year, is:

R = ![]() -1

-1

If the project NPV is positive, for a given cost of capital, r, the project is normally approved.

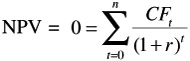

Internal Rate of Return (IRR) Method

The internal rate of return (IRR) is the interest or discount rate, i or r, that results in a zero net present value, NPV = 0, for the project. This is equivalent to stating that time weighted inflows equal time weighted outflows. The equation is

The IRR is that value of r that results in NPV being equal to 0 and is calculated by an iterative process. Once calculated for a project, the IRR is then compared with that for other projects and investment opportunities for the organization. The projects with the highest IRR are approved, until the available investment capital is allocated.

Most real projects would have an IRR in the range of 5 to 25% per year. Managers given the opportunity to accept a project that has calculated values for IRR higher than the company's return on investment (ROI) will normally approve, assuming the capital is available.

The above equations for net present value and internal rate of return have ignored the effects of taxes. Some organizations make investment decisions without considering taxes, while others look at the after-tax results. The equations for NPV and IRR can be used with taxes, if the cash flow effect of taxes is known.

Payback Period Method

The payback period is the length of time necessary for the net cash benefits or inflows to equal the net costs or outflows. The payback method generally ignores the time value of money, although the calculations can be done taking this into account. The main advantage of the payback method is the simplicity of calculation. It is also useful for comparing projects on the basis of quick return on investment. A disadvantage is that cash benefits and costs beyond the payback period are not included in the calculations.

Organizations using the payback period method will set a cut-off criterion, such as 1, 1 1/2, or 2 years maximum for approval of projects. Uncertainty in future status and effects of projects or rapidly changing markets and technology tend to reduce the maximum payback period accepted for project approval. If the calculated payback period is less than the organization's maximum payback period, then the project will be approved. (Quite often, in the six sigma/DFSS world, the payback is figured on a preset project savings rather than time. The most common figure floating around is a $250,000 per-project savings.)

Project Decision Analysis

In addition to the benefit-cost analysis for a project, the decision to proceed must also include an evaluation of the risks associated with the project. To manage project risks, first identify and assess all potential risk areas. Risk areas include:

| Business risks | Insurable risks |

|---|---|

| Technology changes | Property damage |

| Competitors | Indirect consequential loss |

| Material shortages | Legal liability |

| Health and safety issues | Personnel |

| Environmental issues |

After the risk areas are identified, each is assigned a probability of occurrence and the consequence of risk. The project risk factor is then the sum of the products of the probability of occurrence and the consequence of risk.

Project Risk Factor = ![]() {(probability of occurrence) * (consequence of risk)}

{(probability of occurrence) * (consequence of risk)}

Risk factors for several projects can be compared if alternative projects are being considered . Projects with lower risk factors are chosen in preference to projects with higher risk factors. A more extensive description of risk management is found in Kerzner (1995).

EAN: 2147483647

Pages: 235