ERP Systems Impact on Organizations

Overview

Jonas Hedman

Lund University, Sweden

Andreas Borell

Tetra Pak Information Management, Sweden

Copyright © 2003, Idea Group Inc. Copying or distributing in print or electronic forms without written permission of Idea Group Inc. is prohibited.

Abstract

Enterprise Resource Planning (ERP) systems are in most cases implemented to improve organizational effectiveness. Current research makes it difficult to conclude how organizations may be affected by implementing ERP systems. This chapter addresses this issue by presenting an artifact evaluation of ERP systems. The evaluation is based on the Competing Values Model (Quinn & Rohrbaugh, 1981; Rohrbaugh, 1981). The evaluation shows that ERP systems support effectiveness criteria, related to internal and rational goals of organizations. The evaluation also points out weaknesses in ERP systems, especially in areas related to human resource management and organizational flexibility. The result of the evaluation is used to discuss the impact of ERP systems on organizations and is presented as a series of hypotheses.

Introduction

Enterprise Resource Planning (ERP) systems have had an enormous impact on businesses and organizations around the world (Howcroft & Truex, 2001; Swanson, 2000). ERP systems are in most cases implemented with the goal to improve some aspect of the organization, e.g., strategic, organizational, business, management, operational, or IT-infrastructure (Hedman & Borell, 2002).

Studies show improvements, such as business process improvement, increased productivity and improved integration between business units (Davenport, 2000; Hedman & Borell, 2002; Hitt, Wu, & Zhou, 2002; Howcroft & Truex, 2002; Masini, 2001; Murphy & Simon, 2001; Poston & Grabski, 2001; Shang & Seddon, 2000). In order to achieve these benefits, organizational changes are required (Van der Zee & De Jong, 1999). Thereby, ERP systems are often assumed to be a deterministic technology, since organizations have to align their organizational structure, business process and workflow to the embedded logic of the ERP system (Glass, 1998). However, the casual relationship between ERP systems and organizational change has been questioned (Boudreau & Robey, 1999). The impact and benefit of ERP systems is unclear (Andersson & Nilsson, 1996). The only thing we know for certain is that the implementations are very resource consuming (Davenport, 1998).

The ability to determine or to appraise the impact of ERP systems would be of great importance from both theoretical and practical perspective. However, this is difficult for several reasons: First, it is not possible to draw explicit conclusions from IS benefit research (DeLone & McLean, 1992) on ERP systems. Second, there are inconsistent and contradictory findings from research on information technology and organizational change (Robey & Boudreau, 1999). Third, the interdependency between ERP system and organization requires interpretive and holistic evaluation methods (Borell & Hedman, 2001). Fourth, the measurement of organizational effectiveness is an elusive, complex and socially constructed construct (Campbell, 1977). Fifth, there is a lack of theorizing regarding the IT-artifact (Orlikowski & Iacono, 2001).

The purpose of this chapter is to evaluate the market leading ERP system, i.e., SAP R/3 Enterprise, in order to increase the understanding of how ERP systems may affect organizations and organizational effectiveness. The next section argues for conducting and evaluation of ERP systems with IS research as a frame of reference. The subsequent sections present an artifact-evaluation approach, an evaluation framework based on the Competing Values Model (Quinn & Rohrbaugh, 1981; Rohrbaugh, 1981), and the ERP system in question. In the final section, the results are summarized and presented as a series of hypotheses speculating how ERP system might affect organizations and organizational effectiveness. Future research directions are also suggested.

Background

Requirements specification is a problematic area in most IS implementations (Jackson, 1995), since "…we have a tendency to focus on the solution, in large part because it is easier to notice a pattern in the systems that we build than it is to see the pattern in the problems we are solving that lead to the patterns in our solutions to them" (R. Johnson in Jackson, 1995, p. 2). This applies in particular to the implementation of ERP systems (Borell & Hedman, 2000; Rolland, 2000). One of the reasons for this is the difference between implementations based on traditional information system development methods and the process of selecting and implementing ERP systems. It no longer appears meaningful to speak about analysis and design in a traditional fashion, because there is no analysis and design process as such. Instead, an evaluation of the reference model and the functionality of the ERP system is made, followed by a selection process. For each ERP system (or part of a ERP system) considered, there are three basic options: accept, accept with changes, or reject - all with different organizational consequences. These options must be considered in light of the requirements specification, which in turn has to reflect this (Borell & Hedman, 2000). These differences are illustrated in Figure 1. This line of reasoning is equally applicable to implementation of upgrades and extensions.

|

Traditional |

ERP system |

|---|---|

|

User |

Designer |

|

Designer |

System |

|

System |

Organization |

Figure 1: Comparison of traditional information system development methods and the process of selecting and implementing ERP systems

Another reason for addressing evaluation of ERP system comes from the conceptual thinking of IS researchers, such as Rudy Hirschheim and Barbara Farbey. Hirschheim & Smithson (1998) conclude in their literature survey of IS evaluation that the focus on tools and techniques from a positivistic approach has provided the foundation for traditional IS evaluation. The result has been "a more 'technical' interpretation of evaluation" (p. 402) - partly because of the widespread belief that IS are fundamentally technical systems. They argue that omitting the social domain makes it unlikely to produce a true or meaningful evaluative picture and that a more interpretive IS perspective seems to be the best vehicle for doing so.

Farbey, Land, & Targett (1995) propose a model known as The Benefits Evaluation Ladder, which they claim relates specifically to the need for evaluation. They argue that two of the most influential factors when selecting an evaluation method are application and objective (of change). A classification of "the uses of information systems may therefore be of fundamental importance in selecting suitable evaluation methods" (p. 41). Based on the perception that it is possible to classify IS applications associated with different types of organizational change. Their model consists of eight rungs, ranging from mandatory changes and automation to strategic systems and business transformation. Their classification is not rigid, but implies potential benefit as well as the uncertainty of outcome. Potential benefits and the level of uncertainty are both cumulative, thus systems classified on a certain stratum may have all the benefits (and accumulated uncertainty) from any or all of the strata below. They conclude that for the implementation of systems on the eighth rung "...benefits stem from the transformation as a whole. IT provides only one component of what is often a complex series of changes. It is not possible to attribute a portion of the benefits gained to any one factor" (p. 49). We conclude that in the taxonomy of Farbey et al. (1995), ERP systems are on the eighth rung and that they have the possible benefits and accumulated uncertainty of all the strata below. Therefore, it is highly unlikely that any two implementations will have identical requirements or consequences, even if they are based on the same generic software packages. While the potential benefits might be articulated, determination of the actual benefits from implementing an ERP system is difficult to foresee.

McKeen, Smith & Parent (1999) proposed a "supra-framework labeled Organizational Economics." They propose that their model "…can apply to all sorts of projects and organizational forms" (p. 13) and suggest that IT investments can be considered as part of a chain of events: a senior management decision ('IT Governance') has to be made that leads to a specific investment in IT which then needs to be deployed (selected and implemented) before it can be used by an organization to enhance its performance. In their first postulate, McKeen & Parent (1999) state that "With the focus at the enterprise level, it should be possible to capture the effects of the total IT investment on the organization's performance provided that the performance measure is related to the usage of the technology" (p. 15). The delimitation of level of analysis to an entire enterprise is based on the anticipated possibilities to obtain relevant measurements of cost and performance combined with a holistic perspective on the decision process. Investing in an ERP system is a top-management decision. It will have an impact on the culture, processes, structures and strategies of an organization (Davenport, 1998; Davison, 2002; Hanseth & Braa, 1998; Hanseth, Ciborra, & Braa, 2001; Kennerley & Neely, 2001), and therefore the only suitable level of analysis is the enterprise level, i.e., organizational.

Artifact Evaluation

Evaluation of the impact of ERP systems on organizational effectiveness is difficult (Murphy & Simon, 2001; Stefanou, 2001a, 2001b). Some of the problems that arise are the complexity and comprehensiveness of ERP systems, the lack of empirical research on the impact of ERP systems on organizational effectiveness (Hitt et al., 2002; Irani, 2002; Skok & Legge, 2001), and the shortcomings of traditional multivariate methods (such as factor analysis) for solving problems related to organizational effectiveness (Campbell, 1977). Following Hirschheim & Smithson (1998), we approached the problem in an interpretive way by applying an artifact-evaluation approach. This research approach belongs to a research stream stressing artifact utility, which can be broadly divided into artifact-building and artifact-evaluation approaches (Järvinen, 1999; Järvinen, 2000). Although critical, it is not well represented in IS research (Järvinen, 1999; Järvinen, 2000; Lee, 2000; March, Hevner, & Ram, 2000; March & Smith, 1995). An artifact can be a construct (concept), model, method, technique, instantiation of an information system or an ERP system. In artifact-building research, the focus is on questions such as: "Is it possible to build a certain artifact?; How should a certain artifact be defined?; and, How can we develop it?" In evaluation research, questions like "How effective and efficient is this artifact?" are posed and addressed.

To evaluate the effectiveness and efficiency of the artifact, both criteria and measurements are needed. To this end we chose the Competing Values Model (CVM). There were three main reasons for this choice: First, it is a well-established framework, empirically tested in organizational research (Buenger, Daft, Conlon, & Austin, 1996; Quinn & Cameron, 1983), management research (Hart & Quinn, 1993), and IS research (Carlsson & Widmeyer, 1994; McCartt & Rohrbaugh, 1995; Sääksjärvi & Talvinen, 1996) over a number of years. Second, it is related to the critical constructs of individual and organizational effectiveness. Third, it is addressing the organizational level of analysis. Later versions and extensions of CVM for assessing management competence (Quinn, 1989) and diagnosing organizational culture (Cameron & Quinn, 1999) were assessed, but they were not found to be appropriate for this evaluation due to their shortcomings regarding lower level efficiency.

Competing Values Model

Until the development of contingency theory, organizational effectiveness was perceived as an applied area, not a theoretical issue in organizational theory. Contingency theorists' addition to the development of organizational effectiveness as a theoretical issue were arguments that some organizational structures were more suitable than others to certain task, size, and environment, i.e., contingency factors (Scott, 1998). The question that followed was: "Suited in what sense?" The answer given to this question in most cases was in terms of effectiveness (Cameron, 1981; Campbell, 1977; Goodman & Pennings, 1977; Olerup, 1982; Scott, 1998).

Traditionally, organizational effectiveness was defined as meeting or surpassing organizational goals (Bedeian, 1987). The goal approach has dominated organizational effectiveness studies, despite criticisms (Hall, 1980) that organizations have multiple goals (Cameron, 1981) and that criteria for measuring effectiveness are ambiguous (Meyer, 1985). Alternative approaches to organizational effectiveness studies have emerged to deal with both these problems and others: e.g., the resource approach (Cunningham, 1978; Pfeffer & Salancik, 1978), the internal process approach (Ostroff & Schmitt, 1993), the stakeholder approach (Tusi, 1990), and the Competing Values Approach (Quinn, 1981; Quinn & Rohrbaugh, 1981; Rohrbaugh, 1981; Thompson, McGrath, & Whorton, 1981). Despite these efforts, it is still difficult and potentially controversial to quantify organizational effectiveness (Cameron & Whetten, 1983). Effectiveness criteria can be described in very general and broad terms, e.g., survival or profit, or in more narrow terms based on functions, e.g., hierarchical levels, roles, or processes in organizations based on the participants and constituents. The complexity of the concept of organizational effectiveness can be illustrated by Campbell's (Campbell, 1977) list of 30 different criteria for measuring organizational effectiveness, ranging from job satisfaction to growth and productivity. With regard to this, CVM is especially notable, since it combines diverse indicators of effectiveness and performance.

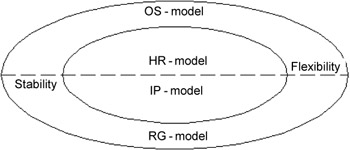

The Competing Values Model is based on the hypothesis that there is a tension between underlying value dimensions (Quinn, 1981; Quinn & Cameron, 1988; Quinn & McGrath, 1982). The first value dimension is focus - internal focus puts emphasis on the well being of the organization itself, while external focus is placed on the organization within its environment. Structure is the second value dimension - stability refers to the need for top management and control and flexibility refers to the need for adaptation and change in organizational structure. The third dimension relates to means and ends in different organizational effectiveness measures (Quinn & Rohrbaugh, 1981; Rohrbaugh, 1981). The measures that underlie the value dimensions reflect one of four organizational models: human relations model (HR), open systems model (OS), internal process model (IP), and rational goal model (RG). A critical point to note is that while different organizational models reflect different effectiveness criteria, they are not dichotomic. Effectiveness may require that organizations are both flexible and stable, as well as have a synchronous internal and external focus (Quinn & Cameron, 1988). The models reflect opposing views of organizational effectiveness simultaneously.

The HR model focuses on internal flexibility to develop employee cohesion and morale. It stresses human resource development, participation, empowerment, team building, trust building, conflict management, supporting, communication internally, developing individual development plans, feedback to individuals and groups, and developing management skills (Quinn, 1989).

The OS model focuses on external flexibility and suggests readiness and flexibility as the reason by which growth may be gained. Important issues are the acquisition of scarce resources, the support of interaction with the external environment, the identification of major trends, the development of business intelligence, the creation of mental models, facilitation of changes, dedication to research and development, the identification of problems, influences from the environment, and the maintenance of external legitimacy through a network of external contacts (Quinn, 1989).

The IP model focuses on internal stability and uses information management, information processing, and communication to develop stability and control. This is done by collecting data (mainly internal quantitative information used to check organizational performance), enhancing the understanding of activities, ensuring that standards, goals, and rules are met, maintaining organizational structure and workflow, coordinating activities, and collecting and distributing information internally (Quinn, 1989).

The RG model is characterized by a focus on external control and relies on planning and goal setting to gain productivity. This includes clarification of expectations, goals and purposes through planning and goal setting, definition of problems, generation and evaluation of alternatives, generation of rules and polices, evaluation of performance, decision support, quality control, motivation of organizational members to enhance productivity, sales support, and maximization of profit (Quinn, 1989).

A summary of the four organizational models (HR, OS, IP, and RG), the value dimensions, and related measures of organizational effectiveness is depicted in Figure 2. The value dimensions and the related organizational models should not be directly compared to the major organizational perspectives that exist in organizational theory: namely rational, natural, and open. Take for instance the open system perspective, which views organizations as open systems but also emphasizes information processing, which relates to the internal process model in CVM.

Figure 2: Competing Values Model based on Quinn (1981) and Rohrbaugh (1981)

CVM is traditionally depicted as a grid or quadrant, as are many other models and frameworks, e.g., the balanced scorecard (Kaplan & Norton, 1996) or SWOT (Andrews, 1971). The quadratic way of representing organizations and information systems may not be the best approach. In information systems are organizations commonly represented through an ellipse. Therefore, we have chosen to depict CVM by using modeling techniques common in the information systems community.

ERP Systems SAP R 3

For the evaluation of ERP systems, we chose SAP R/3 Enterprise, which was recently released during second half of year 2002. Enterprise has basically the same functionality as the previous SAP R/3 version 4.6b, but a new technological platform. The new R/3 architecture is built on the ideas of layered architecture and maintainability, where functionality and technology are separated to enable different release strategies for functionality and technology. This increases the system's portability of technical platform, as well as input and output devices, respectively. The technology in SAP R/3 Enterprise is based on SAP WEB Application Server, which has been in place for different mySAP.com components, such as the mySAP Business Information Warehouse (SAP's data warehouse).

The major implication of this change is that new releases of R/3 can either be of technical or functional nature, and each will have its own release strategy. Furthermore, the functionality, which is represented in the reference model, is divided into Enterprise Core and Enterprise Extensions processes. The first type of processes is internally oriented and contains the same functionality as version 4.6, but the process model has been optimized. For example, fixed asset accounting and payroll processing are two such Enterprise Core processes that are bounded to a firm from a practical and legal perspective. Enterprise Extensions processes include new functionalities, e.g., electronic bank account statements have been added to the financial model and mobile time management has enhanced the human resource model. The separation of Core and Extensions processes makes it easier for a customer to upgrade those parts of the system that are considered essential for them. (Details on SAP R/3 Enterprise are best found on SAP Service marketplace: http://service.sap.com/enterprise.)

One of the attractions of ERP systems is the value of integration. There are other perceived benefits associated to ERP systems including business process improvement, integration among business units, real-time access to data and information (Davenport, 2000), standardization of company processes, increased flexibility, increased productivity, increased customer satisfaction, optimized supply chain, business growth, improvement of order-to-cash time, competitive positioning ability, shared services, improved time to market cycles, and improved product quality (Cooke & Peterson, 1998). To summarize, ERP systems can support an organization in six main ways (Hedman & Borell, 2002):

- First, they support organizations by integrating information flows (such as customer information, financial and accounting information, human resources information, and supply chain information) and making it available to the entire organization (Davenport, 1998).

- Second, they integrate diverse primary business activities, functions, processes, tasks, and workflows (such as accounting, finance, and procurement) as well as secondary activities with primary activities (such as inventory management) (Davenport, 1998).

- Third, they serve as a common data repository (master data) for organizations (Scheer, 1998). The benefit of a data repository for an organization is that it may define the format of the data, which makes communication and interpretation easier.

- Fourth, they specify how organizations should conduct their business based on a best business practice reference model (Kumar & Hillegersberg, 2000).

- Fifth, they reduce the number of logical computer based information systems (Joseph & Swansson, 1998) and replace old legacy systems (Markus & Tanis, 2000).

- The last, and maybe the most obvious support, is that they deliver functionality per se, see below and Rashid, Hossain, & Patrick (2002). There are user administrative tools, data base administration tools, e-mail, appointment calendar, functionality for room reservations, ordering food, a software development workbench, telephone integration, workflow system, and an executive information system.

SAP R/3 Enterprise consists of functionality from three general business areas with different sub-areas. The first one is accounting and it deals with information flows concerning planning, controlling, and value representation of business processes, functions, and business units in an enterprise. Accounting is divided into external and internal accounting, in accordance with the target groups. External accounting (financial accounting) is structured according to legal requirements and the organization's openness to external parties, such as tax authorities and investors. Internal accounting, on the other hand, consists of cost and benefits accounting and is used to provide quantitative information to decision-makers within an enterprise.

The second part is logistics and includes all functionality for the design of material and information and production flow from the vendor, through production, to the consumer. Logistics is dived into three main areas: Sales and Distribution, Materials Management, and Production and Control. With the logistics module an enterprise can plan, control and coordinate logistical processes across department boundaries, based on the integration of existing data and functions. Logistics is similar to MRP II systems (Material Resource Planning systems).

Human resource management is the last part and is divided into two areas. The first area is Personal Planning and Development, which supports the strategic use of personal by giving the enterprise the functionality that makes it possible to manage personal systematically and qualitatively. Functions as organizational management, personnel development, workforce planning, training and recruitment are supported. Personal Administration and Payroll Accounting, which is the second part of human resource management, combines the administrative and operational tasks of human resources management. Here you can find functions for time management, incentive wages, payroll accounting, and travel expense.

In sum, ERP systems are large integrated computer software packages consisting of components, each with a given set of functions. All available functions operate on a shared set of data, thereby achieving integration. The idea of these systems is to support every single aspect of organizational storage, processing, retrieval, and distribution of data and information. This is supposedly done without regard to organizational scope, business, or comprehensiveness - at least that is what the vendors say. In that sense, an ERP system is a generic solution with different levels of adaptability, which makes every implementation unique in some sense since an organization must configure the system to its own specific requirements. In many cases, the system is customized to special requirements that are not supported by standard R/3.

Procedure

The evaluation of R/3 systems was performed in a three-step process. First, the functionality found in the system and reported benefits associated with ERP systems were listed. Then we categorized ERP capabilities with respect the value dimensions - internal vs. external and stable vs. flexible. The third step was to classify the functionality with regard to the value dimensions in CVM. The authors performed the evaluation and classification independently and the outcomes were then compared. There was substantial agreement, approximately 90%, between the evaluations (some functionalities were question-marked in the evaluations). Where disagreements existed, the functionality was reevaluated and a final classification and evaluation decision was made, which satisfied both authors. To some extent, we verified the classification from published articles on ERP systems benefits, but in most cases this was not possible. This is because most research on ERP systems does not describe the ERP functionality to such a detail that it is possible to verify the classification.

This approach has its limitations. For example, production planning is essential to manufacturing firms but is of little or no value to retail firms. In addition, there is the impact of the environment and technology of the user - some capabilities are more important than others depending on the environment and technology of the organization in question. An accountant does not need production planning functionality. Finally, the number of users of each function in an organization - it's likely to assume that some functionalities will have several users, e.g., a firm will have several sales persons.

Result

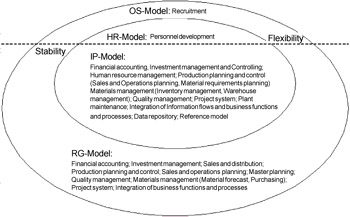

Most of the functionality and benefits map to either the IP model or the RG model; some of the functionality is interpretable as belonging to both models. This is because system functionality supports several organizational functions with different effectiveness metrics.

Accordingly, ERP systems and perceived benefits relate to IP-and RG-associated organizational goals and effectiveness metrics. Hence, ERP systems primarily support tasks related to control, efficiency, productivity, and stability by improving information management, coordination, and planning. The strong support of the IP model is natural since ERP systems (as are most IS, e.g., MIS, controlling systems, and inventory systems) are internal systems that are designed to support the internal processes and functions of organizations. Another important and critical functionality is the creation of master data records for customers and vendor. This functionality is used as a repository for data and makes it possible to communicate information through an organization. This is what makes integration of information and processes possible. However, the lack of support for HR and OS models was surprising. The outcome of the classification and evaluation of the functionality and benefits of ERP systems is presented in Figure 3.

Figure 3: Mapping of ERP system capabilities into CVM. *Parentheses indicate functions within functionality

Discussion

The artifact evaluation of the functionality of SAP R/3 Enterprise shows the existence of an, in part, implicit shared framework with CVM. This, combined with research performed on CVM makes it possible for us to draw conclusions, which we present as a series of hypotheses that predict the impact of ERP system on organizations and organizational effectiveness.

The first conclusion regarding ERP systems such as R/3 is that there is a lack of support regarding HR and OS model effectiveness constructs, i.e., an unbalanced support of organizational effectiveness. Such a suggestion is based on the idea that well-balanced support is in generally beneficial, and that an organization must simultaneously attain several different, and possibly contradictory, goals to become effective (Campbell, 1977). Predictions about ERP systems impact on organizations form our first hypotheses.

- Hypothesis 1a. ERP systems will affect organizations and improve those areas that are tied to organizational effectiveness measures related to IP and RG models.

- Hypothesis 1b. An organization with certain organizational effectiveness requirements must seek capabilities in the corresponding quadrant, which requires an evaluation of the organizations effectiveness requirements.

- Hypothesis 1c. A successful implementation of ERP systems has to be followed by organizational change efforts that will improve organizational effectiveness associated to HR and OS models, i.e., human resource development, flexibility, and adaptability.

- Hypothesis 1d. Organizations with an identified effectiveness focus in the HR or OS models will become less effective if they implement an ERP system.

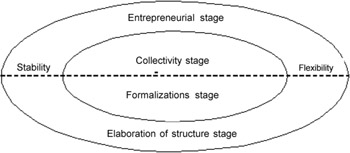

Studies within the CVM framework suggest that all effectiveness constructs are not equally important and critical at the same time. There are changes in the importance of the effectiveness constructs in relation to hierarchical levels and what stage of the life cycle a firm is in. Quinn and Cameron (1983) found, in relation to the CVM framework, four different stages a firm can be in: 1) entrepreneurial, 2) collectivity, 3) formalization and control, and 4) elaboration of structure stage. See Figure 4.

Figure 4: The four stages a firm can be in, in relation to the CVM framework

The critical effectiveness constructs of entrepreneurial stage lie in the OS model, while the critical effectiveness constructs of the collectivity stage lie in the HR model. In the formalization and control stage, the effectiveness constructs are based on the IP and RG models. The elaboration of structure stage has a more balanced emphasis upon the effectiveness constructs. The following hypotheses predicts the influence what stage in the life cycle a firm is in on the impact of ERP systems on organizations.

- Hypothesis 2a. For organizations in the entrepreneurial or collectivity stage, ERP systems are less beneficial, since they do not provide support for their critical effectiveness constructs, i.e., cohesion, morale, human resource development, innovation, adaptation, and growth.

- Hypothesis 2b. Organizations in the formalization and control stage, as well as the elaboration of structure stage, will be effectively supported by ERP systems since they give good support to those effectiveness constructs.

- Hypothesis 2c. Organizations that are in the process of moving from the collectivity stage to the formalization and control state could use an ERP system implementation to impose the structures and formalization needed in that stage.

- Hypothesis 2d. The probability of success of an ERP system implementation will differ depending on the current position of the organization in its life cycle. Most likely to achieve success are those organizations that are in the formalization and control stage.

In another study, it was found that there is also a difference in the importance of the effectiveness constructs in relation to hierarchical levels (Quinn 1989). The two major findings in the study were that: 1) there exists an equal emphasis for the IP and RG model - related effectiveness measurers, and 2) the importance of the OS models increases at higher hierarchical levels. In relation to our evaluation of ERP systems, these findings lead to the following hypotheses:

- Hypothesis 3a. ERP systems will provide support for middle- and lower- level managers.

- Hypothesis 3b. ERP systems do not provide sufficient support for top-level managers.

A question that arose regarding SAP R/3 was "is it effective or not?" This, of course, depends on various contextual factors, e.g., the stage of the life cycle and hierarchical level, which have to be addressed separately. However, it is obvious that R/3 Enterprise does not support top-level managers, expansion and growth of a firm, or the way a firm builds its corporate culture. That said, SAP has responded to some of these weaknesses. Lack of management support is addressed through Management Cockpit, a multi-dimensional executive information system, and drill-down possibilities have been provide in their Data Warehouse solution. The lack of flexibility and shortcomings regarding connections to the external environment is to some extent addressed by the Enterprise Portal. Increased compatibly is provided by BAPIs (Business Application Programming Interface) through predefined interfaces for communicating with other applications. One area, Human Resource Development, is currently not well supported by SAP's ERP system, and we are not aware of any major initiative by SAP to address this issue. This leads us to the final set of hypotheses related to ERP systems and organizations in general:

- Hypothesis 4a. Organizations cannot only rely on ERP systems for their information processing needs and have to seek alternative solutions for information processing related to HR model and OS model.

- Hypothesis 4b. ERP systems vendors have to develop alternative systems that address organizational flexibility and the relationship to the environment. For instance, CRM and SCM systems.

Conclusion

This chapter presents an artifact evaluation of an ERP system using an accepted framework of organizational effectiveness. The purpose of the evaluation was to improve the understanding of how ERP systems may or may not affect organizational effectiveness. The evaluation demonstrates both strengths and weaknesses of ERP systems. The strength of an ERP system is mostly related to IP model and RG model and the shortcomings are related to HR model and OS model.

In a real-case situation, our method must be complemented with both formal and informal methods and techniques. One such method or technique is the "competing values organizational effectiveness instrument" (Quinn, 1989) - the instrument measures perceptions of organizational performance. By applying said techniques and methods, it is possible to assess how different organizations perceive effectiveness constructs, as well as what they perceive as critical for that organization (Cameron & Quinn, 1999). Together these instruments and supplementary ways may be used to develop a recommendation for how competing values should be changed and how an ERP system can support different organizational effectiveness measurers.

Future research on ERP systems will include the development of instruments to diagnose organizations' effectiveness constructs and, in particular, this must include the development of computer-based support for this. This will enable us to determine the critical effectiveness constructs of an organization, which can be mapped to ERP systems. Future research will also include empirical studies addressing the relationship between ERP system use and support for organizational functions and processes, and how this is linked to individual and organizational performance. The result can improve our ability to design and configure ERP systems and prescribe how ERP systems can be used to improve organizational effectiveness.

Acknowledgment

We would like to thank Agneta Olerup, Sven Carlsson, Kevin Fissum and Jonas Larsson for their comments on earlier versions of this chapter.

References

Andersson, R., & Nilsson, A. G. (1996). The standard application package market - An industry in transition? In M. Lundeberg & B. Sundgren (Eds.), Advancing Your Business: People and Information Systems in Concert. Stockholm: EFI and Stockholm School of Economics.

Andrews, K. R. (1971). The concept of corporate strategy. Homewood: Dow Jones-Irwin.

Bedeian, A. G. (1987). Organization theory: Current controversies, issues, and directions. In C. L. Cooper & I. T. Robertson (Eds.), International review of industrial and organizational psychology, 1987 (pp. 1–33). Chichester: John Wiley & Sons.

Borell, A., & Hedman, J. (2000). CVA-Based framework for ERP requirements specification. Paper presented at the Information Systems Research in Scandinavia IRIS, University of Trollhättan, Uddevalla.

Borell, A., & Hedman, J. (2001). Artifact evaluation of ES impact on organizational effectiveness. Paper presented at the 2001 Americas Conference on Information Systems, Boston, MA.

Boudreau, M.C., & Robey, D. (1999). Organizational transition to Enterprise Resource Planning Systems: Theoretical choices for process research. Paper presented at the International Conference on Information Systems (ICIS).

Buenger, V., Daft, R. L., Conlon, E. J., & Austin, J. (1996). Competing values in organizations: Contextual influences and structural consequences. Organization Science, 7 (5), 557–576.

Cameron, K. S. (1981). Domains of organizational effectiveness. Academy of Management Journal, 24, 25–47.

Cameron, K. S., & Quinn, R. E. (1999). Diagnosing and changing organizational culture: Based on the competing values framework. Reading, MA: Addison-Wesley.

Cameron, K. S., & Whetten, D. (Eds.). (1983). Organizational effectiveness: A comparison of multiple models. San Diego, CA: Academic Press.

Campbell, J. P. (1977). On the nature of organizational effectiveness. In P. S. Goodman & J. Pennings (Eds.), New perspectives on organizational effectiveness (pp. 13–55). San Francisco: Jossey-Bass.

Carlsson, S. A., & Widmeyer, G. R. (1994). Conceptualization of executive support systems: A Competing Values Approach. Decision Science, 3 (4), 339–358.

Cooke, D., & Peterson, W. J. (1998). SAP implementation: Strategies and results (R-1217-98-RR). New York: The Conference Board, Inc.

Cunningham, J. B. (1978). A systems resource approach for evaluating organizational effectiveness. Human Relations, 31, 631–656.

Davenport, T. H. (1998, July/August). Putting the Enterprise into the Enterprise System. Harvard Business Review, pp. 121–131.

Davenport, T. H. (2000). Mission critical: Realizing the promise of Enterprise Systems. Boston, MA: Harvard Business School Press.

Davison, R. (2002). Cultural complications of ERP. Communications of the ACM, 45 (7), 109.

DeLone, W. H., & McLean, E. R. (1992). Information Systems success: The quest for the dependent variable. Information Systems Research, 3 (1), 60–95.

Farbey, B., Land, F. F., & Targett, D. (1995). A taxonomy of Information Systems applications: The benefits' of Evaluation Ladder. European Journal of Information Systems, 4 (1), 41–50.

Glass, R. L. (1998). Enterprise Resource Planning: Breakthrough and/or term problem. The DATA BASE for Advances in Information Systems, 29 (2), 14–15.

Goodman, P. S., & Pennings, J. M. (Eds.). (1977). New perspectives on organizational effectiveness. San Francisco: Jossey-Bass.

Hall, R. (1980). Effectiveness theory and organizational effectiveness. Journal of Applied Behavioral Science, 16, 536–545.

Hanseth, O., & Braa, K. (1998, December 13–16). Technology as traitor: Emergent SAP infrastructure in a global organization. Paper presented at the International Conference on Information Systems, Helsinki, Finland.

Hanseth, O., Ciborra, C. U., & Braa, K. (2001). The control devolution: ERP and the side effects of globalization. The DATA BASE for Advances in Information Systems, 32 (4), 34–46.

Hart, S. L., & Quinn, R. E. (1993). Roles executives play: CEOs, behavioral complexity, and firm performance. Human Relations, 46 (5), 543–574.

Hedman, J., & Borell, A. (2002). The impact of Enterprise Resource Planning Systems on organizational effectiveness: An artifact evaluation. In L. Hossain, J. D. Patrick, & M. A. Rashid (Eds.), Enterprise Resource Planning: Global opportunities & challenges (pp. 78–96). Hershey, PA: Idea Group Publishing.

Hirschheim, R. A., & Smithson, S. (1998). Evaluation of Information Systems: A critical assessment. In L. Willcocks & S. Lester (Eds.), Beyond the IT productivity paradox (pp. 381–409). John Wiley & Son, Ltd.

Hitt, L. M., Wu, D. J., & Zhou, X. (2002). Investment in enterprise resource planning: Business impact and productivity measures. Journal of Management Information Systems, 19 (1), 71–98.

Howcroft, D., & Truex, D. (2001). Critical analyses of ERP Systems: The macro level. The DATA BASE for Advances in Information Systems, 31 (4), 13–18.

Howcroft, D., & Truex, D. (2002). Critical analyses of ERP Systems: The micro level. The DATA BASE for Advances in Information Systems, 33 (1), 7–12.

Irani, Z. (2002). Developing a frame of reference for ex-ante IT/IS investment evaluation. European Journal of Information Systems, 11 (1), 74.

Jackson, M. A. (1995). Software requirements & specifications: A lexicon of practice, principles, and prejudices. Wokingham: ACM Press.

Järvinen, P. (1999). On research methods. Tampere: University of Tampere.

Järvinen, P. H. (2000). Research questions guiding selection of an appropriate research method. Paper presented at the Proceedings of the Eighth European Conference on Information Systems, Vienna.

Joseph, T., & Swansson, E. B. (Eds.). (1998). The package alternative in system replacement: Evidence for innovation convergence. Hershey, PA: Idea Group Publishing.

Kaplan, R. S., & Norton, D. P. (1996). The balanced scorecard: translating strategy into action. Boston, Mass.: Harvard Business School Press.

Kennerley, M., & Neely, A. (2001). Enterprise Resource Planning: Analysing the impact. Integrated Manufacturing Systems, 12 (2), 103–113.

Kumar, K., & Hillegersberg, J. V. (2000). ERP experience and evolution. Communications of the ACM, 43 (4), 23–26.

Lee, A. S. (2000). The social and political context of doing relevant research. MIS Quarterly, 24 (3), V.

March, S., Hevner, A., & Ram, S. (2000). Research commentary: An agenda for information technology research in heterogeneous and distributed environments. Information Systems Research, 11 (4), 327–341.

March, S. T., & Smith, G.F. (1995). Design and natural science research on information technology. Decision Support Systems, 15 (4), 251–266.

Markus, M. L., & Tanis, C. (2000). The Enterprise Systems experience: From adoption to success. In R. Zmud (Ed.), Framing the domains of its management: projecting the future ... through the past. Cincinnati, Ohio: Pinnaflex Educational Resources.

Masini, A. (2001). The ERP paradox: Understanding the impact of enterprise resource planning systems on firm performance. Paper presented at the Portland International Conference on Management of Engineering and Technology. PICMET '01.

McCartt, A. T., & Rohrbaugh, J. (1995). Managerial openness to change and the introduction of Gdss: Explaining initial success and failure in decision conferencing. Organization Science, 6 (5), 569–584.

McKeen, J. D., Smith, H. A. & Parent, M. (1999). An integrative research approach to assess the business value of information technology. In M. A. Mahmood & E. J. Szewczak (Eds.), Measuring Information Technology payoff: Contemporary approaches (pp. 5–23). Hershey, PA: Idea Group Publishing.

Meyer, M. (1985). Limits to bureaucratic growth. Walter DeGruyter, Inc.

Murphy, K., & Simon, S. (2001). Using cost benefit analysis for Enterprise Resource Planning project evaluation: A case for including intangibles. Paper presented at the Hawaii International Conference on Systems Sciences.

Olerup, A. (1982). A contextual framework for computerized Information Systems. Copenhagen, Denmark: Erhversökonomiskt Förlag.

Orlikowski, W. J., & Iacono, C. S. (2001). Research commentary: Desperately seeking the "IT" in IT research - A call to theorizing the IT artifact. Information Systems Research, 12 (2), 121–134.

Ostroff, C., & Schmitt, N. (1993). Configurations of organizational effectiveness and efficiency. Academy of Management Journal, 36, 1345–1361.

Pfeffer, J., & Salancik, G. R. (1978). The external control of organizations: A resource dependence perspective. New York: Harper & Row.

Poston, R., & Grabski, S. (2001). Financial impacts of Enterprise Resource Planning implementations. International Journal of Accounting Information Systems, 2, 271–294.

Quinn, R. E. (1981). A Competing Values Approach to organizational effectiveness. Public Productivity Review, 5 (2), 122.

Quinn, R. E. (1989). Beyond rational management: Mastering the paradoxes and competing demands of high performance. San Francisco: Jossey-Bass Publishers.

Quinn, R. E., & Cameron, K. (1983). Organizational life cycles and shifting criteria of effectiveness: Some preliminary evidence. Management Science, 29 (1), 33–51.

Quinn, R. E., & Cameron, K. S. (1988). Paradox and transformation. In R. E. Quinn & K. S. Cameron (Eds.), Paradox and transformation: Toward a theory of change in organization and management. Cambridge, MA: Ballinger Publishing Company.

Quinn, R. E., & McGrath, M. R. (1982). Moving beyond the single-solution perspective: The Competing Values Approach as a diagnostic tool. The Journal of Applied Behavioral Science, 18 (4), 462–472.

Quinn, R. E., & Rohrbaugh, J. (1981). A Competing Values Approach to organizational effectiveness. Public Productivity Review, 5 (2), 122–140.

Rashid, M. A., Hossain, L., & Patrick, J. D. (2002). The evolution of ERP Systems: A historical perspective. In L. Hossain, J. D. Patrick, & M. A. Rashid (Eds.), Enterprise Resource Planning: Global opportunities & challenges (pp. 1–16). Hershey, PA: Idea Group Publishing.

Robey, D., & Boudreau, M. C. (1999). Accounting for the contradictory organizational consequences of information technology: Theoretical directions and methodological implications. Information Systems Research, 10 (2), 167–185.

Rohrbaugh, J. (1981). Operationalizing the Competing Values Approach: Measuring performance in the employment service. Public Productivity Review, 5 (2), 141.

Rolland, C., & Prakash, N. (2000). Bridging the gap between organisational needs and ERP functionality. Requirements Engineering, 5 (3), 180–193.

Sääksjärvi, M., & Talvinen, J. M. (1996). Evaluation of organisational effectiveness of marketing information systems - The critical role of respondents. Paper presented at the Proceedings of the Fourth European Conference on Information Systems, Lisbon, Portugal.

Scheer, A.W. (1998). Business process engineering: reference models for industrial enterprises (Study ed.). Berlin; New York: Springer.

Scott, W. R. (1998). Organizations: Rational, natural, and open systems (4th ed.). Upper Saddle River, NJ: Prentice Hall.

Shang, S., & Seddon, P. B. (2000). A comprehensive framework for classifying the benefits of ERP Systems. Paper presented at the Americas Conference on Information Systems.

Skok, W., & Legge, M. (2001). Evaluating Enterprise Resource Planning (ERP) Systems using an interpretive approach. Knowledge and Process Management, 9 (2), 72–82.

Stefanou, C. J. (2001a). A framework for the ex-ante evaluation of ERP software. European Journal of Information Systems, 10 (4), 204–215.

Swanson, E. B. (2000). Innovating with packaged business software in the 1990s (Working Paper). The Anderson School at UCLA.

Thompson, M. P., McGrath, M. R., & Whorton, J. (1981). The Competing Values Approach: Its application and utility. Public Productivity Review, 5 (2), 188.

Tusi, A. S. (1990). A Multiple-Constituency Model of effectiveness: An empirical examination at the Human Resource Subunit level. Administrative Science Quarterly, 35, 458–483.

Van der Zee, J. T. M., & De Jong, B. (1999). Alignment is not enough: Integrating Business and Information Technology. Journal of Management Information Systems, 16 (2), 137–158.

Part I - ERP Systems and Enterprise Integration

- ERP Systems Impact on Organizations

- Challenging the Unpredictable: Changeable Order Management Systems

- ERP System Acquisition: A Process Model and Results From an Austrian Survey

- The Second Wave ERP Market: An Australian Viewpoint

- Enterprise Application Integration: New Solutions for a Solved Problem or a Challenging Research Field?

- The Effects of an Enterprise Resource Planning System (ERP) Implementation on Job Characteristics – A Study using the Hackman and Oldham Job Characteristics Model

- Context Management of ERP Processes in Virtual Communities

Part II - Data Warehousing and Data Utilization

- Distributed Data Warehouse for Geo-spatial Services

- Data Mining for Business Process Reengineering

- Intrinsic and Contextual Data Quality: The Effect of Media and Personal Involvement

- Healthcare Information: From Administrative to Practice Databases

- A Hybrid Clustering Technique to Improve Patient Data Quality

- Relevance and Micro-Relevance for the Professional as Determinants of IT-Diffusion and IT-Use in Healthcare

- Development of Interactive Web Sites to Enhance Police/Community Relations

EAN: 2147483647

Pages: 174