Decision Analysis with Additional Information

| Earlier in this chapter we discussed the concept of the expected value of perfect information . We noted that if perfect information could be obtained regarding which state of nature would occur in the future, the decision maker could obviously make better decisions. Although perfect information about the future is rare, it is often possible to gain some amount of additional (imperfect) information that will improve decisions. In this section we will present a process for using additional information in the decision-making process by applying Bayesian analysis . We will demonstrate this process using the real estate investment example employed throughout this chapter. Let's review this example briefly : A real estate investor is considering three alternative investments, which will occur under one of the two possible economic conditions (states of nature) shown in Table 12.11. Table 12.11. Payoff table for the real estate investment example

In Bayesian analysis additional information is used to alter the marginal probability of the occurrence of an event . Recall that, using the expected value criterion, we found the best decision to be the purchase of the office building, with an expected value of $44,000. We also computed the expected value of perfect information to be $28,000. Therefore, the investor would be willing to pay up to $28,000 for information about the states of nature, depending on how close to perfect the information was. Now suppose that the investor has decided to hire a professional economic analyst who will provide additional information about future economic conditions. The analyst is constantly researching the economy, and the results of this research are what the investor will be purchasing. The economic analyst will provide the investor with a report predicting one of two outcomes . The report will be either positive, indicating that good economic conditions are most likely to prevail in the future, or negative, indicating that poor economic conditions will probably occur. Based on the analyst's past record in forecasting future economic conditions, the investor has determined conditional probabilities of the different report outcomes, given the occurrence of each state of nature in the future. We will use the following notations to express these conditional probabilities: g = good economic conditions p = poor economic conditions P = positive economic report N = negative economic report A conditional probability is the probability that an event will occur, given that another event has already occurred .

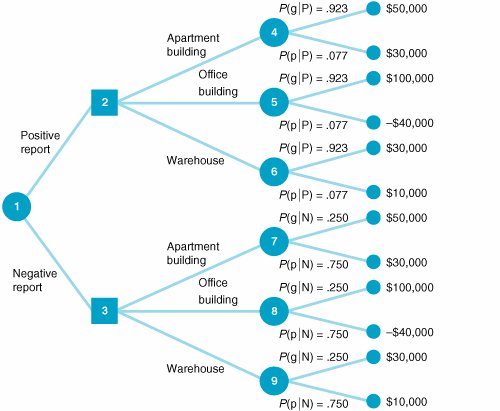

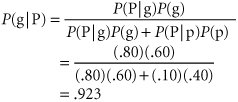

The conditional probability of each report outcome, given the occurrence of each state of nature, follows : P (Pg) = .80 P (Ng) = .20 P (Pp) = .10 P (Np) = .90 For example, if the future economic conditions are, in fact, good (g), the probability that a positive report (P) will have been given by the analyst, P (Pg), is .80. The other three conditional probabilities can be interpreted similarly. Notice that these probabilities indicate that the analyst is a relatively accurate forecaster of future economic conditions. The investor now has quite a bit of probabilistic information availablenot only the conditional probabilities of the report but also the prior probabilities that each state of nature will occur. These prior probabilities that good or poor economic conditions will occur in the future are P (g) = .60 P (p) = .40 Given the conditional probabilities, the prior probabilities can be revised to form posterior probabilities by means of Bayes's rule. If we know the conditional probability that a positive report was presented, given that good economic conditions prevail, P (Pg), the posterior probability of good economic conditions, given a positive report, P (gP), can be determined using Bayes's rule, as follows: A posterior probability is the altered marginal probability of an event, based on additional information. The prior probability that good economic conditions will occur in the future is .60. However, by obtaining the additional information of a positive report from the analyst, the investor can revise the prior probability of good conditions to a .923 probability that good economic conditions will occur. The remaining posterior (revised) probabilities are P (gN) = .250 P (pP) = .077 P (pN) = .750 Decision Trees with Posterior ProbabilitiesThe original decision tree analysis of the real estate investment example is shown in Figures 12.2 and 12.3. Using these decision trees, we determined that the appropriate decision was the purchase of an office building, with an expected value of $44,000. However, if the investor hires an economic analyst, the decision regarding which piece of real estate to invest in will not be made until after the analyst presents the report. This creates an additional stage in the decision-making process, which is shown in the decision tree in Figure 12.6. This decision tree differs in two respects from the decision trees in Figures 12.2 and 12.3. The first difference is that there are two new branches at the beginning of the decision tree that represent the two report outcomes. Notice, however, that given either report outcome, the decision alternatives, the possible states of nature, and the payoffs are the same as those in Figures 12.2 and 12.3. Figure 12.6. Decision tree with posterior probabilities(This item is displayed on page 541 in the print version) The second difference is that the probabilities of each state of nature are no longer the prior probabilities given in Figure 12.2; instead, they are the revised posterior probabilities computed in the previous section, using Bayes's rule. If the economic analyst issues a positive report, then the upper branch in Figure 12.6 (from node 1 to node 2) will be taken. If an apartment building is purchased (the branch from node 2 to node 4), the probability of good economic conditions is .923, whereas the probability of poor conditions is .077. These are the revised posterior probabilities of the economic conditions, given a positive report. However, before we can perform an expected value analysis using this decision tree, one more piece of probabilistic information must be determinedthe initial branch probabilities of positive and negative economic reports . The probability of a positive report, P (P), and of a negative report, P (N), can be determined according to the following logic. The probability that two dependent events, A and B, will both occur is P (AB) = P (AB) P (B) If event A is a positive report and event B is good economic conditions, then according to the preceding formula, P (Pg) = P (Pg) P (g)

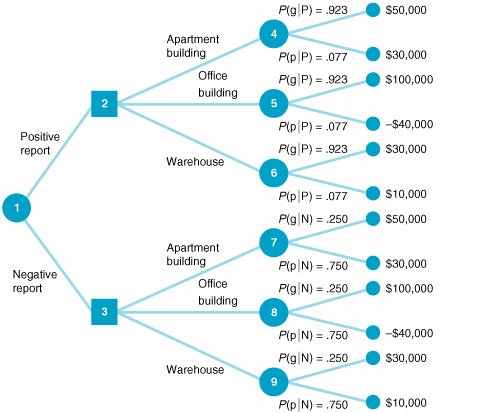

We can also determine the probability of a positive report and poor economic conditions the same way: P (Pp) = P (Pp) P (p) Next, we consider the two probabilities P (Pg) and P (Pp), also called joint probabilities . These are, respectively, the probability of a positive report and good economic conditions and the probability of a positive report and poor economic conditions. These two sets of occurrences are mutually exclusive because both good and poor economic conditions cannot occur simultaneously in the immediate future. Conditions will be either good or poor, but not both. To determine the probability of a positive report, we add the mutually exclusive probabilities of a positive report with good economic conditions and a positive report with poor economic conditions, as follows: P (P) = P (Pg) + P (Pp) Events are mutually exclusive if only one can occur at a time . Now, if we substitute into this formula the relationships for P (Pg) and P (Pp) determined earlier, we have P (P) = P (Pg) P (g) + P (Pp) P (p) You might notice that the right-hand side of this equation is the denominator of the Bayesian formula we used to compute P (gP) in the previous section. Using the conditional and prior probabilities that have already been established, we can determine that the probability of a positive report is P (P) = P (Pg) P (g) + P (Pp) P (p) = (.80)(.60) + (.10)(.40) = .52 Similarly, the probability of a negative report is P (N) = P (Ng) P (g) + P (Np) P (p) = (.20)(.60) + (.90)(.40) = .48 P (P) and P (N) are also referred to as marginal probabilities . Now we have all the information needed to perform a decision tree analysis. The decision tree analysis for our example is shown in Figure 12.7. To see how the decision tree analysis is conducted , consider the result at node 4 first. The value $48,460 is the expected value of the purchase of an apartment building, given both states of nature. This expected value is computed as follows: EV (apartment building) = $50,000(.923) + 30,000(.077) = $48,460 Figure 12.7. Decision tree analysis for real estate investment example(This item is displayed on page 543 in the print version) The expected values at nodes 5, 6, 7, 8, and 9 are computed similarly. The investor will actually make the decision about the investment at nodes 2 and 3. It is assumed that the investor will make the best decision in each case. Thus, the decision at node 2 will be to purchase an office building, with an expected value of $89,220; the decision at node 3 will be to purchase an apartment building, with an expected value of $35,000. These two results at nodes 2 and 3 are referred to as decision strategies . They represent a plan of decisions to be made, given either a positive or a negative report from the economic analyst. The final step in the decision tree analysis is to compute the expected value of the decision strategy, given that an economic analysis is performed. This expected value, shown as $63,194 at node 1 in Figure 12.7, is computed as follows: This amount, $63,194, is the expected value of the investor's decision strategy, given that a report forecasting future economic condition is generated by the economic analyst. Computing Posterior Probabilities with TablesOne of the difficulties that can occur with decision analysis with additional information is that as the size of the problem increases (i.e., as we add more decision alternatives and states of nature), the application of Bayes's rule to compute the posterior probabilities becomes more complex. In such cases, the posterior probabilities can be computed by using tables. This tabular approach will be demonstrated with our real estate investment example. The table for computing posterior probabilities for a positive report and P (P) is initially set up as shown in Table 12.12. Table 12.12. Computation of posterior probabilities

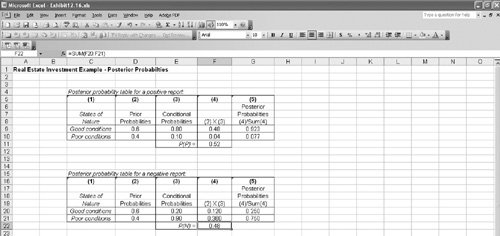

The posterior probabilities for either state of nature (good or poor economic conditions), given a negative report, are computed similarly. No matter how large the decision analysis, the steps of this tabular approach can be followed the same way as in this relatively small problem. This approach is more systematic than the direct application of Bayes's "rule," making it easier to compute the posterior probabilities for larger problems. Computing Posterior Probabilities with ExcelThe posterior probabilities computed in Table 12.12 can also be computed by using Excel. Exhibit 12.16 shows Table 12.12 set up in an Excel spreadsheet format, as well as the table for computing P (N). Exhibit 12.16. The Expected Value of Sample InformationRecall that we computed the expected value of our real estate investment example to be $44,000 when we did not have any additional information. After obtaining the additional information provided by the economic analyst, we computed an expected value of $63,194, using the decision tree in Figure 12.7. The difference between these two expected values is called the expected value of sample information (EVSI) , and it is computed as follows: EVSI = EV with information EV without information The expected value of sample information is the difference between the expected value with and without additional information . For our example, the expected value of sample information is EVSI = $63,194 44,000 = $19,194 This means that the real estate investor would be willing to pay the economic analyst up to $19,194 for an economic report that forecasted future economic conditions. After we computed the expected value of the investment without additional information, we computed the expected value of perfect information , which equaled $28,000. However, the expected value of the sample information was only $19,194. This is a logical result because it is rare that absolutely perfect information can be determined. Because the additional information that is obtained is less than perfect, it will be worth less to the decision maker. We can determine how close to perfect our sample information is by computing the efficiency of sample information as follows: efficiency = EVSI · EVPI = $19,194 / 28,000 = .69 The efficiency of sample information is the ratio of the expected value of sample information to the expected value of perfect information . Thus, the analyst's economic report is viewed by the investor to be 69% as efficient as perfect information. In general, a high efficiency rating indicates that the information is very good, or close to being perfect information, and a low rating indicates that the additional information is not very good. For our example, the efficiency of .68 is relatively high; thus, it is doubtful that the investor would seek additional information from an alternative source. (However, this is usually dependent on how much money the decision maker has available to purchase information.) If the efficiency had been lower, however, the investor might seek additional information elsewhere.

| |||||||||||||||||||||||||||||||||

EAN: 2147483647

Pages: 358