The Porter Model

|

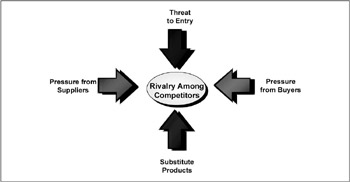

The Porter Model is a conceptual framework used to understand what makes industry change. The model was developed by Michael E. Porter, a professor at Harvard Business School. The model facilitates the formation of business strategy through analysis of the five forces that drive and shape industries (Exhibit 5-1). Determining how these forces can change your business helps you identify your strategic weaknesses and improve your competitive advantage.

Exhibit 5-1: The five forces that drive industry.

Intensity of Rivalry Among Competitors

Competitive intensity is dependent on the number and magnitude of actions taken by market players. Competitive actions can take many forms, such as changes in price, service, and quality. More actions and reactions to competitive movements intensify the amount of competition. Intensity may also be fueled by a few but significant actions, such as dramatic drops in price. Intensity of rivalry is also affected by industry growth rates, product type, the nature of the players, fixed or storage cost levels, and exit barriers.

-

Growth Rates. This aspect of competitive intensity is partially addressed in the economic filter, which addresses changes in market demand. The economic filter assesses alignment with market demand and impact. The focus here is on competition. For purposes of the SWAV, we need to isolate how the Strategic Alternatives will be affected by market growth rates. In high-growth industries, business performance can improve by keeping pace with the market. Assuming a company is growing as fast as its industry, it should increase in profits and size with the market. Shareholder value will be driven by a firm's membership in the industry. A slowgrowth environment will force its players to focus on market share and efficiency to enhance shareholder value. The key to growth is to take market share from other competitors, or to buy market share by acquisition. The only way to increase sales faster than the industry is to get your competitors' business. Increase in profits will come from doing things more efficiently.

-

Product Type. If the product is a commodity, the industry players will compete on price. The major characteristic of a commodity-driven marketplace is that product functions and features of equal quality can be delivered by the majority of the competitors in the marketplace. Brand, customer service, and customer loyalty are not major factors in the buying decision. Oil, steel, and agriculture can be categorized as commodity industries. This fuels more intense competition and tends to reduce the number of competitors. Markets that have complex products generate rivalry through differentiating product features and functions. Biotechnology is an example of an industry where products are highly differentiated.

-

The Nature of the Players. The nature of the market players is a function of their comparative size, demographics, and strategy. Markets containing players of the same size tend to have more intense competition. The absence of a dominant player fuels intensity. Companies take more risks because of the limited impact of competitor responses on their business. Intensity wanes as dominant players emerge. Smaller firms may fear that retaliation by big players will put them out of business.

Market player strategy has an important role in competitive rivalry. If the success of a company is defined by its accomplishment in a particular industry, competition will intensify. This creates a "succeed at all costs" mentality. This strategy may be destructive when large companies are vying for market position.

-

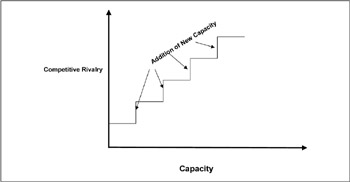

Fixed/Storage Cost Levels. High fixed costs increase competitive rivalry, usually in the form of price wars. This is caused by the push to fill existing capacity and to break even. The marketplace has a "ratchet-like" response to increased capacity (Exhibit 5-2). When capacity is added in large increments (i.e., businesses build large plants), competition tends to intensify. Capacity spikes lead to sharp price drops as businesses push to fill excess capacity. After the industry has reached an equilibrium point, intensity diminishes. This competitive lull will be interrupted by the next addition of a large increment of capacity.

Exhibit 5-2: Relationship between competitive rivalry and capacity.

-

Exit Barriers. The steeper the exit barrier, the more intense the level of competition. If the cost of leaving a market is formidable, then firms tend to stay in the business. This may relate to selling special use assets, union contracts, or synergies with other operating divisions. Back to the example above, if a company has a significant investment in plants, they have created a barrier to exit. The barriers relate to sale of the plant and redeployment of workers and the time involved in liquidation, among other things.

Threat to Entry

Porter states that when barriers to entry are high, the danger of new competition breaking into the market diminishes. The threat from outside competition coming into the market is related to the six barriers to entry in the marketplace: economies of scale, product differentiation, switching costs, access to distribution channels, cost disadvantages independent of scale, and government policy.

-

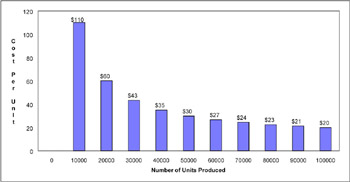

Economies of Scale. This barrier is established when market participants can produce a product less expensively than market newcomers. Economies of scale refer to the decrease in unit cost as the volume produced increases. Exhibit 5-3 illustrates the relationship between production level and unit cost. If ABC Corp. is entering the market and chooses to produce 10,000 units, the cost of production is $110 per unit. At a production level of 20,000, the unit cost declines to sixty dollars. The cost advantage of a 20,000-unit production level over a 10,000-unit level is fifty dollars per unit. The significance of economies of scale diminishes as production levels increase. When ABC doubles production from 50,000 to 100,000 units, they would only realize a decline in unit cost of ten dollars, as shown in Exhibit 5-3.

Exhibit 5-3: ABC Corp. unit costs.

The economics of scale issue creates three choices for the newcomer:

-

Enter the market on a very large scale to be price-competitive. (This requires a significant investment.)

-

Make a limited investment and operate at a cost disadvantage.

-

Identify a strategic partner with manufacturing capability and share potential profits.

-

Product Differentiation. When entering a new market, a company may encounter competitors who have achieved customer loyalty through advertising, customer service, and a prior market presence. It then becomes crucial for the new company to differentiate its product from those of its competitors.

-

Switching Costs. Entering into new markets may require new supplier relationships. These costs are incurred when changing from one supplier to another. For example, entry into the equipment rental business by an equipment manufacturer may require new inventory-tracking software. The switching costs in this instance are:

Switching Cost

Example

Employee retraining costs

Training employees on new software

Costs of new ancillary equipment

Purchasing new hardware to run the software

Cost in time and system testing

Time expended by the information technology staff

Psychic costs

Staff-related issues around operation of the new software and difficulty with interaction with outside staff

-

Access to Distribution Channels. Developing distribution channels for new products is difficult and may require special incentives. A distribution channel is a method of getting product to market. For example, in the retail industry, the distribution channel consists of direct sales to your customer (such as the Gateway stores where customers buy PCs directly from Gateway Computers). Established market participants have the advantage of existing platforms to market products. Channel partners, such as distributors, may view existing relationships as less risky. E-commerce has improved access to distribution channels by creating product exchanges and marketplaces. In addition, e-commerce has inherent barriers that are technological and not physical. For example, a company may encounter problems in getting software systems from different companies to interact with one another.

-

Cost Disadvantages Independent of Scale. Existing competitors also have advantages over new market players that stem from the following four factors:

-

Proprietary product technology such as patents, trademarks, or internal processes. (Viagra is an example here.)

-

Favorable access to raw materials from purchasing agreements with suppliers. (This is a major cost advantage.)

-

Favorable locations that are more accessible to raw materials, or within closer proximity of customers and/or destination. (Hotels located close to beaches or ski slopes are one example.)

-

Better-trained management and staff. (This constitutes a learning or experience curve that has already been traveled.)

-

-

Government Policy. The government may create barriers to market entry to assure the welfare of its citizens, or to constrain growth of business. Two policies that serve as obstacles to entering a marketplace are:

-

Licensing requirements that local governments have enacted. (An example is the licensing requirement for selling alcoholic beverages.)

-

Limits to access of raw materials. (The paper industry has limited access to national forests constraining logging for environmental purposes.)

-

Bargaining Power of Suppliers

High supplier bargaining power constrains market participants' ability to negotiate pricing, quality, and service. As supplier power increases, industry profit margins will decline because costs will increase. Companies are unable to pass price increases on to customers, as customers become price-sensitive. In the mid-nineties, gasoline retailers were affected by the power that oil refiners had to increase the cost of gasoline. The comparable size between the supplier and the buyer plays a role in this relationship. If the suppliers are larger than the buyers, they tend to have a higher degree of bargaining power. A small, familyrun gas station being supplied by a large oil company is an example of this relationship. Since the familyrun business is at the behest of a few large suppliers, the bargaining power of the supplying oil companies is greater.

Bargaining Power of Buyers

The ability of the buyer to negotiate the terms of sale significantly affects pricing and profits. As the customer becomes more powerful, downward pressure is exerted on pricing and profitability. Customer service begins to improve as industry participants find different ways to compete. Improved service has been observed in the banking industry as deregulation and overcapacity has pushed banks to compress product delivery times. Banks have dropped loan approval time from one week to one day on many types of commercial loans.

Substitute Products

Items that decrease sales of products within an industry are substitute products. For example, frozen yogurt is considered a substitute for ice cream. Sport utility vehicles (SUVs) can be considered a substitute product to the automobile. Substitutes can be viewed in two ways. They can be viewed negatively by the industry because they siphon off revenue from auto sales.

The other perspective is that substitute products add to the breadth of the industry by creating opportunities that increase the overall market. Auto companies have enjoyed higher profits because the SUVs have higher margins. This has prompted Mercedes Benz to widen its product offering to include this type of vehicle.

|

EAN: 2147483647

Pages: 117