Completing Cost Budgeting

|

| < Day Day Up > |

|

Cost budgeting is the process of assigning a cost to an individual work package. The goal of this process is to assign costs to the work in the project so that the work may be measured for performance. This is the creation of the cost baseline, as shown here:

Cost budgeting and cost estimates may go hand-in-hand, but estimating should be completed before a budget is requested—or assigned. Cost budgeting applies the cost estimates over time. This results in a time-phased estimate for cost, allowing an organization to predict cash flow needs. The difference between cost estimates and cost budgeting is that cost estimates show costs by category, whereas a cost budget shows costs across time.

Consider the Inputs to Cost Budgeting

Because cost budgeting and cost estimating are so closely related, you can expect many of the same inputs for both. Here are the inputs to cost budgeting:

-

Cost estimates These serve as key inputs; they’re the predicted cost for the project work.

-

Work breakdown structure It’s a key input to this process, as it is the deliverables of the project—it’s what the project is buying.

-

Project schedule The project schedule is needed to determine when the monies in the budget will be spent. The schedule should reflect the sequenced activities against a projected timeline. This allows management not only to plan financially, but also to compare expected cash inflows against the cash outflows the project will demand.

-

Risk management plan The risk management plan is considered because of information it provides of the probability of identified risks and their associated costs. In addition, the risks may have an expected risk value that contributes to the contingency reserve for the project.

Developing the Project Budget

The tools and techniques used to create the project cost estimates are also used to create the project budget. Here’s a quick reminder of the four components:

-

Analogous budgeting This is a form of expert judgment that uses a top-down approach to predict costs. It is generally less accurate than other budgeting techniques.

-

Parametric modeling This approach uses a parametric model to extrapolate what costs will be for a project (for example, cost per hour and cost per unit). It can include variables and points based on conditions.

-

Bottom-up budgeting This approach is the most reliable, though it also takes the longest to create. It starts at zero and requires each work package to be accounted for.

-

Computerized tools The same software programs used in estimating can help predict the project budget with some accuracy.

Creating the Cost Baseline

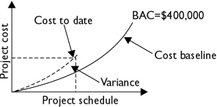

A project’s cost baseline shows what is expected to be spent on the project. It’s usually shown in an S-curve, as in Figure 7-3. The idea of the cost baseline allows the project manager and management to predict when the project will be spending monies and over what time period. The purpose of the cost baseline is to measure and predict project performance.

Figure 7-3: Cost baselines show predicted project and phase performance.

Large projects that have multiple deliverables may have multiple cost baselines to illustrate the costs within each phase. Additionally, larger projects may have cost baselines to predict spending plans, cash flows of the project, and overall project performance.

The purpose of a cost baseline is to measure performance, and a baseline will predict the expenses over the life of the project. Any discrepancies early on in the predicted baseline and the actual costs serve as a signal that the project is slipping.

|

| < Day Day Up > |

|

EAN: 2147483647

Pages: 209