The Third Dimension - Conflict of Interests

|

The Third Dimension—Conflict of Interests

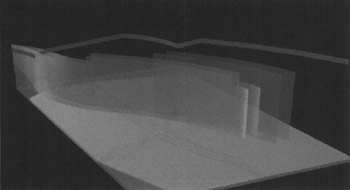

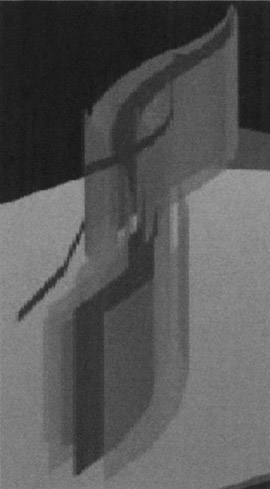

The traditional approach to EVM and statistical control, just explained, ignores the element of conflict. Although the owner normally thinks that the contract document resolves all conflicts, in reality it is only a beginning. Conflict is all-pervasive. Negotiations happen throughout the project duration and unless the basis for such negotiations is "best for everybody concerned" (Deming 1997), the conflict of financial interests is the third unquantified dimension in most contracts. Both owners and contractors expect "risk protection to ensure that they obtain what they expected at the time of the transactions." However, the project objective frequently changes for all or some of the project stakeholders during the course of the project. In construction programs, as part of real property investment, all stakeholders, in their positions as owners, contractors, developers, or equity partners, have an expectation of a fair return from a portfolio of multiple, interrelated projects which are being managed simultaneously for an aggregate return on investment. They all have some forecasts of expected cash flows. But the uncertainty inherent in the forecasting process carries with it a potential trap. It often creates gaps in expected and realized returns and the results and their effects are different for all the stakeholders as they manage their unique portfolios. Theoretically, the contract should protect all parties and reduce the uncertainty they face in order to stabilize their operating environments. In a practical sense, we need to at least accept the conflicts and understand the need to cooperate, coordinate activities, and reach a greater level of performance in a win-win relationship. Unmanaged conflicts have significance beyond the scope of a single current project, as they damage future project opportunities as well. The third dimension of the BCWS is an acceptance of this phenomenon. Figures 6, 7, and 8 show the BCWS extruded to the third dimension—the differing heights suggesting different conflict levels at various stages of the project.

Figure 6: EVM is a Three-Dimensional Process

Figure 7: View of the BCWP and BCWS Band

Figure 8: View of the BCWP and BCWS Band

Often times, the contractor operates in a multiproject environment and his profitability at any time is determined by how all the projects are doing. A detrimental effect in one could snowball to others if his rate of return on investment and working capital is affected. This induces a new negotiating and maximizing attitude in an otherwise "in control" project, ultimately jeopardizing its route to success. Shifting priorities often destroy the mutually compatible set of interests envisioned in the contract document. Suddenly there arise conflicting expectations, which ultimately deteriorate the trust between stakeholders. The mitigation and optimization of these conflicts within the contractual framework is the third dimension, which determines the success of project performance.

The Project and the Portfolio

All the stakeholders in a project vie for the same fixed resources of all the others. It is the ability to manage these multiple projects in a comprehensive manner that defines the program management space of all the players. What happens to the single project in these multiple project scenarios is a very interesting issue. We need to interpret the residual significance of the time and cost constraint imposed on the individual project when all the players are actually in a dynamic environment, dictated by their levels of commitment at the program management level. In fact, the development of the theory of diversification through portfolio selection is an adequate acknowledgement of the issue. It is based on the concept of maximizing the utility of an investor's wealth under conditions of uncertainty. A portfolio achieves a maximum return for any given level of risk or a minimum level of risk for a given level of return. Hence the assumption of a guaranteed payoff is clearly unrealistic. We can only put forward our best forecast based on the information we have today. Whether it is time or cost or the future value of the property under construction, it is wiser to talk of expected financial returns over the life cycle of the property or over the holding period of the investment. So as we widen our horizon, the view of our project changes. We are not only trying to minimize the standard deviation of our project returns; we are also trying to simultaneously minimize the standard deviation of our portfolio risk. Changing market conditions put new constraints on resources and the priority of projects in a portfolio may change for one or more of the parties in a contract. With numerous stakeholders in complex projects, the situation is essentially going to be different for different stakeholders in a project. This intriguing relationship of the project to the portfolios of the various stakeholders can very well be the focus of further research, but for now, optimizing this conflict within this process envelope is the final challenge.

|

EAN: 2147483647

Pages: 207