5.3 Multivariate elastic random walk

5.3 Multivariate elastic random walk

From Assumption 1 the n underlying factors follow a multivariate joint elastic random walk [2] :

where ± i ( t, x )= a i + B ij x i . In matrix notation this linear system of equations becomes:

where

The short- term interest rate is expressed as a linear combination of the underlying stochastic factors (Assumption 2), hence:

where

-

x - vector of stochastic factors characterising the underlying economic system,

-

w - vector of weights which are either constants or functions of time.

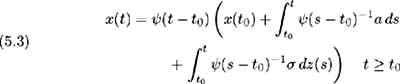

The solution to (5.1) has the form [3] :

where ˆ ( t ˆ’ t ) is the matrix solution [ 33 ], [ 3 ]to:

In the special case where B is a constant:

and (5.3) becomes

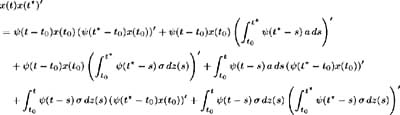

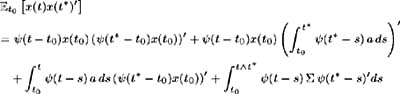

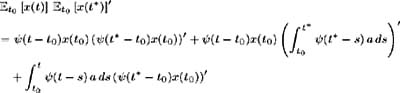

For this special case [4] , the expected value and covariance matrix of x ( t ) and x ( t *)( t and t * are future points in time) are then calculated to be [5] :

where & pound ; is the covariance matrix:

with elements ƒ ij = ij ƒ i ƒ j where ij = ![]() [ dz i · dz j ].

[ dz i · dz j ].

[2] As usual dz i is the standard Wiener process with:

-

[ dz i ] = 0,

[ dz i ] = 0, -

[ dz i dz i ] = dt .

[ dz i dz i ] = dt .

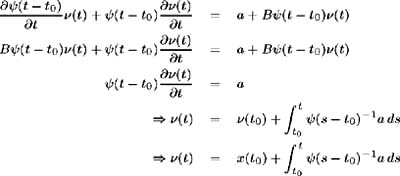

[3] The deterministic system of equations corresponding to (5.1) is:

This is a linear system, which has a solution of the form

where ½ ( t ) is some function of time and ˆ ( t ˆ’ t ) is the solution to the homogeneous matrix equation

with initial condition ˆ ( t ˆ’ t )= I , and hence it is the fundamental matrix of the system (5.4).

Matrix equation (5.4) now becomes:

and hence the solution to the deterministic system is:

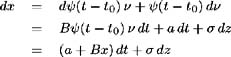

Now consider the system of stochastic equations

which has solution

Applying Ito's Lemma to x ( t )= ˆ ( t ˆ’ t ) ½ ( t )

which is the original differential system (5.1). Hence, we have shown that the solution to this system is

[4] The calculations are shown for the special case due to the simplified notation, however the more general case proceeds in a similar fashion.

[5] The covariance is calculated as follows :

Consider:

and so:

Also:

and hence (5.7) follows.

EAN: 2147483647

Pages: 132