2.4 Value of any contingent claim in equilibrium

2.4 Value of any contingent claim in equilibrium

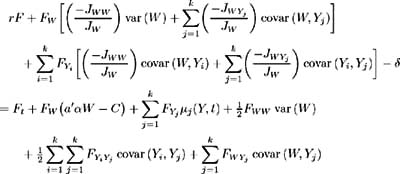

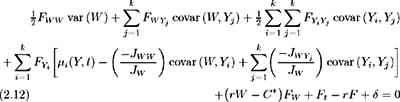

Now comparing the drift coefficients in (2.10) and (2.3) we have:

Making use of (2.11) yields:

Rearranging terms we have a partial differential equation for the price of any contingent claim [5] :

This valuation equation holds for any contingent claim. Specific terminal and boundary conditions as well as the structure of , the payout flow, define the unique characteristics of a claim.

[5] First group the coefficients of F W and make use of (2.8) to give:

Interest Rate Modelling (Finance and Capital Markets Series)

ISBN: 1403934703

EAN: 2147483647

EAN: 2147483647

Year: 2004

Pages: 132

Pages: 132

Authors: Simona Svoboda