Right Idea, Wrong Distribution

| For this purpose, my dear friend and colleague, Pascal Leroy[4], suggested the skewed lognormal distribution[5], which more accurately reflects many phenomena in nature.

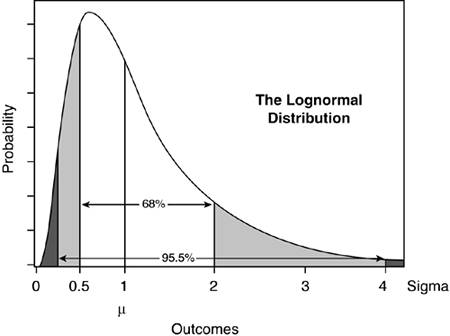

Unlike the standard normal distribution, the lognormal distribution is asymmetrical and lacks a left tail that stretches to infinity. Figure 9.5 shows what it looks like. Figure 9.5. The lognormal distribution for depicting positive outcomes only.

We still use a sigma to represent the standard deviation, but we interpret it differently for the lognormal distribution, as explained next. Note that µ is now coincident with 1 sigma. Half the area under the curve is to the left of 1 sigma and half is to the right; if we believe the universe of projects has this distribution, then we want our project to fall to the right of the 1 sigma line, which means its reward will be above the average.[6] This is the equivalent of saying that we are willing to invest µ (or 1 sigma) to do the project; any outcome (payoff, reward) less than that represents a loss (red ink), and anything above that is a win. To put it another way, we have "shifted" the lognormal distribution such that µ (s = 1) corresponds to breakeven or zero net payoff.

Unlike the standard normal distribution, the lognormal distribution clumps unsuccessful projects between zero and 1 sigma, and successful projects range from 1 sigma to infinity with a long, slowly diminishing tail. This tells us that we have a small number of projects with very large payoffs to the right, but our losses are limited on the left. This seems to be a better model of reality. The meaning of sigma is different in this distribution. As you move away from the midpoint, which is labeled here as 1 sigma, you accrue area a little differently. Each confidence interval corresponds to a distance out to ((1/2)n x sigma) on the left, and out to (2n x sigma) on the right. This means that 68 percent of the area lies between 0.5 sigma and 2 sigma, and 95.5 percent of the area lies between 0.25 sigma and 4 sigma. This is how the multiplicative nature of the lognormal distribution manifests itself. Mathematically, the distribution results from phenomena that statistically obey the multiplicative central limit theorem. This theorem demonstrates how the lognormal distribution arises from many small multiplicative random effects. In our case, one could argue that all variance in the outcomes of software development projects is due to many small but multiplicative random effects. By way of contrast, the standard normal distribution results from the additive contribution of many small random effects. |

EAN: N/A

Pages: 269

- Structures, Processes and Relational Mechanisms for IT Governance

- Integration Strategies and Tactics for Information Technology Governance

- Technical Issues Related to IT Governance Tactics: Product Metrics, Measurements and Process Control

- Governing Information Technology Through COBIT

- The Evolution of IT Governance at NB Power

- Chapter II Information Search on the Internet: A Causal Model

- Chapter III Two Models of Online Patronage: Why Do Consumers Shop on the Internet?

- Chapter IV How Consumers Think About Interactive Aspects of Web Advertising

- Chapter XI User Satisfaction with Web Portals: An Empirical Study

- Chapter XVI Turning Web Surfers into Loyal Customers: Cognitive Lock-In Through Interface Design and Web Site Usability