Economic Perspectives of the Strategic Positions

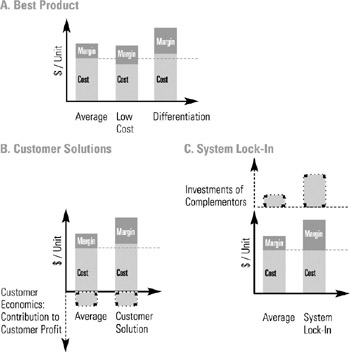

The three strategic positions are focused on three distinct economic perspectives (see figure 8.4). The economic implications of the best-product position are shown in Part A of the figure. The average business performer reflects the average cost of the industry and the margin available to the average player. In contrast are the lowcost competitor and the differentiated competitor; these two positions are the basic trade-offs represented in classic strategic positioning.

Figure 8.4: Economic Perspectives of the Strategic Positions

The lowest-cost performer is able to obtain a higher margin while still competitively pricing the product. This is a strong competitive advantage because the efficiency of the cost structure allows pricing below the cost of the average competitor that, in the long run, might put the average performers out of business. This is why the alternative to low cost must be differentiation, offering unique product attributes that the customer values and will pay a premium for. The differentiated player could have a higher cost than the average performer while still enjoying a fairly high margin because of the inherent additional value of the product. While the graph is simplistic, it represents important economic hurdles. To have a genuine low-cost position, a company needs to demonstrate lower relative unit costs. To have the economic leverage of a differentiated product, a company needs to show clearly that the customer will pay more, and that this premium is more than the added costs.

By contrast, the customer solutions position (shown in Part B of figure 8.4) centers on how products and services will impact the customer economics, either by lowering the customer's internal costs or by allowing the customers to have higher revenue. The customer solutions provider may have higher costs, but these are far outweighed by the economic contributions to the customer. The economic hurdle here is to show measurable and positive impact on the customer's profit.

Finally, we can contrast the economics of the system lock-in position with the other alternatives by recognizing that the scope is further enlarged to encompass the total system of which products or services are part. The economic hurdle is both to create additional value to the system as a whole through the heavy investment by complementors, and then to be able to appropriate this value. Part C in figure 8.4 shows an average competitor whose complementors modestly add value to the overall system. In contrast, the owner of a proprietary standard has been able to get significant investments from its complementors, which adds value to its system. At the same time, its ability to appropriate this added value is evident in its higher margins.

EAN: 2147483647

Pages: 214