Chapter Twelve Controlling the Buying Process

Twelve Controlling the Buying Process

Overview

There I was—the proverbial elephant hunter trying to drag home a live, adult elephant. A large organization in the financial services industry had agreed to explore doing business with us. I was excited and eager, but I knew there was a big risk—I could lose control of the elephant.

The path had been cleared; I had found a great Sponsor. Meetings with the Power Sponsor had gone extremely well. On the basis of his agreement to explore doing business with us, I suggested that I go back to my office, document our discussion, and propose a way for him to evaluate our capabilities. He had agreed, and asked if I could be ready the next day with something for him to look over. I said yes, and we agreed to meet for lunch and review the Evaluation Plan.

After lunch the next day, I gave him my letter with its attached Evaluation Plan. He began to review the letter and plan. Looking at his body language, I wasn’t sure what he was thinking; he seemed a little puzzled. He then reached into his inside jacket pocket, pulled out a pen, and began to edit the plan. At that point, I smiled to myself. Why? Because he was doing exactly what I wanted him to do—take ownership of the Evaluation Plan.

After he finished editing the Evaluation Plan, he handed it back and said, “I think this sequence of events will work better for us.” He had requested some schedule changes, nothing too significant.

At that moment, something came over me and I just had to ask, “Would you agree that we’re in the middle of a sales cycle?”

“Yes,” he responded, “I guess we are.”

“Who would you say is in control of the sales cycle at this point in time?” I said.

“I am, of course,” he said without hesitation. “I just took control when I changed your suggested sequence of events. The changes made it my own.”

“That’s exactly what I hoped you would say,” I responded.

He paused for a moment and then picked up the proposed Evaluation Plan from the table and tore it into pieces. He looked over at me and said, “I don’t think I’ll need this.”

I became very anxious and nervous. I thought my curiosity about my process had gotten me into trouble. Why couldn’t I have left well enough alone? Why did I have to ask that question?

A smile returned to his face. “If you can teach our salespeople to do what you just did,” he said, “which is to control the buying process and have the buyer believe he’s in control of buying, that alone is worth doing business together. We don’t need to evaluate any further. How soon can we get started?”

YOU WIN WHEN YOU CONTROL THE BUYING PROCESS

This control principle specifies that the salesperson controls the buying process—not the buyer. Keeping control of the buying process and letting the buyer buy without pressure appear to be mutually exclusive, but they are not. Solution Selling is about keeping control while letting your buyers direct themselves. The role of the salesperson in Solution Selling is to be a buying facilitator.

I often ask salespeople who are engaged in active opportunities what elements of control they have been able to put in place during the buyer’s evaluation process. If the answer is none, I know they have a low probability of winning, so I work with them on strategies and techniques to put controls in place. If this can’t be done, I encourage them to disengage. Remember the concept of column fodder? It’s alive and well. Stop wasting time on opportunities that won’t allow you to exert any control: those are opportunities you’re unlikely to win.

The job aids I introduce in this chapter help salespeople work professionally and collaboratively with their buyers to solve their critical business issues and reach a mutual decision to do business together. Exerting control may be as simple as establishing the time frame to make a decision or as specific as defining the exact evaluation criteria on which their decision will be based.

One way to control the buying process is through project management techniques. Project management is not a term used very often in selling. However, when you use good project management techniques, you put standard processes in place to deal with all contingencies, which enables you to achieve predictable results. This is important in most sales campaigns because there are so many variables.

Think about it. How often does a development project, or sale for that matter, come in on time and within budget without a plan? We all know that the answer is not very often, if at all. Incorporating project management techniques into the sales process helps transform selling activities from a series of random events into a logical sequence that concludes with a successful sale.

Project Management

The aim of project management is to organize the activities to achieve a goal within a specified time frame. In Solution Selling, the fundamental documents we use are the Power Sponsor Letter and the Evaluation Plan. If a salesperson can get a buyer to agree to an Evaluation Plan, including the sequence of events and a time line for each event, he or she will win these opportunities most of the time. This is not control of the buyer or the final decision, but control of the buying process.

Why would buyers allow a salesperson to exert any level of control over their buying process? The answer is that most buyers don’t buy (or go through the evaluation process) very often, so therefore they want and need help when they do buy. When salespeople demonstrate good situational knowledge by defining the buyer’s pains, diagnosing the reasons for the pains, and creating or re-engineering a vision of a solution, the buyer usually welcomes the salesperson’s proposed plan of action.

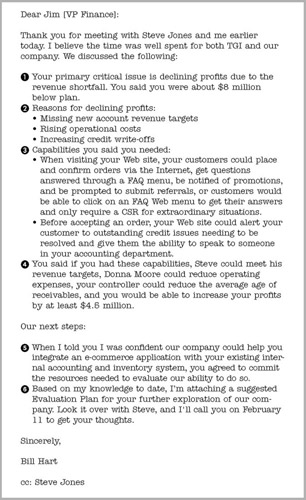

POWER SPONSOR LETTER

The Power Sponsor Letter used in Solution Selling is a classic example of how to incorporate project management techniques into selling. It helps Journeypeople look and act like Eagles.

Power Sponsor Letters help buyers buy and salespeople close business deals. Such letters help management predict the amount of business in the pipeline and when that business will close, and they help qualify opportunities and optimize resources by giving managers a view into the future. Without a doubt, this tool is the number one job aid used by the more than 500,000 salespeople who have been trained in Solution Selling globally.

Power Sponsor Letters have two components: (1) a letter written to the Power Sponsor and (2) a suggested Evaluation Plan with a sequence of events for the prospective customer to follow.

The Letter

The letter itself outlines the salesperson’s understanding of the situation: the pain, reasons for the pain, vision of a solution, organizational impact, agreement to explore doing business with the salesperson’s company, and an Evaluation Plan.

As you can see, the Power Sponsor Letter incorporates many of the same elements that are in a Sponsor Letter. The major differences are the request to commit resources to the evaluation process and the Evaluation Plan attached to the letter. I believe a good Power Sponsor Letter contains the following major elements (the numbered paragraphs correspond to the circled numbers in Figure 12.1):

- Pains. The principle no pain, no change also applies to Power Sponsors. It’s important to document and get verification of the critical business issue your Power Sponsor faces. Reconfirming your understanding of the pains in the letter also helps to establish personal credibility.

- Reasons for the Pain. You discovered and confirmed the reasons for your Power Sponsor’s pain in both the Diagnose Reasons and Explore Impact columns using Solution Selling’s 9 Block Vision Processing Model. Reconfirm the reasons in the letter as well.

- Buying Vision. This is Box C3 in the 9 Block Model and is critical to include in your letter. It should be clear and powerful and contain the capabilities that you helped the Power Sponsor see that he or she needs.

- Organizational Impact. This is where you confirm what the Power Sponsor has told you about the impact of the pain throughout the organization. Much of this came from the conversation that took place during Boxes I1 and I2 of the 9 Block Model. This helps to build the business case and the compelling reason to take action.

- Agreement to Explore. This reminds your Power Sponsor of his or her agreement to take the next step and explore ways of solving the pain. It’s important to remind him or her of this in the letter because it’s more difficult for people to change their minds after things have been committed to writing.

Figure 12.1: Power Sponsor Letter—Example

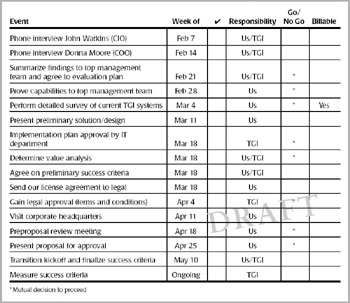

An Attached Draft Evaluation Plan

The draft Evaluation Plan (Figure 12.2) is attached to the Power Sponsor Letter. This plan details the evaluation process. It lists critical events necessary to get to the close, each event’s scheduled time line for completion, and go/no go decision points. Ultimately, the plan helps a salesperson exert control over the buyer’s evaluation process. A good plan should contain all the critical Milestones that will help you get to a win and the buyer to obtain your offering.

Figure 12.2: Draft Evaluation Plan—Example

The Event column breaks down what to do into a sequence of interdependent steps. The Week Of column gives suggested dates for each event. If dates are missed, the salesperson should negotiate new time lines and send out an amended plan. The Responsibility column designates who is responsible for a given event.

The Go/No Go column is a powerful qualifier because it requires that a decision be made about whether or not to proceed further in the evaluation. Read the footnote in the figure that says going forward or not is a mutual decision. This empowers both the buyer and the salesperson to make a mutual decision to proceed or not to proceed at each step along the way. This key element assures the buyer that he or she is in control of buying.

The Billable column is optional and may not be applicable in all cases. However, this can imply to the buyer that your activities or services are valuable. Any billable item may be negotiable, but it’s hard to negotiate it if it isn’t first in the plan.

Why Use an Evaluation Plan?

Simply put, the Evaluation Plan is the best closing tool I’ve ever used. It helps keep sales campaigns on track and provides a high level of predictability. It helps the buyer stay in control of the buying process and helps the salesperson stay in control of the selling process. Evaluation plans provide continuous feedback about where buyers are within their buying cycles and where salespeople are within their sales process. It’s not likely that a buyer would go through the time and effort to engage in an Evaluation Plan with someone with whom he doesn’t see himself doing business.

Why Make a Draft Evaluation Plan?

Initially, an Evaluation Plan is just a draft plan or a proposed sequence of events. It’s not the final Evaluation Plan—not until the buyer accepts it. So what’s the best thing you could wish for after you submit the plan and call to get the prospective customer’s feedback? You want them to suggest or make changes to the plan. Remember, if they change it, they own it. Just as in my story at the beginning of the chapter, buyers usually want to review it, change it, and make it fit their organization before they feel comfortable executing it. You want buyers to own the plan. It’s not your plan, it’s theirs. Buyers are more likely to execute their own plan than yours.

The Number of Events in an Evaluation Plan Varies

The number and sequence of events in an Evaluation Plan vary according to the scope of the opportunity. There are many variables, including the players involved, the industry being sold to, and the complexity of products and services being sold. In less complex sales, where you can close the sale quickly with one call, you construct the plan verbally and then work through each element with the prospective customer. In more complex sales, the list of events should be more extensive.

Never propose more steps than you think are necessary. You don’t want the buying process to be too complicated and cumbersome. On the other hand, a good and thorough evaluation is important for everyone involved.

Possible evaluation events in longer sales cycles or complex selling situations can open a number of opportunities to you. It’s also important to specify certain criteria so that you minimize surprises between yourself and your buyer (or buying committee). Evaluation events can provide opportunities for you to

- Gather all necessary information and details about the situation

- Interview all key players and beneficiaries

- Summarize and confirm findings to top management

- Specify when the costs and the associated value will be revealed

- Present a preliminary solution

- Specify when and how proof will be revealed

- Develop a value justification/value analysis

- Develop an implementation/transition plan

- Specify legal/technical/administrative steps to follow

- Specify a preproposal review

- Determine Success Criteria

- Specify ongoing measurement of Success Criteria

Remember, each sales situation is unique. Don’t fall into the trap of thinking, “This is the way we always do it” or “This is the series of steps we always follow.” But because many of the opportunities you’ll engage in are similar, use Evaluation Plans and sequences of events that have been successful in the past. Each event in your proposed plan should have a specific purpose. For example, summarizing your initial findings to top management can help you build momentum and qualify the opportunity further. The plan also serves the customers by making sure they are fully committed and not wasting their time and resources.

ADVANCE YOUR EVALUATION PLAN WITH VALUE JUSTIFICATION

By definition, justification is a reason, fact, circumstance, or explanation that justifies or defends the action being taken. Justification answers the question, Does the end justify the means? Unless you’re dealing with a single individual who has the power, money, and authority to buy without answering to anyone else, justification must be done. Too often salespeople leave this important step up to the prospect or customer to do. They don’t have a model to work from, or they’re afraid to get involved because they don’t know how. I recommend that salespeople initiate the activity and participate with the customer in the value justification activities. If you don’t know how, you must learn.

A COMPELLING REASON TO ACT

Value justification gives customers a compelling reason to take action. People will spend money if they can see that doing so will enable them to make more money or save money they’re currently spending.

Salespeople have been participating in ROI (return on investment) analysis and cost justifications for years. Many times I’ve observed salespeople frustrated because, though their proposal was completely justified with a fantastic ROI and a short time frame for payback, the customer still didn’t take action. Why? One reason is that the return and the payback are in the mind of the salesperson and not the buyer. The only way prospective buyers can get the same vision and understand the real value of the solution is if they understand and own both the problem and the solution. As long as salespeople are telling buyers, “We can solve your problems,” they’re not enabling prospective buyers to take ownership.

Historically, salespeople and customers have used terms such as cost justification and ROI analysis instead of value justification or value analysis. I stress the term value justification because I want salespeople to focus their customers and prospects on value. It’s very important for salespeople to know that the higher the price, the more important it is to sell value. Remember, in Solution Selling we define value as Total Benefits minus Total Cost or Total Investment.

Why Participate in Value Justifications?

There are several reasons for participating in value justifications. They include sale cycle initiation, closing a sale, discounting, proof, and avoiding no decisions.

Initiate Sale Cycles Once you know the value you bring to situations, you can leverage this to help initiate new opportunities and create curiosity in your prospect or customer more easily and quickly.

Close Sales Value justification creates compelling reasons to take action. With a compelling value justification, buyers often ask to get started early. In other words, the cost or impact of delay is so overwhelming that they can’t afford to wait any longer.

Minimize Discounting When the buyer and the salesperson know the real (measured and quantified) value, this onerous pressure can be greatly reduced. The buyer is less likely to ask for (or at least expect) a discount, and the salesperson is less likely to feel he or she has to give one.

Provide Proof Visionaries see how the implementation of your offerings will give them an advantage in the marketplace. However, these visionaries only make up 20 percent of buyers in the market. The other 80 percent are more pragmatic and conservative. They need proof and the demonstration of high value to mitigate the risk that buyers naturally feel at the close of sell cycles. Value justification and value analysis are very important to this segment of the market.

Avoid No Decision For one reason or another, some opportunities never conclude. The customer makes a no decision (we call this No Decision, Inc., or NDI). One of the main reasons buyers end up making a no decision is that they see no compelling reason to act; they don’t see enough value in the solution.

I contend that we actually do lose these opportunities because buyers do make a decision—they choose an alternative project. They don’t go with you or your competition, but they choose instead to invest that budgeted money with someone else. We all need to stop kidding ourselves about this situation; we lost.

Think of your buyers as people who hold the money like bankers. They don’t sit on the money; they invest it to get a return. You may well be competing against an accounting system, a new fleet of trucks, furniture, and so on, not just your usual competitors. Expect your buyers to go with the projects that provide the greatest value and the greatest return.

THE VALUE JUSTIFICATION MODEL

I recommend that every company provide its salespeople with a model to assist them with value justification. Keep in mind that every prospective customer will have his or her own way of analyzing value and the return on investments. Nonetheless, you’re always better off being prepared and presenting a projected ROI based on what you’ve learned. Unless you’re asked otherwise, keep it simple, and if the customer wants to take the analysis further, you’ll gladly assist him or her. (See Appendix A for a sample value justification.)

VALUE JUSTIFICATION ELEMENTS

The key to a successful value justification is making sure the customer owns it. After all, it doesn’t matter what you think; it’s what the customer thinks. I encourage salespeople to answer the five following questions with their value justification models:

- What elements of the customer’s business will be impacted and measured?

- Who is responsible for the changes in the impacted areas?

- How much impact and value is possible, and over what period of time?

- What capabilities will be needed?

- When will the investment pay for itself?

Element 1 What Will Be Measured?

Many elements and measurements are superfluous. You can clutter your buyer’s vision if you choose measurements that detract from the real issue. Find out the few elements that if changed will make a significant difference. When two or three elements or reasons for the problem align with your products and services, make those the key points in the value justification. Examples include the following:

Profits Remember, this is the reason most organizations exist. If you don’t include profits as one of your elements in the value justification, you’re making a mistake.

Revenues This element is very powerful because businesses (and even nonprofit organizations) depend on it to survive. Cash flow is critical, and revenues are needed to sustain good cash flow. Organizations depend on revenues to pay staff, suppliers, and shareholders, so revenues tend to have immediate, direct consequences. Revenue measurement can focus great buying attention on your capabilities.

Cost Whether absolute or relative, I’m talking about cost reduction or cost containment. This is a very big area of opportunity because every part of every organization is a cost center. The two types of cost reduction you should focus on are displaced cost and avoided cost.

Displaced Cost If your products and services can displace or get rid of an existing cost, you want your buyer telling you how and by how much.

Avoided Cost If your products and services can help a customer avoid future spending, again, you want your buyer telling you how and by how much.

Intangible Benefits These benefits, such as employee morale, customer satisfaction, image, reduced stress, goodwill, and quality of life, are hard to put a dollar value on. However, if the customer is willing to assign a value to them based on the capabilities of your solution, I suggest you include them in your value justification model.

Element 2 Who Is Responsible?

It is critically important that the customers own the value justification. This comes into play when the customer is ready to make a decision. If the person ultimately responsible for making the decision asks about the value justification and the response is, “I don’t know where those numbers came from” or “I don’t know if we can achieve those results or not,” the decision to move forward with your proposed solution will likely not happen. On the other hand, if the person being asked responds, “Yes, those are my numbers, and yes, we can achieve the results because of the capabilities being proposed,” the decision to move forward with you will happen.

Element 3 How Much Total Value Is Possible?

How much can profits improve? How much can revenues increase? How much can cost be reduced, either displaced or avoided? The value justification must answer all these questions, and the answer needs to cover a period of time—one year, two years, and so on.

Element 4 What Capabilities Will Be Needed?

The value justification must state what capabilities will help change the business. If this question can’t be answered with assurance, why would a prospective customer take the risk? For example, if a company was experiencing rising costs in the customer service department and this was negatively impacting profitability, you would want to link specific capabilities you offer to reducing or avoiding additional cost in the customer service department. For example, it might sound something like this: “What if you could allow your customers to access their own accounts online and see frequently asked questions from other callers, thus eliminating your need to hire three new customer service representatives and the additional $250,000 in expenses you’re scheduled to take on this year? Would this help? Would this be of value to you?”

Element 5 When Will This Investment Pay for Itself?

Value justification must answer this question. Buyers want to know when the breakeven point is. They want to know when the numbers start to turn from red to black. The answer is when the cumulative total benefits, including the increase in revenues and the reduction in cost, exceed the cumulative investments made to acquire and implement the products and services, including services suggested in any Implementation Plan. (See Appendix A: Part 2 for an example.)

ADVANCE THE EVALUATION PLAN PREPROPOSAL REVIEW

Go back and take a look at the Evaluation Plan in Figure 12.2. Toward the bottom of the plan, note the event, Preproposal review meeting.

One way to ensure that your final proposal wins the business is to have the customer review the proposal before it is due and take ownership of the document. You want all the work that’s been completed to date to be the customer’s work. It needs to be the customer’s proposal, not yours.

Before the preproposal review is conducted, the salesperson should make sure all legal, technical, and administrative approvals have been cleared and all value has been established. If you don’t have these items completed, then you give the committee an excuse to delay accepting the proposal.

During the preproposal review meeting, review and reconfirm all go decisions. These were the mutual decision points in the Evaluation Plan to proceed. Be sure to review organizational interdependence from the perspective of each key player by recapping the Pain Chain. Review the value justification elements and all the other work that has been done, making sure that nothing has changed.

Overall, this approach should satisfy the buying committee members that you have accomplished some powerful things: (1) you’ve gone through a mutual process with their organization, (2) you understand their business, (3) you’ve brought operational capabilities to help them resolve their critical issues, (4) you’re prepared to help them (via your products and services) get from where they are today to where they want to be, and (5) you’ve established the value and a payback (using their numbers) that is compelling. Finally, you can make sure that nothing has changed on the customer’s behalf.

When ending the preproposal review, and if everything appears in order, suggest an early close. You might do this by saying, “I know you weren’t planning on approving the proposal until next week, but it seems like everything is in order. Does it make sense that we approve this today so you can start realizing the benefits of the capabilities sooner?” If the review has been compelling, the buying committee itself may even approve an early closing. Depending on the committee’s reaction, you may need to schedule another preproposal review due to competition or items that need to be completed.

Sometimes, no matter how much they might like your proposal, the buying committee members feel they should wait and get final proposals from the other vendors. In that case, you should ask to come back after all the other vendors have presented. This allows you to address any new issues that may arise from competing vendor presentations.

Here’s a story I like about Ross Perot. In 1957, after an honorable discharge from the U.S. Navy, Perot became a salesperson for IBM’s data processing division in Dallas, Texas. While with IBM, Perot is said to have developed the “yellow pad” proposal (the forerunner to the preproposal review). Legend has it that Perot provided each member of the buying committee with detailed notes (on yellow legal pads) concerning all the activities and events of the buying process up to that point. His goal was to review the content in a draft format and get his customers’ input before presenting them with a final proposal.

If he felt everything was in order, he would suggest an early close, even leaving the room to allow the committee to talk in private. Upon his return, if the committee was not ready to move forward, he would pick up his yellow pads and explain that he must have missed something if they weren’t ready to move forward. He would leave, saying that he would “fix it” and return.

As the story goes, Ross never left a draft proposal behind. One of his claims to fame is that he never delivered a final proposal to a customer that he didn’t win.

ADVANCE THE EVALUATION PLAN SUCCESS CRITERIA

One item on the suggested Evaluation Plan that deserves special attention is Measure Success Criteria. The objective of putting together a list of Success Criteria is to determine if and when a project is successful. The approach is straightforward: It establishes a baseline and measures how business is done before your solution is implemented, monitors the postsale results, calculates the delta (the improvement), and then reports the findings.

Success Criteria identifies specific elements that the buyer and salesperson agree will be impacted and that should be measured once the capabilities have been implemented. It could be one or two items or it could be a long list, but it’s essential that they be measurable. The actual criteria are mostly derived from information uncovered during the vision processing conversations and the elements defined in the value justification.

Establishing Success Criteria helps salespeople in multiple ways. Initially, it helps to establish credibility and trust—key ingredients in any relationship. It’s important for the salesperson to let the customer know that he or she isn’t going away, that the salesperson is interested in the customer’s overall success, not just in making the initial sale. Success Criteria allow the salesperson to put a stake in the ground to measure against postsell. It’s often hard to go back and get baseline metrics after the sale is closed.

I recommend that you measure performance quarterly, though this may vary depending on your customers’ business. Look at the example of a Success Criteria chart in Appendix A.

YOUR SUCCESS DEPENDS ON YOUR CUSTOMER S SUCCESS

There are important benefits to establishing Success Criteria during the evaluation process and then measuring to determine the amount of success later on. When your customers achieve a measurable change in their business, it’s a success for them and it’s also a success for you. Their success becomes a Reference Story that you can leverage.

Reference Stories tell of other customers who reduced costs or increased profits by a specific amount because they used your capabilities. The best way to obtain these compelling results is to determine the elements to measure during the evaluation process and, postsale, follow up and measure them on an ongoing basis. Today’s success becomes tomorrow’s Reference Story.

Part One - Solution Selling Concepts

Part Two - Creating New Opportunities

- Chapter Four Precall Planning and Research

- Chapter Five Stimulating Interest

- Chapter Six Defining Pain or Critical Business Issue

- Chapter Seven Diagnose Before You Prescribe

- Chapter Eight Creating Visions Biased to Your Solution

Part Three - Engaging in Active Opportunities

Part Four - Qualify, Control, Close

- Chapter Eleven Gaining Access to People with Power

- Chapter Twelve Controlling the Buying Process

- Chapter Thirteen Closing: Reaching Final Agreement

Part Five - Managing the Process

EAN: N/A

Pages: 106