Chapter 7: The DuPont Model

|

Introduction to the DuPont Model

THE PURPOSE of this chapter is to discuss the DuPont Model and its use in the operational filter. This model has been used to detect the drivers of change in financial performance. The model is also an excellent tool for a forward-looking assessment of Strategic Alternatives. The DuPont Model was originally developed in 1919 by a finance executive at E.I. du Pont de Nemours and Co. of Wilmington, Delaware, for financial planning and control purposes. The DuPont system helps many companies understand the critical building blocks in return on assets (ROA) and return on equity (ROE).

Return on assets is a measure of the productivity of assets. Assets appear on your balance sheet. They are things that you own. Some examples of assets are equipment, real estate, inventory, software, trademarks, and patents. ROA tells you how much net income your assets are generating. This type of measurement is important in understanding short-run impacts to value. It can be used to measure the productivity of Strategic Alternatives in isolation and combined with the rest of the business. ROA is an important tool for the analysis of mergers and acquisitions because it measures the productivity of the transaction on the total purchase price.

Return on equity (ROE) measures productivity in relation to equity. This measure focuses on the part of the investment that is funded by equity. Strategic Alternatives can be funded using two sources: debt and equity. Debt is money that is borrowed (for example, money from the bank). Equity is money that is contributed by shareholders. Projects are funded using a mix of debt and equity. This mix affects the cost of capital, which may be used as the adjustment for time and risk (as discussed in Chapter 10)—more specifically, the risk adjustment. Risk adjustments start with a benchmark called the cost of capital that takes into account the proportions of debt and equity used to fund a Strategic Alternative. A detailed treatment of the cost of capital can be found in Chapter 10.

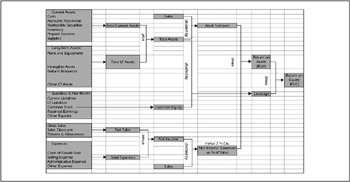

By virtue of its familiarity and simplicity, the DuPont Model is a way of visualizing the components of ROA and ROE. A typical DuPont chart resembles a chart drawn to mark the progress of competitors in a tennis or basketball tournament, as shown in Exhibit 7-1. This schematic shows how the formula links all aspects of the balance sheet and income statement together.

Exhibit 7-1: DuPont chart.

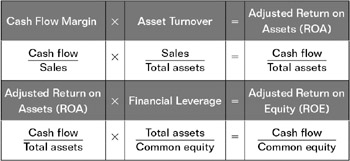

An alternate and more brief form of the DuPont approach is to use the formula itself where ROA and ROE are broken down into their component parts for further analysis, as shown in Exhibit 7-2.

Exhibit 7-2: DuPont chart—alternate version.

These components are the drivers of financial performance and consequently intrinsic value. In order to use this model to evaluate SAs, we need to adjust the model to align with the intrinsic value model. Our concept of value is based on cash flow and not net income. The difference between cash flow and net income is that cash flow does not contain noncash charges (such as depreciation, amortization, and depletion) that distort operating performance of current periods. This adjustment makes the formula appear as follows in Exhibit 7-3.

Exhibit 7-3: Adjusted DuPont chart.

Before we use the model in its new form, we need to spend time understanding its specific components.

|

EAN: 2147483647

Pages: 117