EU Government Legislation

First, for the past several years in Europe, the government has supported strongly, if not actually led, the CSR initiative. The European Union has pressed for corporations to provide wider reporting on such issues as environmental and social performance, and has set up a forum for promoting CSR programs throughout Europe, with the EU Commission in July of 2001 calling for voluntary triple-bottom-line reporting from all EU companies. The Commission also approved a resolution on CSR in 2002 that proposes the creation of a standardized multistakeholder platform for judging CSR criteria, and has provided funding to study the possibility of developing an EU Ombudsman for monitoring and assessing European company social and environmental activities in developing countries .

Similarly, in 2001 the French National Assembly passed a mandatory-requirement for nonfinancial reporting, that came as a surprise to many observers. Always strong on workers rights, of course, with its history of powerful trade unions and close corporate and government ties, France has nonetheless not traditionally been known for this type of corporate transparency or concern for the environment in the past. But in 2001, the French Parliament passed the Nouvelles R ˆgulations Economiques (NRE), a set of French laws that requires French corporations listed on the premier march ˆ (first league) of the CAC to make mandatory disclosure on social and environmental issues in their annual reports against a template of community, labor, and environmental standards. [4 ] The NRE went into effect in 2003, and made reporting on issues such as labor policies, water and energy use, and emissions of greenhouse gasses obligatory as part of a company s annual report. Organizations are also required to explain their social and environmental programs and their efforts to educate and train employees about good environmental and ethical management.

Britain, too, has moved toward enshrining at least the reporting requirements of corporate social responsibility in law. In 2002, the Trade and Industry Secretary, a British cabinet-level post, officially took on the job for advocating corporate social responsibility (the British remain the only nation to have a cabinet-level position officially dedicated to CSR), and the government has made a straightforward case for the use of public policies to promote standard codes of conduct and to encourage social and environmental reporting.

This government effort came on the back of moves by the British insurance industry ” representing corporations that control 20 percent of the UK stock market ” to require British companies to report on their policies for managing risks in social and environmental policies. As part of a move toward greater transparency and disclosure, British law also now requires pension fund trustees to declare to what extent they take into account social, environmental, and ethical issues when making their investment decisions.

These moves by the government to support social and environmental reporting were a direct reflection of the British public s demand for higher standards of corporate behavior. Half those responding to Mori s 2002 UK corporate responsibility study, for example, said that business should pay as much attention to society and the environment as it does to financial performance. Almost half of those interviewed (44 percent) said that social responsibility played a very important part in their purchasing decisions. This number has almost doubled in the past five years. [5 ]

With an extraordinarily active group of consultancies, forums, initiatives, and advocates, Britain is very much at the center of the SEAAR movement. UK companies are now pioneering new levels of transparency and reporting, with corporations such as British Telecom, Diageo, British Airways, and even Shell and BP/Amoco joining innovative companies such as the Body Shop and Co-Operative Bank in providing clear and detailed company reports on environmental and employment policies. In SustainAbility s recent Top 50 Sustainability Companies, the top seven companies were all British.

Possibly the most important contribution to CSR made by the British has been the development of the Ethical Trading Initiative in 1997, a collaborative effort between the UK government, British industry, and various NGOs and standards development bodies. The ETI (see Chapter Ten) encourages adoption of agreed labor and environmental standards, and promotes open social and environmental reporting, and is quickly becoming one of the de facto cornerstones of the European SEAAR framework.

One of the most progressive countries in terms of environmental policiesand SEAAR reporting, Germany is also a leader in reporting initiatives, accounting for nearly 80 percent of the Eco-Management and Audit Scheme (EMAS) reports filed in 2002. Similarly, over half of Europe s 40 facilities that have received SA 8000 certification ( guaranteeing that the facilities meet high social and labor rights standards) are in Italy, and the Italians have recently launched the Italian Resource Centre on Corporate Social Responsibility, an online database providing best practices and a guide to university and business school CSR courses. [6 ]

Many other EU countries have also taken measures toward requiring mandatory SEAAR reporting. For example, since 1995 Denmark has required green accounting by its top 3,000 firms, those that have significant environmental impacts. The Netherlands passed legislation in 1999 that requires several hundred of its companies to report on their environmental management systems. Norway passed the Accounting Act (Regnskapsloven) in 1999 that requires all companies to include health, safety, and environmental information in their annual financial reports, and Sweden has required that environmental performance information from 20,000 companies be included in their annual reports. [7 ] In total, companies from more than 13 EU countries were providing reports in 2002. (For a good summary of the many corporate responsibility and reporting initiatives now flourishing in Europe, see Appendix A).

On top of this flurry of European business and government activity in the area, the academic community has also rallied strongly in support of the CSR and nonfinancial reporting movement. Beginning with a group of prominent academics calling for a wholesale rethinking of the way business education was being offered in European universities, the result is a collaborative effort among major European business schools , the EU, and several major multinationals to integrate the core principles and values of CSR into European business school MBA and executive course curriculum.

One of the most important efforts in this area is the European Academy on Corporate Social Responsibility, an initiative that involves many of the major business schools in Europe: Copenhagen Business School, Cranfield University School of Management, ESADE Business School, ASHRIDGE, INSEAD, and many others. The academy s eventual goal is to persuade some 250 business schools and universities in Europe to adopt their CSR curriculum. Their stated mission is to help companies achieve profitability, sustainable growth and human progress by placing Corporate Social Responsibility (CSR) in the mainstream of business practice. Supporting them in this effort are many of the world s most powerful corporations, including GM, Volkswagen AG, Nike, Danone, Coca- Cola, IBM, Levi Strauss, Motorola, Microsoft, and many others.

The greatest critique of MBA training at the moment is that it is out of date, says Etienne Davignon, the director of the Academy. If teaching on CSR doesn t come fairly soon, businesses will lose interest ” not in the topic but in the business schools. [8 ]

Accordingly, the academy is sponsoring a series of research programs, funded by the EU Commission and with additional support from European corporations, that will help better define CSR, setting parameters around its activities, and helping companies apply policies and principles effectively. [9 ]

This push to incorporate CSR into a core curriculum promises to revolutionize European business education, instilling in future business leaders new views on the role of business in sustainability and social and environmental policies. The new coursework will include classes to help future managers deal with pressure groups and NGOs, to learn new accounting and reporting requirements, and to appreciate the complexities inherent in a global supply chain.

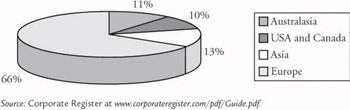

Moreover, this business and government-sponsored drive to adopt CSR programs is not limited to the European Union. Japan, itself going through a similar exercise in SEAAR realization, has the highest level of social and environmental reporting by companies in the world, with strong reports coming from powerful multinationals such as Toyota and Honda. Japan has the highest number of companies (more than 2,000 in 2001) that have been certified to the ISO 14001 environmental standard (see Chapter Ten). Australia, a strong proponent of SEAAR, particularly in their mining sector, has begun to provide tax incentives to companies that demonstrate that they have strong environmental and social policies, and under their new Financial Services Reform Act (March 2003), now requires investment firms to disclose the extent to which labor standards or environmental, social, or ethical considerations are taken into account by analysts (see Figure 5-2). [10 ]

Figure 5-2: Nonfinancial Reporting by Region in 2000

Source: Corporate Register at www.corporateregister.com/pdf/Guide.pdf.

[4 ] For a detailed explanation and critique see www.sa-intl.org/press_releases/NREPressRelease.pdf .

[5 ] Alison Maitland, Social Reporting: Pressures Mount for Greater Disclosure, FT.com, December 10, 2002.

[6 ] Italy Country Profile, CSR Europe Web site at www.csreurope.org/ partners /default.asp?pageid_ 256 .

[7 ] Paul Scott, The Pitfalls in Mandatory Reporting, Environmental Finance, April 2001, p. 24.

[8 ] Roger Cowe, Embracing Companies Social Role, The Financial Times, May 10, 2002, p. 6.

[9 ] Ibid.

[10 ] William Baue, Australia to Require Investment Firms to Disclose How They Take SRI into Account, Social Funds.com, January 3, 2003 at www.socialfunds.com/news/print.cgi?sfArticleId _998 ; Paul Scott, Reporting All Over the World, Environmental Finance, December 2000 “ January 2001, p. 36 at www. nextstep .co.uk/uploadedfiles/pdf/article5.pdf.

EAN: 2147483647

Pages: 123

- Chapter IV How Consumers Think About Interactive Aspects of Web Advertising

- Chapter VII Objective and Perceived Complexity and Their Impacts on Internet Communication

- Chapter VIII Personalization Systems and Their Deployment as Web Site Interface Design Decisions

- Chapter XIV Product Catalog and Shopping Cart Effective Design

- Chapter XVI Turning Web Surfers into Loyal Customers: Cognitive Lock-In Through Interface Design and Web Site Usability