Cost estimating

|

|

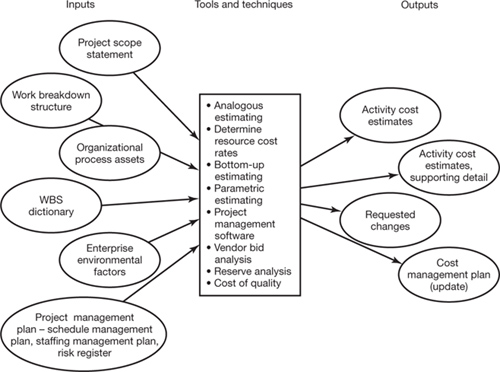

Figure 7.1 shows the inputs, tools and techniques, and outputs for the cost estimating process. Fundamentally, the purpose of the cost management plan is to answer two questions:

Figure 7.1. The cost estimating processThe primary output is the cost management plan and especially the activity cost estimates. These must be supported by the underlying details, and the process of creating the activity cost estimates will lead to updates to the cost management plan and requests for changes. The cost management plan is a part of the overall project management plan. Adapted from PMBOK Guide (p.162)

The project manager, the sponsor, the financial control function of the owning organization and the customer will certainly want to know the answers to these questions, and other stakeholders are likely to as well. As a project manager you may have legal liability for ensuring that cost estimates are prepared properly, which means that the workings by which the answers to these two questions were reached should be documented in addition to the answers themselves. The main point of doing cost estimating is to answer these two questions, which in terms of the outputs listed in Figure 7.1 means the updates to the cost management plan (usually a part of the project plan), and especially the activity cost estimates. We have just explained the need for supporting detail from the legal risk point of view. Another, more positive, reason for keeping supporting detail that underlies the cost estimates is that there may be stakeholders and subject matter experts who can hep to reduce costs or risks by reviewing the details and applying their knowledge and experience to suggest better ways of doing things. Remember that, like so much else in project management, cost estimation is an iterative process and you as project manager are there not to be an expert, but to manage the process. So you should encourage and facilitate a proper debate about cost estimates and risks, in order to improve these iteratively, finding and drawing on the relevant expertise available to the project. And of course you should work closely with the sponsor on this. Accuracy of estimatesThe future is inherently unpredictable. In a weather forecast, most people are not interested in knowing how many inches or millimetres of rain will fall tomorrow, they just want to know if it will rain or not. This means they don't need a forecast that is accurate to a sixteenth of an inch of rain, so making a forecast to that accuracy is money wasted. Another problem with weather forecasting is that it suffers the law of diminishing returns, which means that spending more money on trying to improve the accuracy of the forecast produces smaller and smaller gains in accuracy the more extra that is spent. Cost estimating is the same as weather forecasting. Sometimes an accurate cost estimate is not necessary, just something to the nearest order of magnitude. Often at the early stages of planning or initiation all that is required is a rough order of magnitude (ROM) cost estimate, to be refined perhaps as one of the first stages of the project, as the project progresses. So before you start cost estimating, ensure that you know what accuracy of estimate is required, and check whether the cost is worth it or whether a less accurate estimate might suffice. Inputs, tools and techniquesThe inputs to the cost estimating process listed in Figure 7.1 need no further explanation, as we have explained why the WBS dictionary is an important input, where there is one. Similarly, we have explained the outputs, which together answer the two key questions described above. Let us spend the rest of this section therefore describing the tools and techniques used in cost estimating, as per the list in Figure 7.1 and as that is categorized in Figure 7.2.

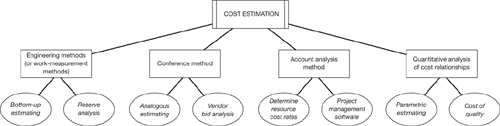

Figure 7.2. The four approaches to cost estimationThis chart attempts to categorize the PMBOK's eight specific tools and techniques for cost estimating into the more generally recognized management accounting approaches. The reason for doing this is to help readers to understand the different general approaches implicit in the eight particular PMBOK tools, and also to help them communicate with their colleagues from the finance and accounting functions, with whom they may work on project cost management. Project management software could go under any of the four headings, but will usually draw on information in the organization's MIS; increasingly project management software tools link directly into the MIS. Reserve analysis could also fall under any heading, but at heart it is an engineering technique; the same is true of cost of quality, but cost of quality should draw on all the other techniques as necessary.

Engineering methodsEngineering methods (also known as work-measurement methods) include:

Bottom-up estimating is the main technique under this heading; it means building a model or a cost structure from the bottom up. Reserve analysis means analyzing the project buffer or float, that is the amount of 'just-in-case' reserve that there should be. It can be used for two different purposes in the cost estimation process. First, project cost estimates may include a contingency reserve. Secondly, there are ways to use estimates of reserve to check the overall budget. The critical chain project management methodology places particular emphasis on using and managing a buffer or reserve. The principal features of engineering methods of cost estimation are as follows:

Conference methodThe conference method means asking other people what they think. (It is similar to the Delphi technique of information gathering.) Two ways of doing this are:

Analogous estimating means finding analogous projects, that is similar ones that have been done before or are at a more advanced stage; in other words, asking what happened last time. The case study gives an example of analogous estimating in use.

Vendor bid analysis means obtaining one or more bids for the project or parts of it from suppliers and analyzing the cost data contained therein. (Note that to request bids with the sole intention of extracting such data from them, that is, with no real intention of accepting the bid, is to act in bad faith, which is unethical and may create legal and costs risks. Even if these risks do not materialize, when an organization gets a reputation for this kind of behaviour it often finds that good suppliers cease to do business with it.) The principal features of the conference method of cost estimation are as follows:

Account analysis methodThe two particular techniques under this heading are:

The principal features of the account analysis method of cost estimation are as follows:

Quantitative analysis of cost relationshipsThe two particular techniques from the PMBOK that fall under this heading are:

Cost of quality is in terms of cost estimation a special case of parametric estimating. (The word 'parametric' simply means that parameters or other qualitative factors are used, and in this context it means exactly the same as the term 'quantitative analysis'.) The principal features of the quantitative analysis of cost relationships method of cost estimation are as follows:

|

|

Top of Page