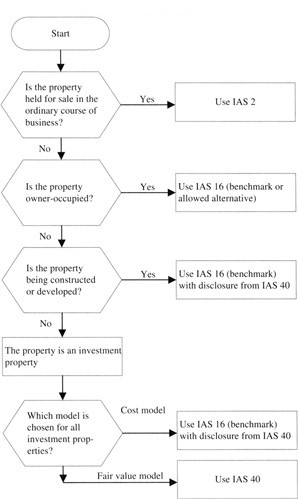

Appendix Schematic Summarizing Treatment of Investment Property (Source: IAS 40, Appendix A)

Appendix Schematic Summarizing Treatment of Investment Property (Source: IAS 40, Appendix A)

WILEY IAS 2003: Interpretation and Application of International Accounting Standards

ISBN: 0471227366

EAN: 2147483647

EAN: 2147483647

Year: 2005

Pages: 147

Pages: 147

- Integration Strategies and Tactics for Information Technology Governance

- Linking the IT Balanced Scorecard to the Business Objectives at a Major Canadian Financial Group

- A View on Knowledge Management: Utilizing a Balanced Scorecard Methodology for Analyzing Knowledge Metrics

- Technical Issues Related to IT Governance Tactics: Product Metrics, Measurements and Process Control

- Governing Information Technology Through COBIT