SETTING THE STAGE

|

|

"Consider Fe Reyes. The resident of Quezon City, Manila's biggest residential district, waited nearly three decades for the nation's monopoly telephone service, Philippine Long Distance Telephone Co., to reach her doorstep. But last year, thanks to 1993's deregulation that allowed rival companies to start offering phone service, she got a new company to install a line in just three days."[1]

The telecommunications sector in the Philippines was deregulated in 1993. Prior to the deregulation, the government-sponsored Philippine Long Distance Telephone Company (PLDT) handled the infrastructure and services requirements related to telecommunications. For most practical purposes, PLDT was commonly viewed as an operational arm of the government's Department of Transportation and Communications. Since the deregulation of 1993, over 150 new telecommunications infrastructure providers have been formed. Five players have now emerged as the leading keepers of telecommunications for the Philippines. This change has had a significant impact for the Philippines and for the Southeast Asian region in general. This new environment raises a variety of economic and technological issues that organizations need to recognize as they operate in the Philippines. With its geographical compositions of over 7,100 islands, the Philippines provides some unique challenges for information technologies and telecommunications. This case examines the current status of investments in the Philippines telecommunications infrastructure and their implications. Using a single representative organization—Globe Telecom—financial, competitive, regulatory, and technology pressures and opportunities are examined in light of a recently deregulated telecommunications sector. Using Globe Telecom as a focus organization, this case includes a macro perspective and provides insights and information that illustrate the impacts from a national and regional (Southeast Asia) perspective.

The pervasive utilization of information technology throughout the telecommunications sector inherently makes it ideally suited to study. Furthermore, economically speaking, the international investment banking sector has suggested that investments in the telecommunications sector typically produce a 30-fold return on investment for a host nation's economy. At a macro level, telecommunications can be viewed as an indicator of a country's development status. At an organizational level, telecommunications can be a source of competitive advantage (Clemons & McFarlan, 1986).

Understanding the Philippines

The Philippines unique geographical composition makes it an excellent case for a telecommunications study. Composed of over 7,100 islands, the Philippines is located in Southeast Asia off the coasts of China, Vietnam, and Malaysia, between the South China Sea and the Philippine Sea (see Exhibit 1). The nation encompasses an area of approximately 300,000 sq. km., comparable to the size of Arizona. There are roughly 80 million inhabitants of the Philippines, and approximately 11 million of those are located in metro Manila. Quezon City, within metro Manila, is the seat of the country's capital, while Makati is metro Manila's financial district. The Philippines has two official languages: Filipino and English. In fact, the Philippines is the third largest English-speaking country in the world, maintaining a 95% literacy rate. The Philippines gained their independences from the United States in 1946. Since that time, they have slowly moved toward a democracy, finally ratifying their new Constitution on February 2, 1987.

The Philippines is a member of the United Nations and the Association of South East Asian Nations (ASEAN). ASEAN plays a key role in the region and is comprised of the following countries: Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam. The functional goals of ASEAN is to accelerate the economic growth, social progress and cultural development in the region through joint endeavors in the spirit of equality and partnership in order to strengthen the foundation for a prosperous and peaceful community of Southeast Asian nations. They also aim to promote regional peace and stability through abiding respect for justice and the rule of law in the relationship among countries in the region and adherence to the principles of the United Nations Charter. The ASEAN region has a population of approximately 500 million, a total area of 4.5 million square kilometers, a combined gross domestic product of US$737 billion, and a total trade of US$ 720 billion.[2]

In 1998, the Philippine economy—a mixture of agriculture, light industry, and supporting services – deteriorated as a result of spillover from the Asian financial crisis and poor weather conditions. Growth fell from 5% in 1997 to approximately −0.5% in 1998, but since has recovered to roughly 3% in 1999 and 3.6% in 2000. The government has promised to continue its economic reforms to help the Philippines match the pace of development in the newly industrialized countries of East Asia. This strategy includes improving infrastructure, overhauling the tax system to bolster government revenues, moving toward further deregulation and privatization of the economy, and increasing trade integration with the region.[3] In 2000, the inflation rate was estimated to be 5%, the unemployment rate 10%, national debt US$52 billion, and GDP US$76.7 billion.

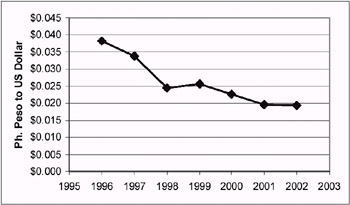

The monetary unit of the Philippines is the Philippine Peso. Over the past few years, the Philippine pesos per U.S. dollar has devaluated quite dramatically due in large part to the economic phenomenon known as the "Asian Flu." This economic downturn was widespread and lasted throughout much of the late 1990s. Figure 1 shows the Philippine Peso dropping approximately 50% in five years, from almost US$0.04 to just under US$0.02 in value. During the first two years of the new millennium, the Philippine Peso has stopped its decline and has stabilized against the US dollar.

Figure 1: The "Asian Flu" Effect and the Devaluation of the Philippine Peso

The Philippine government has gone through a number of changes in the recent years. In January 2001, President Estrada was found unable to rule by the Philippine Supreme Court due to the large number of resignations in key cabinet positions. Vice President Gloria Macapagal-Arroyo assumed the presidency for the remainder of the term. The next presidential elections will be held May 2004. Prior to the Estrada presidency, other presidential reigns included Ferdinand Marcos (1965–1986), Corazon Aquinos (1986–1992), and Fidel Ramos (1992–1998).

History of Telecommunications in the Philippines

Until 1993, the Philippine telecommunications sector was completely dominated by a single, privately-owned company. Philippine Long Distance Telephone Company (PLDT) provided 95% of all telephone service in the Philippines. Their record of poor service and even worse investment left the nation with just 1.1 phone lines per 100 residents, and a backlog of over 800,000 requests with as much as a five-year wait. Consider the following story reported in the Asian Wall Street Journal.

"Bella Tan had just given birth to her first-born son when she and her husband applied for a phone line. Her son is now 17 years old. A daughter, now 11, has been added to the family. The phone line still hasn't arrived."[4]

In 1990, investment in the Philippines telecommunications sector was approximately 1% of GDP—about one fourth of other Asian countries (World Bank, 2000).

In 1993, President Ramos signed two executive orders (Executive Order 59 and 109), in an attempt to spur competition in this sector. Executive Order 59 (see Exhibit 2) required PLDT to interoperate with other carriers, forcing them to share in the lucrative long distances market and to provide access to its subscribers. Executive Order 109 (see Exhibit 3) awarded local exchange licenses to other operators. In exchange for offering cellular or international gateways, the government also required the installation of landlines by those operators. For each license granted, a cellular company was required to build 400,000 landlines by 1998. Similarly, for each international gateway operator, 300,000 local lines were required to be added. The target of 4,000,000 new phone lines set under Executive Order 109 were met and even exceeded; with PLDT's contribution of over 1,250,000 lines, the total count of lines exceeded 5,250,000. Table 1 shows the number of lines committed and installed under the Basic Telephone program.

| Carrier | Total lines required | Total lines | Cumulative lines |

|---|---|---|---|

| Digitel | 300,000 | 337,932 | 337,932 |

| Globe Telecom | 700,000 | 705,205 | 705,205 |

| ICC/Banyantel | 300,000 | 341,410 | 341,410 |

| Islacom | 700,000 | 701,330 | 701,330 |

| Philcom | 300,000 | 305,706 | 305,706 |

| PILTEL | 400,000 | 417,858 | 417,858 |

| PLDT | 0 | 1,254,372 | 1,254,372 |

| PT&T | 300,000 | 300,000 | 300,000 |

| SMART | 700,000 | 700,310 | 700,310 |

| ETPI | 300,000 | 300,497 | 200,050 |

| All Carriers | 4,000,000 | 5,364,620 | 5,264,173 |

| Source: National Telecommunications Commission, Republic of the Philippines | |||

Table 2 shows the current status of telephone line distribution per region, including the actual number of lines installed and number of lines subscribed to. This table gives two teledensity numbers, one of capacity and one of subscription. While 9.05 is a substantial increase over the 1.1 teledensity previously provided by PLDT, and meets the goals the Philippine government set for the telecommunications sector for the year 2000, it is rather misleading in that a large number of those lines go unused. It is suspected that a large number of those lines run into business/office buildings and are not fully utilized, whereas those living in rural areas, and, in some cases, many who live in metro areas still go without. Investigating the actual subscription rates tells a whole different story. Subscribed teledensity shows that only four individuals out of every 100 have a telephone line, as compared to nearly 11 out of every 100 people for the rest of Asia and just over 17 per 100 people for the entire world's average.

| REGION | TELEPHONE LINES | SUBSCRIBERS | POPULATION | TELEDENSITY | |

|---|---|---|---|---|---|

| TELELINES | SUBSCRIBED | ||||

| I | 256,828 | 104,712 | 4,140,531 | 6.20 | 2.53 |

| II | 41,246 | 29,948 | 2,812,589 | 1.47 | 1.06 |

| III | 513,626 | 222,915 | 7,686,845 | 6.68 | 2.90 |

| IV | 1,086,030 | 470,817 | 11,301,272 | 9.61 | 4.17 |

| V | 136,465 | 61,047 | 4,755,820 | 2.87 | 1.28 |

| VI | 331,576 | 151,315 | 6,324,098 | 5.24 | 2.39 |

| VII | 484,968 | 182,278 | 5,539,177 | 8.76 | 3.29 |

| VIII | 100,468 | 48,272 | 3,743,895 | 2.68 | 1.29 |

| IX | 160,537 | 26,641 | 3,152,009 | 5.09 | 0.85 |

| X | 188,827 | 76,510 | 4,441,739 | 4.25 | 1.72 |

| XI | 366,971 | 126,168 | 5,749,821 | 6.38 | 2.19 |

| XII | 76,245 | 26,139 | 2,660,270 | 2.87 | 0.98 |

| NCR | 3,025,164 | 1,481,269 | 10,405,479 | 29.07 | 14.24 |

| CAR | 88,052 | 44,592 | 1,400,490 | 6.29 | 3.18 |

| ARMM | 48,959 | 8,764 | 2,206,106 | 2.22 | 0.40 |

| TOTAL | 6,905,962 | 3,061,387 | 76,320,141 | 9.05 | 4.01 |

| Source: National Telecommunications Commission, Republic of the Philippines | |||||

A Tale of Two Regions

The telecommunications sector in the Philippines is really a tale of two regions, metro Manila and the rest of the Philippines. NCR is the National Capital Region, which includes metro Manila. Outside of NCR and Region IV, no other region even remotely nears the Philippine national teledensity average. With those two exceptions all other regions fall significantly below the national teledensity average.

Telecommunications is more than just "plain old telephone service" (POTS). Like any country, the Philippines telecommunications industry is a mixture of a number of different services, some of which have remained relatively constant over that past several years, and some that have grown rapidly. Table 3 breaks down the Philippine telecommunication industry per the governmental recognized categories.

| TELECOM SERVICE | 1997 | 1998 | 1999 | 2000 |

|---|---|---|---|---|

| Local Exchange Carrier Service | 76 | 76 | 76 | 77 |

| Cellular Mobile Telephone Service | 5 | 5 | 5 | 5 |

| Paging Service | 15 | 15 | 15 | 15 |

| Public Trunk Repeater Service | 10 | 10 | 10 | 10 |

| International Gateway Facility | 11 | 11 | 11 | 11 |

| Satellite Service | 3 | 3 | 3 | 3 |

| International Record Carrier | 5 | 5 | 5 | 5 |

| Domestic Record Carrier | 6 | 6 | 6 | 6 |

| Very Small Aperture Terminal | 4 | 4 | 4 | 5 |

| Public Coastal Station | 12 | 12 | 12 | 12 |

| Radiotelephone | 5 | 5 | 5 | 5 |

| Value-Added Service | 47 | 70 | 106 | 156 |

| Source: National Telecommunications Commission, Republic of the Philippines | ||||

[1]Asian Wall Street Journal, June 10, 1997.

[2]ASEAN Objectives, found at http://www.aseansec.org.

[3]Information obtained from the World Factbook 2001 at http://www.cia.gov.

[4]Asian Wall Street Journal, April 15, 1996.

|

|

EAN: 2147483647

Pages: 367