6.4 Net present value and the gated project approach

6.4 Net present value and the gated project approach

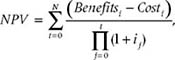

NPV is possibly the most widely accepted criterion for project evaluation. A project with a positive NPV increases the wealth of the firm, since the total value generated through the project's lifetime is superior to the cost of financing it. NPV is measured in today's dollars. The equation below summarizes the process as commonly applied.[5]

where

i = discount rate;

t = period in which Benefitst and Costt are incurred.

Its computation is based on the principle of discounting: All projected future cash flows of the project are discounted back to the present time under the assumption that one dollar today is worth (1 + i)t dollars at time t in the future. The cash flows represent the estimated costs, cost savings, and revenues at various points during the useful lifetime of the project. The variable i is the discount rate; it captures the opportunity cost and the risk of the underlying investment. A higher NPV is always preferable to a lower NPV, and a negative NPV represents an unacceptable investment [11].

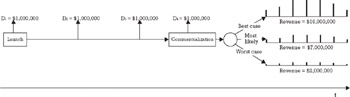

Applying the NPV method to the project illustrated in Figure 6.14, with a discount rate set at 25%[6] and the most likely return of $7,000,000, yields a valuation of

![]()

and hence the project is rejected.

Figure 6.14: NPV project valuation.

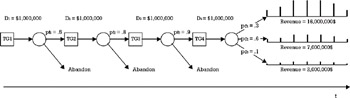

The problem with this valuation is that it assumes that the project is executed in its entirety and that the success or failure is only known at the end. This completely ignores the fact that most R&D projects are managed and reviewed throughout their existence and that many of them, but perhaps not enough, are killed in their infancy after changes in market conditions or negative results in the development stage affect their prognosis. Furthermore, in a gated approach to project management the option to continue funding the project, to defer further funding until certain conditions are met, or to stop funding are on the table at each tollgate review. The decision-tree valuation approach (see Figure 6.15) better matches the escalation of commitments implicit in the gated approach.

Figure 6.15: Decision-tree project valuation.

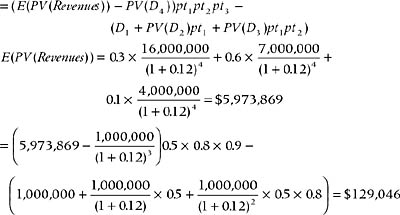

In this case, the discount rate would be set at the weighted average cost of capital (WACC)[7] of 12%[8] and the valuation of this project would be

which provides a return of 3.46%[9] over the cost of capital, and hence the project is accepted.

The reason for using different discount rates is that in the NPV method, risk is embodied in the discount rate, while in the decision-tree valuation it is explicitly captured by the probabilities of success attached to each node.

The examples above clearly show how NPV's failure to recognize that management does in fact manage, undervalues projects by not recognizing the reduction in risk that characterizes the gated decision process.

Be aware that the justification for a decision-tree valuation is provided by the ability and willingness of management to kill or change projects that do not perform up to expectations. If for cultural or political reasons management were not prepared to do it, then a decision tree or an options valuation would be inappropriate.

[5]The general form of the NPV equation is NPV which allows for different discount rates for different periods. The common form of the equation assumes that the discount rate is the same for all periods.

which allows for different discount rates for different periods. The common form of the equation assumes that the discount rate is the same for all periods.

[6]Lucent in its financial staements for 2001 used risk-adjusted discount rates ranging from 25% to 35%. Boeing for the same year used a composite rate of 18.7% to discount forecasted revenues.

[7]The after-tax weighted average cost of capital (WACC) is the intyerest rate that must be paid for the investment capital to the stockholders and the debt financiers. It is calculated by the formula WACC=PecentOfDebtFinancing CostOfDebtFinancing (1 − CorporateTaxBracket) + PercentOfEquityFinancing CostOfEquityFinancing. The value of WACC is normally provided by corporate finance.

[8]The cost of capital for several leading firms for 1999 was AOL, 16.7%; Intel, 12.9%; Pfizer, 11.4%; Walt Disney, 10.0%; and SBC Comm., 8.4%. Source: Fortune magazine.

[9]Assuming a risk-free interest rate of 5.0%.

EAN: 2147483647

Pages: 81

- Step 1.2 Install SSH Windows Clients to Access Remote Machines Securely

- Step 3.2 Use PuTTY / plink as a Command Line Replacement for telnet / rlogin

- Step 3.3 Use WinSCP as a Graphical Replacement for FTP and RCP

- Step 4.5 How to use OpenSSH Passphrase Agents

- Step 6.2 Using Port Forwarding Within PuTTY to Read Your E-mail Securely